Taxation, often considered a daunting task, is a testament to a business's diligence and professionalism. Properly filing business taxes not only ensures legal and ethical compliance but also reflects the integrity and responsibility of a business entity. Furthermore, the process, while meticulous, serves as an indicator of a business's financial health and operational transparency. Neglecting this essential duty can be detrimental. Inaccurate tax filings or overlooking tax obligations can lead to severe legal implications and financial penalties. Beyond these tangible repercussions, businesses might suffer a blow to their reputation, a factor that can have long-lasting impacts on stakeholder trust and market perception. A sole proprietorship is the simplest form of business structure. In this model, the business and its owner are one and the same. All profits, losses, and liabilities flow directly to the owner. This setup allows for easy management and straightforward taxation, but it exposes the owner to any financial or legal vulnerabilities the business might face. In the realm of taxation, this direct flow means that income generated by the business is essentially the owner's personal income. The tax implications are hence intertwined with the owner's personal tax obligations. It's a structure that offers simplicity but demands caution, given the personal liability involved. Partnerships emerge when two or more individuals collaborate in a business venture. Here, all partners contribute resources—capital, skills, or other assets—and share the profits and losses. In terms of taxation, partnerships operate as pass-through entities. This means the entity itself isn't taxed; instead, each partner reports their share of the profits or losses on their individual tax returns. While partnerships offer the advantage of pooled resources and collaborative decision-making, they require clear agreement terms. This clarity is essential to ensure transparency in profit distribution, responsibility allocation, and tax obligations, making them beneficial yet demanding diligent governance. Corporations stand as distinct legal entities, separate from their owners or shareholders. This separation offers protection to shareholders from the company's liabilities. A C-Corporation faces its own set of taxes on profits, and then shareholders are taxed again on dividends, leading to what's known as double taxation. S-Corporations, on the other hand, allow profits and some losses to pass directly to the owner's personal income, without corporate tax rates applied. Navigating the corporate tax realm necessitates a deep understanding of its intricacies. While it offers liability protection and potential financial benefits, it's essential to remain cognizant of the regulatory complexities and potential pitfalls. Limited Liability Companies (LLCs) provide the best of both worlds, combining the flexibility of a partnership with the liability protection intrinsic to corporations. Members of an LLC aren't personally liable for company debts. When it comes to taxes, LLCs showcase versatility. They can choose to be taxed as a sole proprietorship, partnership, or corporation, depending on their preferences and what's financially advantageous. This flexibility, however, demands an informed choice. Each taxation path offers its unique set of advantages and implications. Therefore, members must gauge their business operations, financial landscape, and future aspirations before locking in a decision. Your choice of business structure significantly influences your tax landscape. This choice determines the nature of tax forms to be filed, the frequency of tax payments, and eligibility for various deductions and credits. For instance, a sole proprietor might be eligible for certain deductions that a corporation isn't and vice versa. Furthermore, each structure demands a distinct level of compliance and documentation. The rigorousness of corporate tax compliance differs vastly from that of a sole proprietorship. Thus, businesses must remain informed about the tax nuances each structure introduces, ensuring they maximize benefits while remaining compliant. Income statements, often referred to as profit and loss statements, provide a snapshot of a business's financial performance over a specific period. It outlines revenues, expenses, and the resulting profit or loss. On the other hand, balance sheets offer a comprehensive view of a company's financial position at a specific moment, detailing assets, liabilities, and equity. Together, these financial statements serve as the backbone of tax preparation. They provide essential data required for accurate tax calculations. Not only do they help in determining tax obligations, but they also provide insights that can inform strategic financial decisions, ensuring businesses are not only compliant but also financially astute. Maintaining a meticulous record of business expenses is paramount for accurate tax filing. These records offer a detailed account of the money spent in running the business, from utilities and rent to marketing and employee salaries. Each of these expenses can influence the tax obligation, as many can be deducted from the taxable income. Beyond just the major costs, even the minute business expenses play a significant role. Those lunch meetings, travel expenses, or office supplies, when aggregated, can lead to substantial tax deductions. Hence, businesses should cultivate a culture of diligent expense recording, ensuring every penny spent is accounted for. Employee compensations form a substantial chunk of a business's expenses. Payroll records, therefore, become indispensable when preparing for tax season. These records detail salaries, wages, bonuses, and other forms of compensation paid to employees, all of which carry tax implications. In addition to their significance in determining tax obligations, payroll records are subject to scrutiny by tax authorities. Accuracy and timeliness in maintaining these records protect businesses from potential penalties and ensure that they remain compliant with employment tax obligations. Capital assets, be it machinery, equipment, or technology, represent significant investments for businesses. The tax code allows businesses to deduct a portion of these assets' cost every year, a concept known as depreciation. To leverage these deductions, businesses must maintain detailed records of these assets, their purchase dates, costs, and the method of depreciation applied. By keeping an organized record of assets and their depreciation schedules, businesses not only ensure they avail of the maximum deductions but also safeguard themselves from potential audit discrepancies. These records, while serving immediate tax needs, also aid in informed business decision-making regarding asset management and investments. Beyond the standard documents, businesses often find