The task of settling an estate goes beyond distributing heirlooms and property. It delves into the complexities of the tax world. When a person passes away, the assets they leave behind, collectively termed their 'estate,' might be subject to taxation. Addressing these tax obligations properly not only ensures adherence to the law but also optimizes the financial aspects of inheritance for beneficiaries. Moreover, the process of estate tax filing is a testament to honoring the wishes and legacy of the deceased. By ensuring all assets are accounted for and all liabilities met, executors and trustees are safeguarding the estate's value, thereby ensuring the departed's intentions for their assets are fully realized. At its core, an estate tax is a levy on the transfer of a deceased person's assets. It's a distinct entity from the regular income tax most individuals are accustomed to. The central document in this process is Form 706. This form, titled the United States Estate (and Generation-Skipping Transfer) Tax Return, is designed to capture all financial details of the estate. While Form 706 might seem extensive, it's methodically structured to guide the filer through the estate's assets, liabilities, and deductions. It's through this form that the IRS assesses the size of the estate and determines the tax due. It's also the platform on which any applicable tax credits or exemptions are claimed. Not all estates meet the threshold for tax filing. Only those surpassing a specific financial benchmark, set annually by federal regulations, are mandated to file Form 706. However, it's not always as straightforward. Certain nuances, such as asset transfers to surviving spouses or gifts made prior to death, can influence whether an estate needs to file. Yet, it's not just about size. Other factors, including the estate's connections to non-residential assets or ties to specific trusts, can trigger a filing requirement. This landscape of exemptions and requirements underscores the importance of a thorough understanding when dealing with estate taxes. An estate's tax journey begins long before the first figure is entered on Form 706. It starts with a meticulous collection of vital documents. The will, offering a blueprint of the deceased's wishes, is paramount. Equally vital are documents like the death certificate, which often serves as a gatekeeper to other processes, and property deeds or financial account statements that outline the estate's worth. Yet, it's not just about value. Documents also paint a picture of the deceased's financial and personal life. Previous tax returns, trust agreements, or even business contracts can shed light on potential tax obligations or deductions. Together, these records offer a cohesive view of the estate's fiscal landscape. Valuing an estate isn't merely about totaling bank account balances. It's a nuanced process that requires assessing the market value of assets, ranging from real estate and jewelry to stocks and business interests. An accurate valuation ensures that the estate pays the correct amount of tax, neither overpaying nor underpaying. This valuation extends beyond tangible assets. Intellectual properties, future revenue from ongoing contracts, or even the projected growth of certain investments can factor into the estate's worth. On the flip side, debts or obligations, including mortgages or personal loans, will reduce the estate's taxable value. This careful balancing act highlights the intricacy of estate valuation. Estate taxes can seem overwhelming, but there are avenues to mitigate the burden. The tax code allows for numerous deductions, including funeral expenses, administrative costs tied to managing the estate, and even certain debts or mortgages. By leveraging these deductions, the taxable amount of the estate can be significantly reduced. In addition to deductions, the IRS offers tax credits for estates. These credits can directly reduce the tax owed, sometimes leading to substantial savings. For instance, estates can often benefit from credits tied to previously taxed transfers or foreign taxes paid. Harnessing these deductions and credits effectively can greatly impact the estate's financial obligation. Form 706, while comprehensive, is designed to be navigable. It guides the filer, step by step, through the various sections, each tailored to capture specific financial details. From listing tangible assets like property and jewelry to detailing any charitable donations or bequests, the form leaves no stone unturned. However, while filling out the form is one task, ensuring its timely submission is another. The IRS has stringent guidelines about when Form 706 should be filed, typically mandating submission within nine months of death. Any delays can result in penalties or additional interest on taxes owed. This punctuality, paired with the form's comprehensive nature, ensures the estate meets its tax obligations fully. Tax deadlines are no mere suggestions; they're mandates set by the IRS. For estates, the primary tax form, Form 706, typically bears a submission deadline of nine months following the decedent's death. This timeframe offers a window to gather necessary documents, evaluate the estate, and ensure a precise tax filing. Yet, Form 706 isn't the only document estates need to be mindful of. Depending on the estate's structure and financial ties, other forms, each with its own unique deadline, might also be required. Keeping