Substantially Equal Periodic Payments (SEPP) are withdrawals from qualified retirement plans before 59 1/2 years, but are not subject to any early withdrawal or tax penalties. The plan mandates yearly payouts for a minimum of five years or until the account holder reaches age 59 1/2, whichever comes later. Under normal circumstances, there is a 10% early withdrawal penalty if assets are withdrawn from retirement plans before age 59 1/2. With a SEPP program, it is possible to avoid all those taxes and penalties while still having access to the funds. Have questions about Retirement Planning? Click here. Consider these factors for determining the withdrawal amount to assess if SEPP can help with your present financial situation: The Internal Revenue Service (IRS) sets specific interest rates for SEPP withdrawals. When calculating SEPP amounts using the fixed amortization and annuitization approach, the account holder may apply a rate of up to 120% of the federal midterm rate to determine the payment amount. The policy requires no minimum rate. Instead, only a cap on interest rates is needed; zero interest rates are permitted. You can maximize payment by choosing the highest interest rate within the permissible range. The interest rate choice can significantly impact the payout under the amortization or annuitization techniques. The required minimum distribution method, which considers life expectancy and the annual account amount, is unaffected. One may use the single life expectancy table, the uniform lifetime expectancy table, and the joint and last survivor expectancy table to compute SEPP. The single life expectancy table yields the shortest life expectancy, whereas the uniform lifetime table yields the longest. If the owner of the IRA wants to maximize the annual distribution, the single life expectancy table will be a better option. The uniform lifetime table will be preferable if the goal is to extend payments over the longest period. The option to select between different life expectancy values is offered for the required minimum distribution and the amortization method. There is no table selection option with the fixed annuitization approach. The table below shows an extracted expectancy table for both a uniform lifetime table and a single life expectancy table to illustrate the difference in life expectancy for a 55-year-old IRA owner. For instance, a 55-year-old IRA owner's value using the uniform lifetime table and the single life expectancy table would be 41.6 and 31.6, respectively. For the joint life and last survivor expectancy table, the taxpayer must consistently apply the table used in the first year's calculations for the required minimum distribution method in subsequent annual calculations. The correct number is taken from the table using the taxpayer's age on their birthday in the year of the distribution. The beneficiary's age is compared to the IRA owner's when the joint and last survivor table is used. Without considering any potential adjustments made throughout the year or in previous years, the beneficiary is established as of January 1 of the distribution year. If more than one beneficiary is designated at the start of the year, the figure from the table is calculated using the oldest beneficiary's age. For a 50-year-old account owner, with beneficiaries ages 25 and 55, the 55-year-old is used for calculation. Below is an extracted joint expectancy table. The result from the joint and last survivor table would be 40.2, which was determined by comparing the ages of the 50-year-old and the 55-year-old. The account balance of the individual, must be considered and used to calculate the payments they will receive. Account balances are often only significant for subsequent payouts if the RMD approach is employed. Both the annuity and amortization approaches include fixed payments, while RMD payouts depend on the account balance. Individuals should select one of three approved distribution calculation methods at the beginning of their withdrawal: amortization, annuitization, or RMD. Each will result in a different annual distribution calculation. Premature termination of the plan would incur penalties and interest on the waived plan payouts. Below are the different ways of calculating SEPP withdrawals: The amortization method is required when an individual wants fixed payments. This calculation takes into account both the interest rate and life expectancy. The amortization method subtracts the owner's life expectancy factor from the account's original value. The SEPP is then subdivided into annual installments over a predetermined period. This approach best suits those who want a fixed payment each year because it allows them to plan accordingly without worrying about changes in their account balance. Account holders are required to take the same payout each year. The amount is computed using an annuity based on the owner's age and the age of their beneficiary, as well as a selected interest rate. The annuity factor is calculated using a mortality table given by the IRS. This annuity factor is considered along with the original account balance to calculate the annual payout. The calculation is only done once, and the individual receives the same fixed payment each year until they reach the end of