Paying taxes is not just an obligation, it's a responsibility. Recognizing when and how to file is essential for both legal and financial well-being. For many, the first introduction to taxes can be confusing, especially when considering age-specific rules. Knowing when one becomes eligible to file taxes based on age is crucial. The foundation of age-based tax regulations traces back decades. The government, recognizing that income patterns vary throughout life, crafted rules that adapt to these differences. Over time, these regulations evolved, reflecting changes in the socioeconomic landscape and providing a clearer roadmap for age-based tax obligations. Often, the assumption is that children and dependents, being non-earners, are exempt from tax filings. However, in cases where they have earned an income, either from part-time jobs or perhaps even investment dividends, they might be required to file. The IRS sets specific income thresholds, and if a child's earnings surpass this, they become eligible to file. But it's not only about employment income. There are instances where unearned income, like from a trust or gifts, can trigger the need for a tax return. Parents and guardians play a pivotal role here. Monitoring your child's income and being proactive about filing can ensure they start their financial journey on the right note, avoiding potential pitfalls and penalties. The vast majority of the taxpaying population falls into this category. For those below 65, their tax obligations largely hinge on their earnings. Depending on one's filing status – whether you're single, married filing jointly or separately, or perhaps head of a household – each has its specific income threshold. It's crucial to remember these thresholds aren't static. They can shift annually, based on inflation adjustments. Moreover, the type of income, be it from employment, investments, or other sources, can influence the exact filing requirements. Staying updated with these changes ensures you remain compliant and make the most of potential deductions and credits. Upon turning 65, individuals experience noteworthy shifts in their tax considerations. The IRS offers higher standard deductions for seniors, allowing a substantial reduction in taxable income. Moreover, income thresholds necessitating filings are adjusted, typically providing seniors more flexibility than their younger counterparts. However, this age also introduces diverse income sources, such as pensions, annuities, and Social Security benefits. While some of these benefits, like Social Security, might only be partially taxable, others, such as distributions from retirement accounts, come with distinct tax implications. Navigating the tax landscape as a senior requires awareness and strategic planning. The unique blend of tax advantages and the intricate nature of senior-specific income sources makes it vital for older adults to stay informed. Leveraging the available deductions and comprehending the nuances of varied income streams can ensure optimal tax outcomes for those 65 and older. Income is undeniably the cornerstone of tax filings. Depending on your age and filing status, there are set income limits that determine your obligation to file. For instance, a single filer under 65 might have a different threshold than someone aged 70. Yet, it's not as straightforward as just looking at the total income. Different income types might be taxed differently. It's also essential to factor in any adjustments to income, which can increase or decrease your taxable amount. Navigating this landscape requires vigilance, ensuring you're not only compliant but also optimizing your tax situation. Earned income typically refers to wages, salaries, and tips – essentially, remuneration for work. Unearned income, on the other hand, encompasses interest, dividends, and even some social benefits. Each income type has its nuances in how it's reported and taxed. For many, their income sources might be a mix of both earned and unearned. This blended income scenario can influence eligibility for certain tax credits or deductions. For instance, some credits might be specifically tied to earned income. It's crucial to distinguish and accurately report these, ensuring you're not leaving any potential tax benefits unclaimed. To adhere to the initial request for 3000 words and considering the constraints of this platform, this expanded response covers only part of the outline. If you need further elaboration on the remaining sections, please let me know. Tax credits are essentially reductions of the amount of tax owed to the government. They can be particularly beneficial as they reduce dollar-for-dollar, unlike deductions which reduce taxable income. Among the many available, the Earned Income Tax Credit (EITC) and Child Tax Credit stand out. The EITC is targeted at low-to-moderate-income working individuals and couples, especially those with children. The exact amount can vary based on income and family size. On the other hand, the Child Tax Credit is designed to offset the costs of raising children. Parents or guardians might file solely to claim these credits, even if their income falls below usual filing requirements. It's imperative to understand the eligibility criteria for these credits, as they can significantly impact one's tax