track of these deadlines is vital to avoid financial penalties or potential legal issues. Sometimes, even with the best of intentions, meeting a tax deadline becomes untenable. Recognizing this, the IRS provides avenues for estates to request extensions. Form 4768, specifically designed for this purpose, can grant estates additional time, typically up to six months, to file Form 706. However, an extension for filing doesn't equate to an extension for payment. Any taxes the estate owes are still due by the original deadline. If unpaid, they'll accrue interest. Yet, in certain hardship cases, the IRS might also grant extensions for payment. Engaging with the process diligently ensures that, even if extensions are required, the estate remains compliant with its tax obligations. Estates aren't only subject to estate taxes. They might also have income tax obligations. Enter Form 1041: the U.S. Income Tax Return for Estates and Trusts. This form addresses income earned by the estate after the decedent's death, such as interest from bank accounts or rent from properties. Filing Form 1041 becomes essential if the estate earns income above a certain threshold. The fiduciary, be it an executor or trustee, bears the responsibility of ensuring this filing. Through Form 1041, any applicable taxes on the estate's income are addressed, ensuring comprehensive tax compliance. Estates often function as more than static entities holding assets; they can be dynamic, earning income through various channels. When this income is distributed to beneficiaries, it carries tax implications. Beneficiaries might owe taxes on the income they receive, depending on their individual tax situations. To streamline this, estates issue Schedule K-1 forms to beneficiaries, detailing their share of the estate's income. This document becomes a beacon for beneficiaries when filing their personal taxes, guiding them on declaring any income received from the estate. Ensuring accurate and timely distribution of Schedule K-1s is, therefore, paramount. With tax obligations addressed, the estate's assets are primed for distribution. This process, guided by the will or trust documents, sees beneficiaries receiving their designated inheritance. Whether it's property, financial assets, or personal items, this distribution marks the culmination of the estate's settlement process. Yet, it's not merely a transactional process. Distributing assets also carries emotional weight, symbolizing the deceased's legacy being passed on. Ensuring this distribution is both accurate and respectful is essential, paying homage to both the departed and the beneficiaries' emotional journeys. Estate tax filings can sometimes lead to unexpected financial outcomes. Overestimations can result in tax overpayments, warranting refunds from the IRS. Conversely, underestimations or overlooked financial details might mean the estate owes additional taxes. In either scenario, proactive engagement is key. For refunds, the estate can opt for direct deposits or checks. If additional taxes are due, addressing them promptly avoids potential penalties. Throughout this, maintaining open communication with the IRS ensures the estate's financial slate remains clean. Once the estate's taxes are filed, and assets distributed, the process might seem complete. Yet, the importance of diligent record-keeping can't be overstated. Retaining copies of tax returns, asset valuations, and distributions serves as a historical record, invaluable in potential future disputes or clarifications. Organizing these documents systematically, whether in physical folders or digital archives, offers easy access. It's not just about compliance. It's about preserving the narrative of the estate's journey, offering insights for future generations or beneficiaries. The landscape of estate taxation isn't solely federal. States have their own set of rules and regulations. While some states mirror the federal guidelines, others have distinct thresholds, rates, and exemptions. For estates with assets or ties across multiple states, this can lead to intricate tax scenarios. Yet, it's not just about understanding each state's tax laws; it's also about adhering to them. Ensuring state-specific compliance, especially in states with unique estate or inheritance taxes, is paramount. This dual focus, on both federal and state regulations, ensures holistic tax compliance. In managing the financial intricacies of an estate after a loved one's passing, understanding tax obligations is paramount. The estate's assets, which might encompass everything from tangible property to intellectual rights, can be subjected to specific taxation policies. By navigating through federal forms like Form 706 and potentially state-specific regulations, executors and trustees ensure both legal compliance and financial optimization. Properly addressing the tax implications not only protects the estate's value but also upholds the intentions of the deceased, making certain that beneficiaries receive their rightful inheritances. Moreover, with possibilities of income generation even after the decedent's death, the estate might have additional tax obligations. In essence, meticulous preparation, accurate valuation, and adherence to deadlines are crucial for a seamless estate tax filing process. This ensures that the legacy left behind is both honored and preserved for future generations.Overview of Filing Taxes for an Estate