the withdrawal period. The account holder receives an annual payout based on their life expectancy. There would be no losses or gains on the account balance except for the SEPP payouts. At the end of life expectancy, the funds are also consumed. RMD is not a fixed payout like the two other methods. It is calculated annually by dividing the account balance by the expected remaining years left and the selected life expectancy table. Sample calculations are shown to differentiate the three methods. Anton is 50 years old with a retirement account balance of $500,000. The interest rate to use is any interest rate that is not more than 120% of the federal mid-term rate for either of the two months immediately preceding the month the distribution starts. The applicable federal mid-term rate assumed in this case is 2.24% and will be used in the amortization and annuitization methods. The annual payment remains constant over the series with the fixed amortization technique. The payment for the first year is calculated by dividing the account balance by the selected interest rate and a predetermined number of years based on the life expectancy from one of the IRS tables. By using the amortization method, the annual distribution amount is calculated by reducing the value of the account balance ($500,000) over several years, equal to Anton's single life expectancy factor (36.2) at a 2.24% interest rate. The annual distribution amount is $20,307. In fixed annuitization, there is a one-time calculation of a fixed payout based on the account value, a unique mortality factor table as a proxy for life expectancy, and an interest rate. Under the annuitization method, the annual payout equals the account balance ($500,000) divided by an annuity factor that would provide a dollar per year to Anton beginning at age 50. The annuity factor for age 50 is calculated based on the IRS mortality table and an interest rate of 2.24% resulting in an annual distribution of $20,200. The annuity factor calculation is complex and may be best left to a financial advisor or online calculators. It comprises a series of equations that account for yearly changing mortality rates. Required Minimum Distribution The RMD method of computing SEPP contributions depends totally on two things: the account balance and life expectancy With the RMD method, the distribution is recalculated every year. In Anton's case for 2022, the annual distribution amount is calculated by dividing the account balance of $500,000 by the single life expectancy value of 36.2 using age 50, resulting in a payout of $13,812. SEPPs can be a valuable tool for obtaining retirement funds early, particularly if you have lost your work or are nearing retirement age. The primary benefit of the SEPP plan is that it allows individuals to withdraw money from their retirement accounts without incurring any penalties. This early access to funds can help those in a financial pinch, such as during unemployment or medical expenses. The SEPP plan provides a steady stream of income near or in retirement. The amortization and annuitization methods can be employed to ensure that recipients have the same amount of money each year until they reach the end of their withdrawal period. You should know some significant restrictions and obligations associated with this plan. Once individuals choose one of the three approved methods, they must stick with it for their withdrawal period. If their financial circumstances change, they may be unable to adjust their payment amount accordingly. The SEPP plan requires recipients to stop contributing to their retirement accounts for them to start receiving the payments. Individuals cannot take advantage of compound interest and the tax benefits of making contributions. The SEPP plan prohibits individuals from contributing to employer-sponsored retirement accounts. Those with 401(k) or other employer-sponsored retirement plans cannot use the SEPP option and must rely on alternative methods of withdrawals. SEPP withdrawals are appropriate if you need money to survive, not to pay off one large debt or escape bankruptcy. If you lost a long-term job, take advantage of the SEPP as an alternative to unemployment benefits while looking for another one. It may be challenging to look for a career in your 50s. If you are most likely to take a lump sum, this is not an option to consider. The SEPP strategy allows individuals to withdraw money from their retirement accounts without incurring the 10% penalty associated with early withdrawals. There are three approved methods for calculating SEPP withdrawals - amortization, annuitization, and required minimum distributions. The payouts would also depend on the interest rates, life expectancy, and the account's balance. The benefits of the SEPP plan include access to needed funds without penalties and a steady income stream. Unfortunately, there are also drawbacks to the strategy, such as inflexibility and prohibiting contributions to employer-sponsored accounts. The SEPP strategy is best for those who need money to cover living expenses, such as during a period of unemployment or medical expenses. It is not a suitable choice for individuals needing to pay off large debts or escape bankruptcy.What Is Substantially Equal Periodic Payment (SEPP)?