themselves entangled with a myriad of other tax-relevant documents. These could range from interest statements for business loans, records of tax-deductible contributions to retirement plans, or documentation of any tax credits availed. While each might seem trivial in isolation, together they paint a comprehensive picture of a business's tax landscape. Having an organized repository ensures that businesses are primed to tackle tax season head-on, with all necessary ammunition in their arsenal. Targeted at sole proprietors, Form 1040 Schedule C is a crucial tax form that details the profits and losses of their business. It's a comprehensive document that delves into income streams, cost of goods sold, and business expenses. Once populated, the net profit or loss gets transferred to the owner's individual tax return. While the form might appear daunting at first glance, its meticulousness ensures sole proprietors account for all business-related financial activities. It not only aids in tax calculations but serves as a valuable reflection of the business's financial health, offering insights for future strategy formulation. As the name suggests, Form 1065 caters to partnerships. It's a declaration of the income, gains, losses, deductions, and credits of the business. Not designed to calculate tax, it rather provides a breakdown of financial activities to inform each partner's individual tax returns. Completing Form 1065 requires collaboration. Partners must collate their financial data, ensuring each transaction is accounted for. This collective exercise not only fulfills tax obligations but fosters transparency and trust among business partners. C-Corporations, with their distinct legal status, are required to file Form 1120. This document captures the corporation's income, gains, losses, deductions, and credits. Unlike pass-through entities, C-Corporations are subject to corporate tax rates, making this form instrumental in determining their tax liability. While Form 1120 ensures C-Corporations remain compliant, it also serves a broader purpose. Shareholders, investors, and other stakeholders often refer to this form to gauge the financial health and profitability of the corporation, making its accurate completion both a legal and strategic imperative. S-Corporations, while bearing the corporation tag, differ significantly in their tax treatment. They don't pay corporate taxes. Instead, their profits, losses, credits, and deductions flow through to shareholders, who then report these on their individual tax returns. Form 1120S, therefore, serves as a conduit to facilitate this flow. Filling out Form 1120S requires a meticulous aggregation of the financial activities of the S-Corporation. Given its significance in shareholders' tax computations, its completion demands diligence, ensuring that every shareholder is equipped with accurate financial data for their personal tax filings. Tax obligations often don't stop at the federal level. Most states have their taxation systems, with unique forms and requirements. While there's a semblance of similarity between state and federal forms, nuances exist. For instance, while a corporation might file Form 1120 at the federal level, a state might have its variant with distinct fields and calculations. Understanding these differences is vital. Businesses must ensure they remain compliant not just with federal tax laws, but also with the state(s) they operate in. This dual compliance ensures businesses are insulated from potential legal complications at both levels. Business expenses, both prominent and minute, play a pivotal role in tax computations. Typical deductions include costs incurred for a home office, business-related travel, meals, and entertainment. Each of these deductions reduces taxable income, providing financial relief to businesses. However, to avail of these deductions, businesses must adhere to specific criteria. For instance, a home office deduction demands exclusive and regular use of a part of the home solely for business. Understanding these criteria ensures businesses legitimately claim deductions, maximizing savings while avoiding potential audit complications. Innovation is the lifeblood of progress. Recognizing its importance, the tax code incentivizes businesses to invest in research and development (R&D). These tax credits are designed to offset some of the costs associated with R&D activities, making innovation financially appealing. To qualify for these credits, businesses must meet certain conditions, ensuring their R&D efforts align with the broader goal of technological advancement. By availing of these credits, businesses not only benefit financially but also contribute to the broader technological and societal landscape. The Work Opportunity Tax Credit (WOTC) is a federal tax incentive aimed at encouraging employers to hire individuals from specific target groups, often facing significant employment barriers. By hiring eligible candidates, businesses can avail of a tax credit, reducing their tax liability. While the WOTC serves as a financial incentive, its broader goal is societal upliftment. Businesses, by embracing this credit, play a pivotal role in integrating marginalized sections of society into the workforce, fostering diversity, and driving economic inclusivity. With the increasing emphasis on sustainability, the tax code rewards businesses that make eco-friendly choices. Energy-efficient tax credits are designed for businesses that invest in green technology, be it solar panels, wind turbines, or energy-efficient appliances. These credits not only offer financial benefits but position businesses as environmentally conscious entities. In an age where sustainability is paramount, leveraging these credits allows businesses to bolster their green credentials while enjoying financial incentives. Filing business taxes, often perceived as complex, is more than just a legal obligation. It's a reflection of a company's commitment to transparency, ethical practices, and sound financial health. While the chosen business structure, be it a Sole Proprietorship, Partnership, Corporation, or LLC, influences the tax obligations, it's the meticulous documentation that lays the foundation for an accurate and seamless filing process. From income statements to depreciation schedules, every record serves as a cornerstone in understanding and fulfilling tax responsibilities. The landscape of business taxation is vast, spanning various forms, both at the federal and state levels. Yet, it's the tax deductions and credits, from common business expenditures to R&D, that offer businesses an opportunity to maximize savings while fostering innovation, sustainability, and social inclusivity. In essence, mastering the intricacies of business taxation is an investment in the company's reputation, financial stability, and future growth.Overview of Business Taxation