Understanding the Estate Tax Return

What Is an Estate Tax Return?

Who Must File an Estate Tax Return?

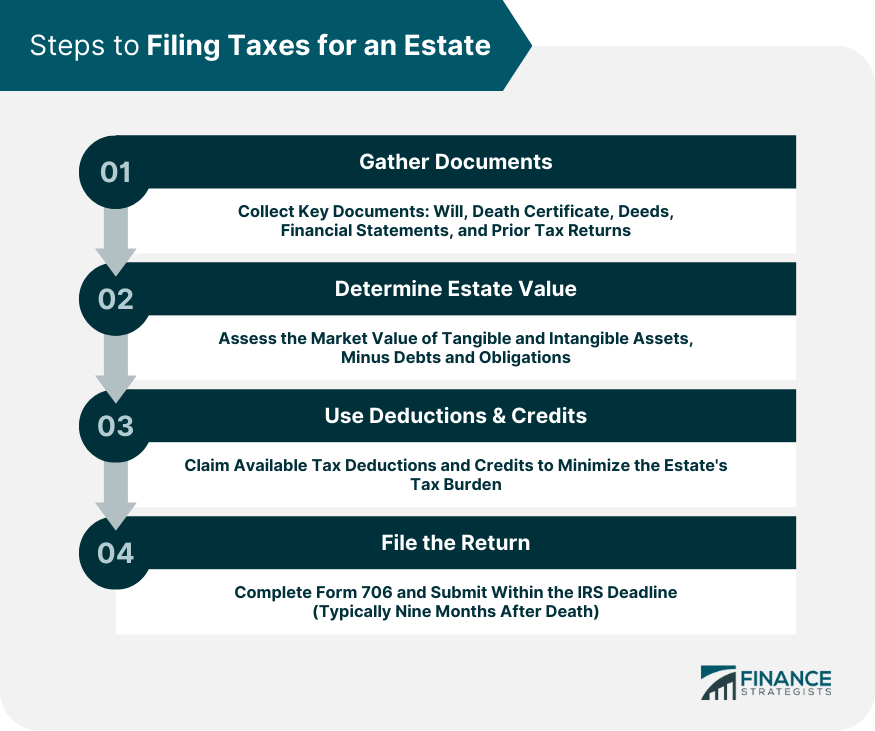

Steps to Filing Taxes for an Estate

Gather Essential Documents

Determine Value of the Estate

Leverage Deductions and Credits

Complete and File the Return

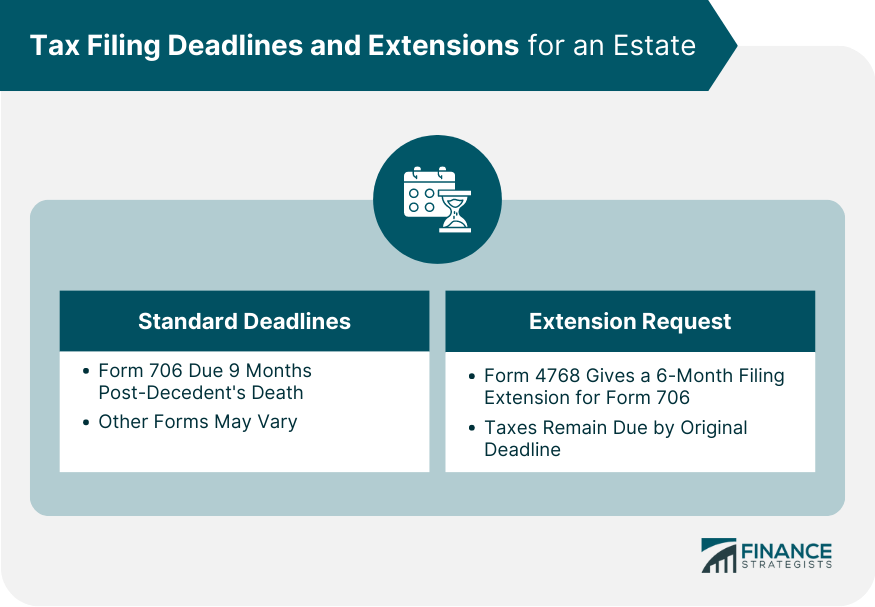

Tax Filing Deadlines and Extensions for an Estate

Standard Deadlines for Different Forms

Requesting an Extension

Income Tax Obligations for Estates

Understanding the Fiduciary Income Tax Return

Income Distribution to Beneficiaries

Post-Filing Considerations

Distributing Estate Assets to Beneficiaries

Dealing With Potential Tax Refunds or Additional Payments

Record-Keeping and Documentation for Future Reference

State-Specific Requirements When Filing Taxes for an Estate

Bottom Line

How to File Taxes for an Estate FAQs

It's a tax on the transfer of a deceased person's assets, primarily filed using Form 706.

Estates surpassing a specific financial benchmark set annually, though other factors like prior gifts can influence this requirement.

By submitting Form 4768, estates can potentially gain up to six more months to file Form 706.

Estates might need to file Form 1041 if they earn income after the decedent's death, like interest or rent.

Yes, each state may have its own rules and regulations, separate from federal guidelines, for estate taxation.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.