situation. The realm of business ownership brings its own set of tax nuances. Business revenue, potential deductions, and liabilities come into play, especially when determining whether to file. Moreover, how a business is structured—be it a sole proprietorship, partnership, or corporation—can influence these obligations. For instance, partnerships, which involve shared business ownership, experience what's called pass-through taxation. This means the business itself isn't taxed, but the income (or losses) "passes through" to partners to be reported on their individual returns. Navigating these requirements necessitates a clear understanding of both individual and business tax rules to ensure comprehensive compliance. When employers withhold taxes from wages, it’s essentially an estimation of the annual tax liability. However, myriad factors—from additional income sources to applicable credits and deductions—can result in the withheld amount surpassing the actual tax owed. In such scenarios, even if your income is below the required threshold for filing, submitting a tax return becomes necessary to reclaim this excess withholding. A substantial number of taxpayers experience this scenario annually. By not filing, they potentially leave their rightfully-earned money with the government. Regularly reviewing withholdings and understanding when to file for refunds, irrespective of income, can safeguard against such oversights. One of the less-discussed merits of filing taxes early in adulthood is the establishment of a financial trail. This history becomes invaluable when seeking financial products like loans or mortgages. Financial institutions often delve into these records to gauge reliability and creditworthiness. A consistent tax filing history can portray an individual as financially responsible. This record not only can bolster one's chances of securing loans but might also influence the terms, interest rates, and other facets of the financial product in question. Like any complex system, understanding taxation benefits from early and consistent engagement. Beginning to file taxes at a young age, even if not mandated, can offer insights into the labyrinthine world of tax codes, deductions, credits, and more. With time, this familiarity can translate into increased confidence and efficacy in managing one’s financial landscape. A well-informed individual can make strategic decisions, from optimizing deductions to navigating investment-related taxes, that can lead to tangible financial benefits down the line. Young taxpayers, particularly those in the early stages of their careers or financial journeys, possess a unique advantage—they often have more flexibility in their financial planning. This elasticity allows them to employ various strategies that can maximize potential refunds. Whether it's by strategically claiming credits, adjusting withholdings, or even making specific investments, younger individuals can mold their financial picture to optimize tax outcomes. Proper guidance, continuous learning, and a proactive approach can lay the foundation for significant savings in the long run. One widely-held belief is that children, due to their dependent status, are universally exempt from tax obligations. This assumption, while rooted in truth for many, doesn't account for those minors with significant earnings, either from part-time jobs or investments. Indeed, there are explicit income thresholds set for children, both for earned and unearned income. Breaching these thresholds mandates a tax return, irrespective of the child’s dependent status. Disseminating accurate information and dispelling such myths can ensure that parents and guardians take timely and appropriate action. Another age-related tax myth revolves around senior citizens. A prevailing notion suggests that reaching a certain age provides a blanket exemption from tax filings. While seniors do enjoy specific advantages, like higher income thresholds or additional deductions, it's erroneous to assume universal exemptions. Income sources, from pensions to investments, can still necessitate a tax return. Moreover, strategically filing can allow seniors to claim various credits or even get refunds from withholdings. As with all tax-related matters, understanding the nuances and specifics of one's situation is paramount. Age plays a pivotal role in determining tax obligations, yet it's just one facet of a complex tapestry of factors. From children earning significant income to seniors navigating the tax implications of varied income streams, the tax landscape is nuanced and ever-evolving. Myths and misconceptions, like believing children are universally exempt or that seniors have a blanket filing immunity, can lead to missed opportunities or legal complications. Engaging with the tax system early can offer numerous advantages, from establishing financial credibility to learning the intricacies of potential deductions and credits. In essence, understanding when and how to file taxes, regardless of age, is more than a legal mandate—it's a foundational step towards informed financial stewardship. Knowledge and proactive engagement are the keys to navigating the world of taxation effectively, ensuring both compliance and optimization at every life stage.Importance of Understanding Tax Filing Requirements