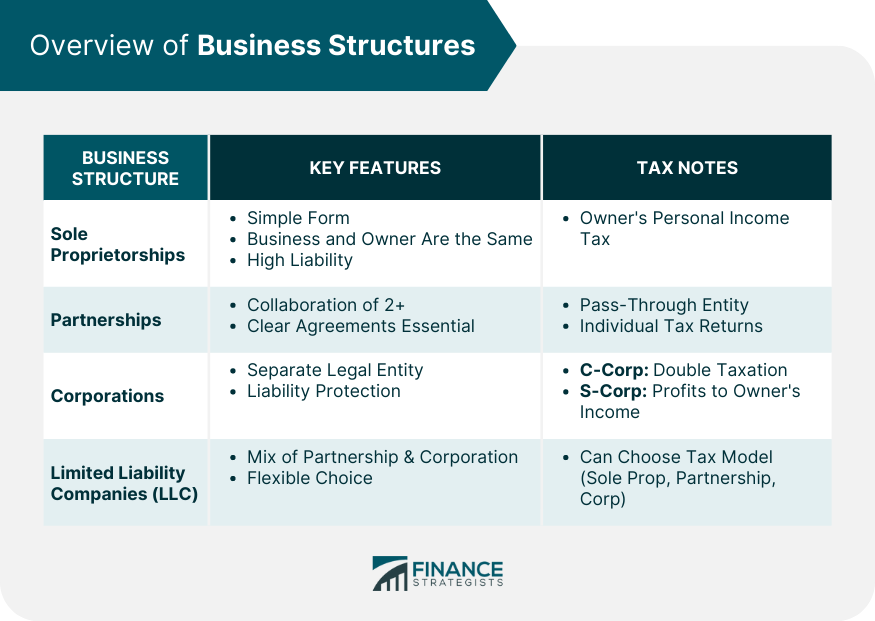

Determining Your Business Structure

Sole Proprietorships

Partnerships

Corporations

Limited Liability Companies (LLC)