Factors to Consider for SEPP Withdrawals

Interest Rates

Life Expectancy

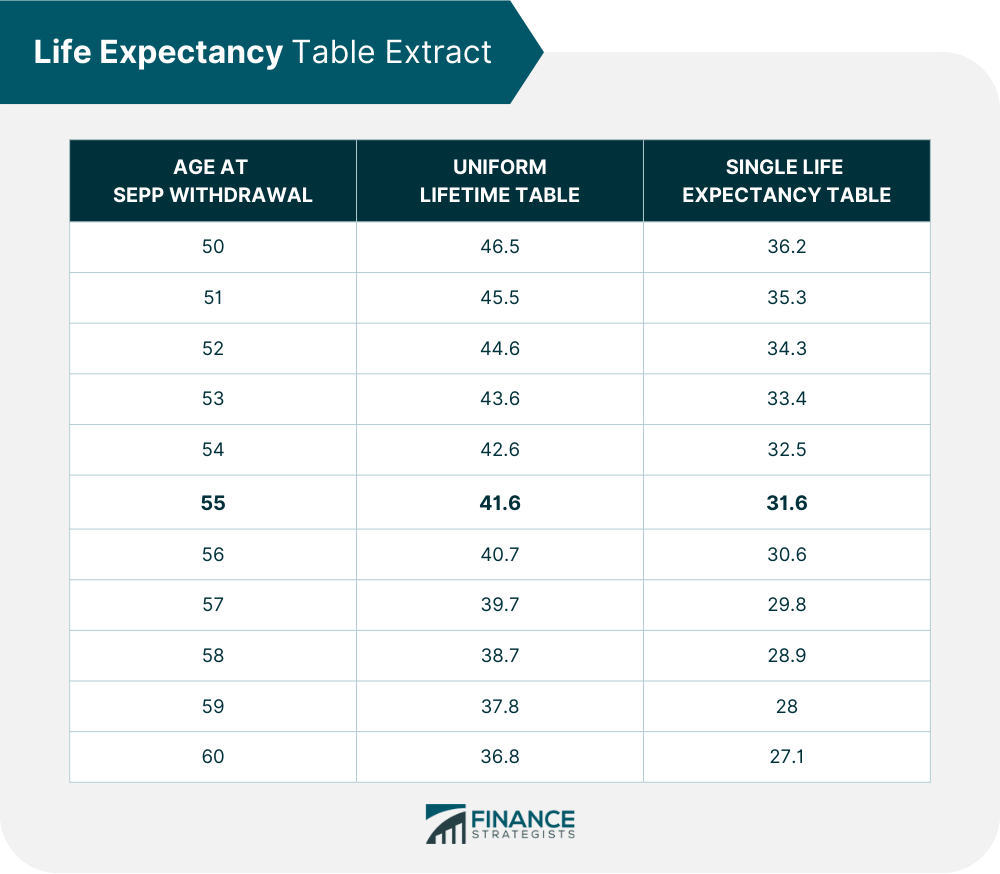

Single and Uniform Life Expectancy Tables

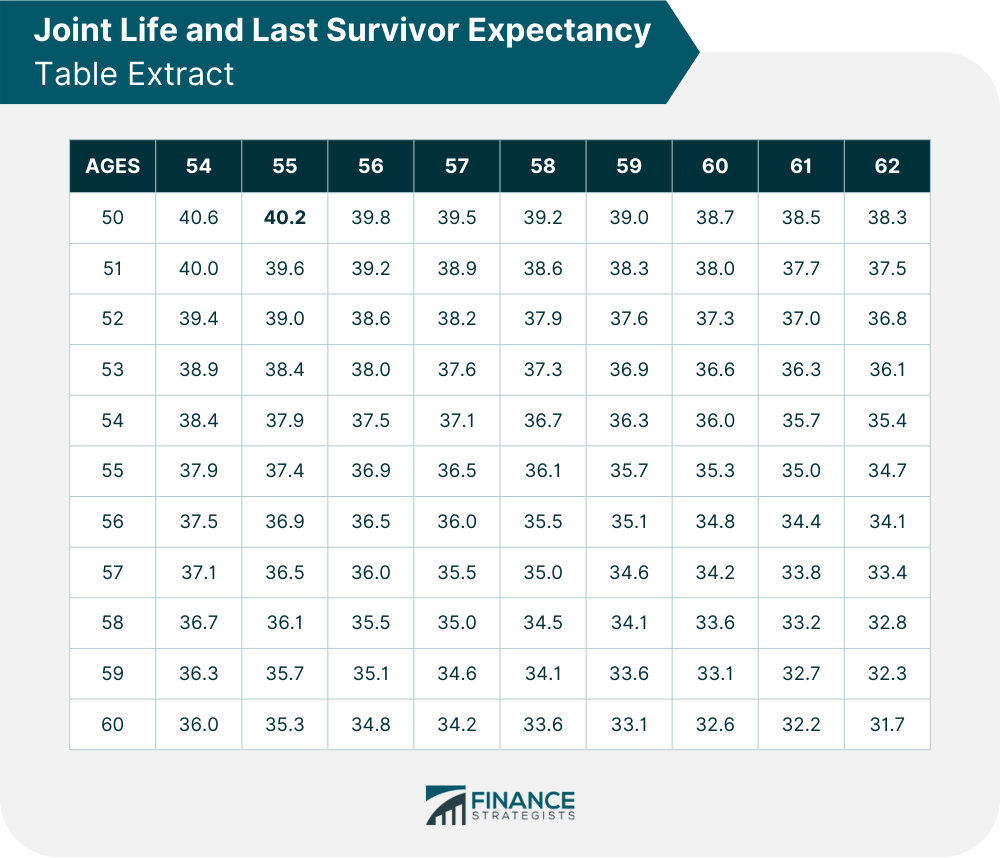

Joint Life and Last Survivor Expectancy Table

Account Balance

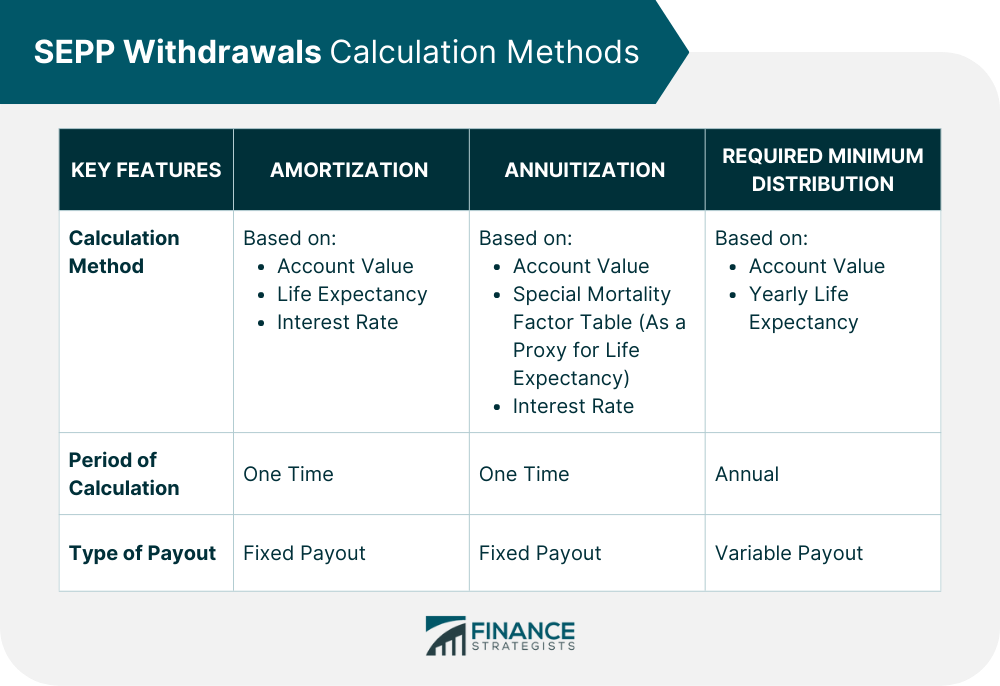

How to Calculate SEPP Withdrawals

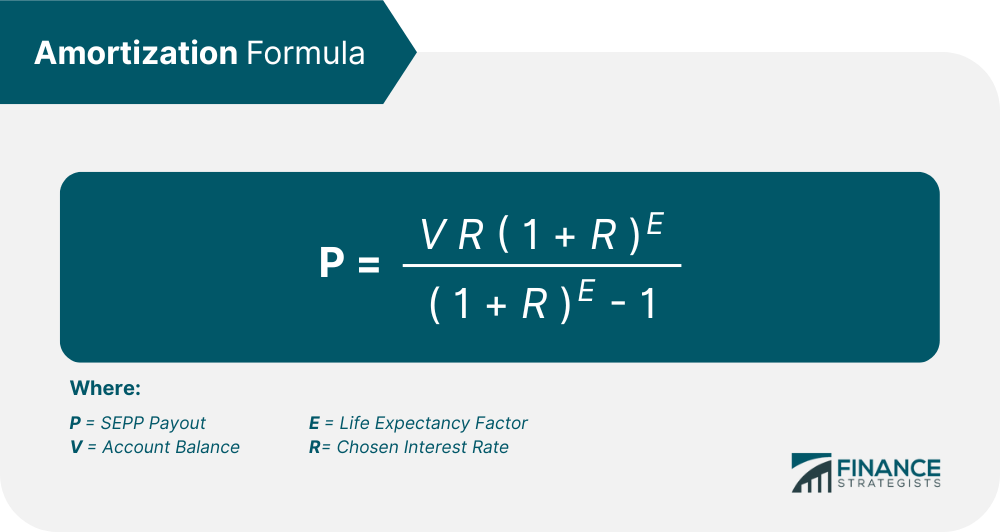

Amortization Method