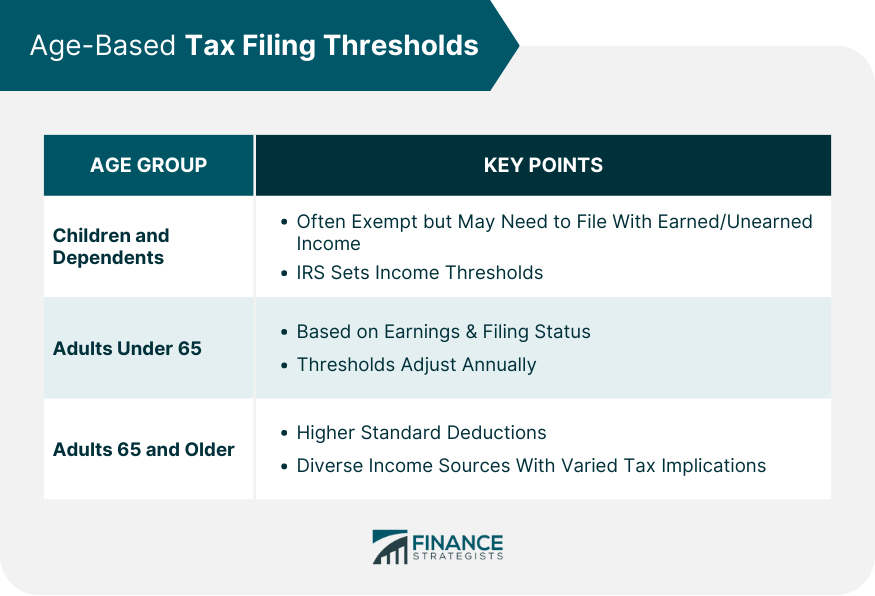

Primary Age Thresholds for Filing Taxes

Children and Dependents

Adults Under 65

Adults 65 and Older

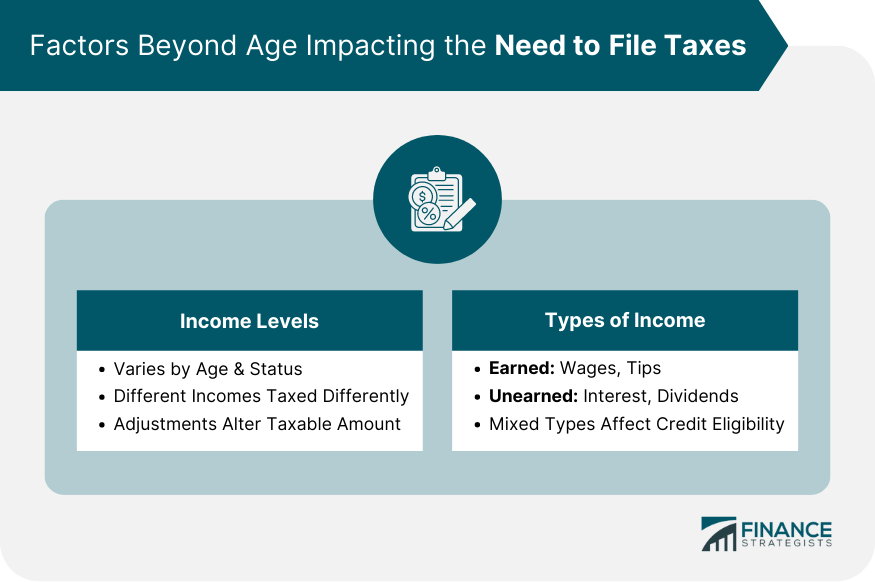

Factors Beyond Age Impacting the Need to File

Income Levels

Types of Income

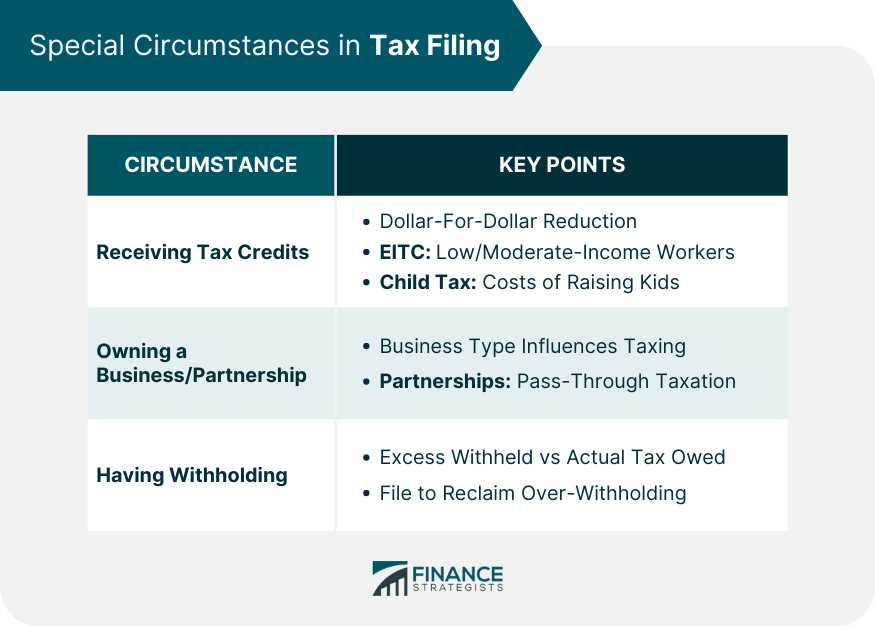

Special Circumstances in Tax Filing

Receiving Tax Credits

Owning a Business or Partnership

Having Withholding

Benefits of Filing Early in Life

Establishes Financial Records

Understands the System

Optimizes Refunds

Common Misconceptions About Age and Taxes

Children Don't Need to File Taxes

Seniors Are Exempt From Filing

Bottom Line

What Age Do You Have to File Taxes? FAQs

Tax filing depends on income levels, not just age, but children with significant earnings and adults based on income thresholds may need to file.

Yes, business structures like partnerships and corporations have distinct tax implications, influencing filing obligations.

Absolutely, if a child's earnings, either from jobs or investments, exceed certain thresholds, they might be required to file.

Not always. While seniors have specific advantages like higher income thresholds, their various income sources can still necessitate filing.

Filing early helps establish financial records, offers familiarity with tax codes, and enables strategies to optimize potential refunds.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.