How Each Structure Affects Your Tax Obligations

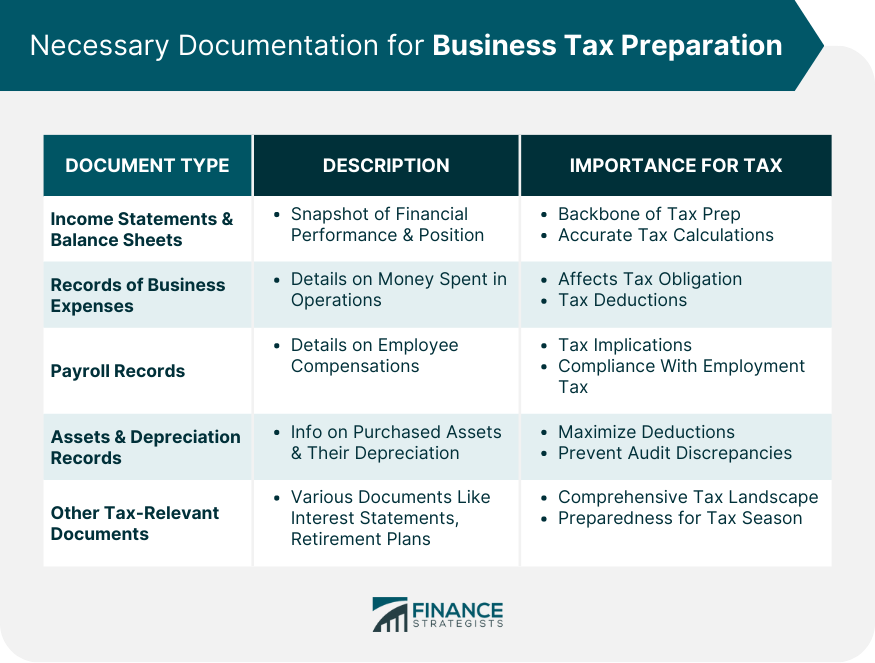

Gathering Necessary Documentation

Income Statements and Balance Sheets

Records of Business Expenses

Payroll Records

Records of Assets Purchased and Their Depreciation Schedules

Any Other Tax-Relevant Documents

Understanding Business Tax Forms

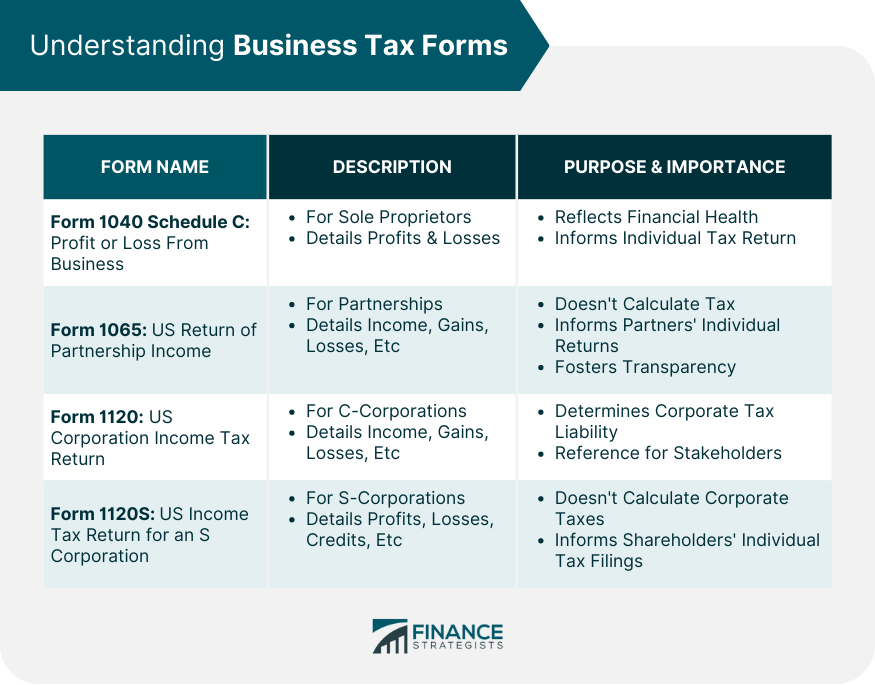

Form 1040 Schedule C: Profit or Loss From Business

Form 1065: US Return of Partnership Income

Form 1120: US Corporation Income Tax Return

Form 1120S: US Income Tax Return for an S Corporation

Differentiating Between State and Federal Forms

Tax Deductions and Credits for Businesses

Common Tax Deductions

Research and Development Credits

Work Opportunity Tax Credits

Energy-Efficient Tax Credits

Bottom Line

How to File Taxes for Your Business FAQs

The main types include Sole Proprietorships, Partnerships, S-Corp, C-Corp, and LLCs.

Key documents include income statements, balance sheets, business expenses receipts, payroll records, and asset depreciation schedules.

Each structure has unique tax treatments, from pass-through taxation in Sole Proprietorships and Partnerships to corporate taxes for C-Corps.

Businesses can deduct expenses like home office costs, business travel, meals, entertainment, and certain credits like R&D.

To ensure compliance at both levels, as each may have unique forms, requirements, and tax rates.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.