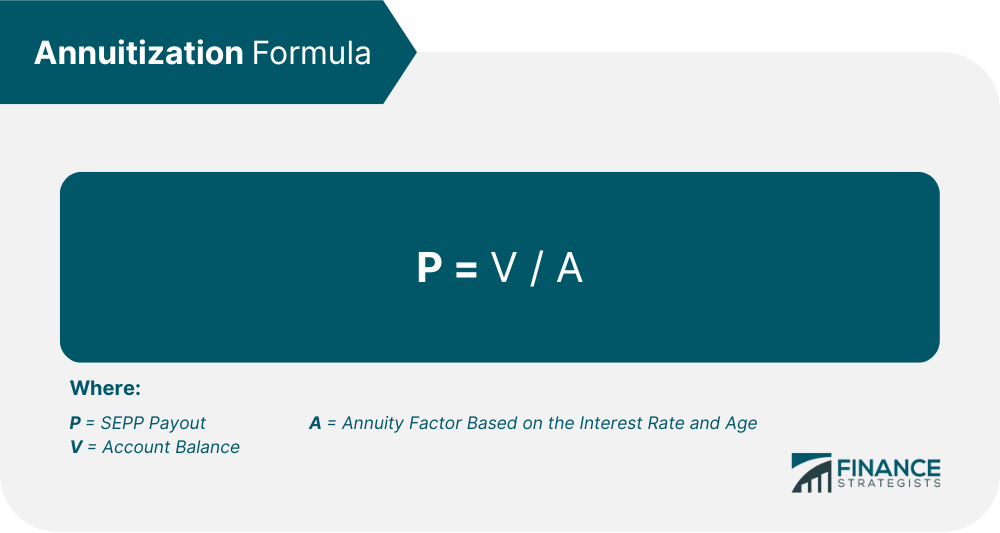

Annuitization Method

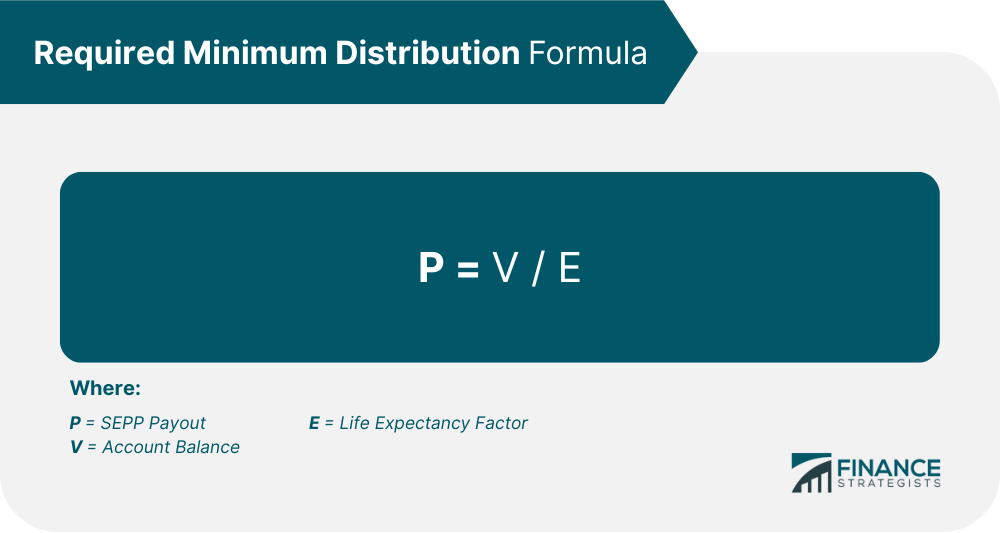

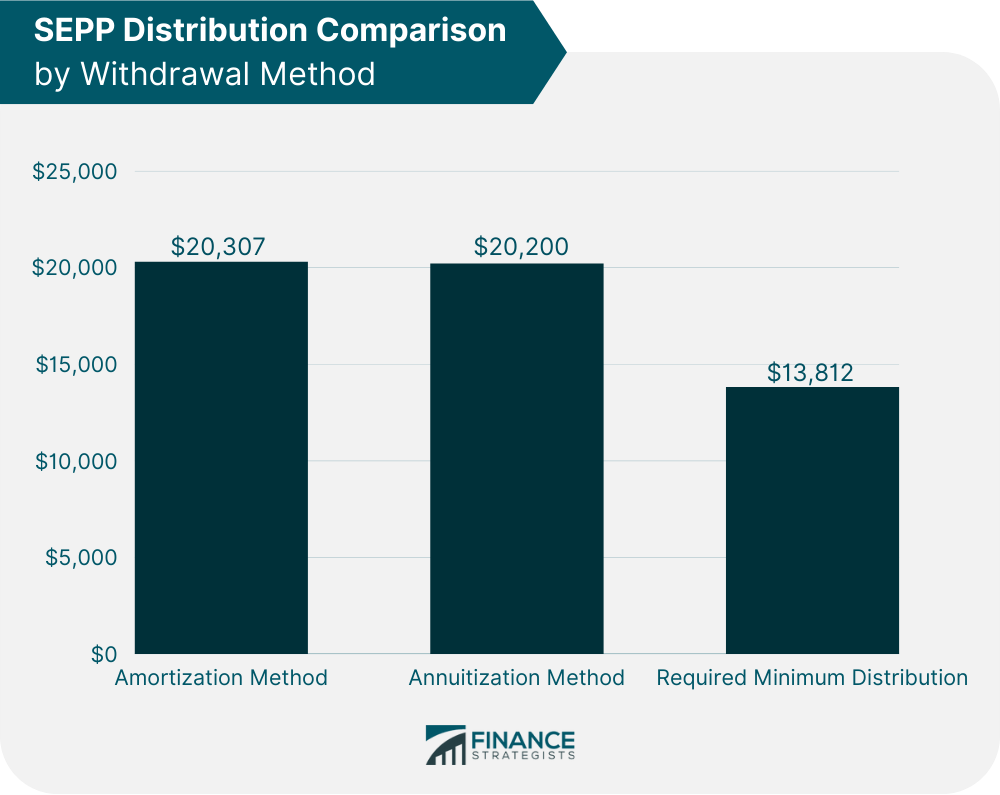

Required Minimum Distribution

SEPP Sample Calculation

The Amortization Method

The Annuitization Method

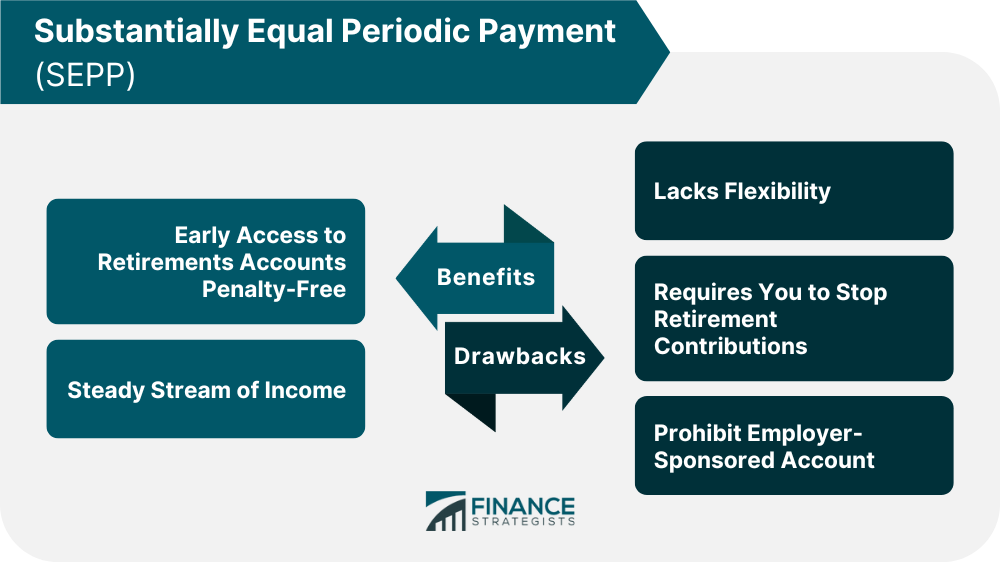

Benefits of the SEPP Plan

Early Access to Retirements Accounts Penalty-Free

Steady Stream of Income

Drawbacks of the SEPP Plan

Lacks Flexibility

Requires You to Stop Contribution to Your Retirement Account

Prohibit Employer-Sponsored Accounts

Is the SEPP Strategy Right for You?

Final Thoughts

Substantially Equal Periodic Payment (SEPP) FAQs

A SEPP is a strategy that allows individuals to withdraw money from their retirement accounts without incurring the 10% penalty associated with early withdrawals.

The SEPP strategy is most beneficial for those who need money to cover living expenses, such as during a period of unemployment or medical expenses. There are better choices for individuals needing to pay off large debts or escape bankruptcy.

Yes. The rule allows a one-time shift from the amortization or annuitization method to the required minimum distribution method. However, a switch from RMD to amortization or annuitization is not permitted.

The three approved methods for calculating SEPP withdrawals are amortization, annuitization, and required minimum distributions. These calculations would depend on the chosen interest rates, life expectancy tables, and the account's balance.

Some drawbacks include inflexibility, discontinuation of retirement contributions, and prohibiting contributions to any employer-sponsored retirement plans.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.