Medicaid spend-down is a process by which individuals who do not meet Medicaid eligibility requirements can become eligible by spending down their income and assets to meet eligibility requirements. Medicaid spend-down is a way for individuals to access necessary medical services and long-term care Nursing Homes without depleting their resources entirely. The purpose of Medicaid spend-down is to allow individuals who do not meet Medicaid eligibility requirements to access necessary medical services and long-term care. By spending down their income and assets, individuals can become eligible for Medicaid benefits and receive the care they need without depleting their resources entirely. To be eligible for Medicaid spend-down, individuals must have income and assets that exceed Medicaid eligibility requirements. Medicaid spend-down requirements vary by state but generally require individuals to reduce their income and assets to meet Medicaid eligibility requirements. Individuals must also have a medical need for Medicaid services to qualify for spend-down. Medicaid spend-down is calculated by subtracting an individual's income and assets from the Medicaid eligibility requirements for their state. The amount by which an individual exceeds Medicaid eligibility requirements is the amount they must spend down to become eligible. Examples of Medicaid spend-down can include paying for medical expenses out of pocket, paying down debts, and purchasing exempt assets, such as a home or car. For individuals who require long-term care, spend-down can include the use of long-term care insurance, personal services contracts, or the establishment of a trust. Expenses that can be included in Medicaid spend-down vary by state but typically include medical expenses, health insurance premiums, and long-term care expenses. Other expenses that may be included in spend-down can include housing costs, transportation expenses, and utility bills. Medical expenses can be a significant part of Medicaid Spend-Down. They can include expenses such as doctor visits, hospitalizations, prescription drugs, medical equipment, and other health-related costs. Individuals who have private health insurance but cannot afford the premiums may be able to include these costs in their Medicaid Spend-Down. Medicaid will pay for the health insurance premiums once the spend-down requirement has been met. Long-term care can be a significant expense for individuals who require extended care due to chronic illness, disability, or aging. Medicaid Spend-Down can help cover the costs of long-term care in nursing homes or other facilities. Individuals who need to make home modifications or need assistance with housing expenses, such as rent or mortgage payments, may be able to include these costs in their Medicaid Spend-Down. Transportation can be a significant expense for individuals who need to travel for medical appointments or other health-related reasons. Medicaid Spend-Down can help cover the costs of transportation to and from medical appointments. Individuals who have high utility bills, such as electricity, heating, or cooling, may be able to include these costs in their Medicaid Spend-Down. Medicaid is a significant source of funding for long-term care services in the United States. Medicaid provides coverage for a range of long-term care services, including nursing home care, home health care, and personal care services. Medicaid spend-down can be an effective strategy for individuals who require long-term care services but do not meet Medicaid eligibility requirements. By spending down their income and assets, individuals can become eligible for Medicaid benefits and access necessary long-term care services. Medicaid planning for long-term care can involve strategies such as asset transfers, the use of trusts, and the purchase of long-term care insurance. Working with an experienced professional can help individuals and families develop a comprehensive and effective Medicaid plan that meets their unique needs and circumstances. Medicaid estate recovery is a process by which states may seek reimbursement from the estates of deceased Medicaid recipients for certain long-term care expenses. Medicaid estate recovery can result in significant financial impact on an individual's heirs and beneficiaries. Medicaid planning strategies, such as the use of trusts and personal services contracts, can help protect assets and resources from Medicaid estate recovery. Incorporating these strategies into an individual's Medicaid plan can help ensure that their legacy is preserved for future generations. Estate planning is an essential component of Medicaid planning, as it can help protect an individual's assets and resources from Medicaid estate recovery and other potential risks. Working with an experienced professional can help individuals and families develop a comprehensive estate plan that meets their unique needs and circumstances. Medicaid spend-down is a process by which individuals can become eligible for Medicaid benefits by spending down their income and assets to meet eligibility requirements. Spend-down can be an effective strategy for individuals who require medical services and long-term care but do not meet Medicaid eligibility requirements. Understanding Medicaid spend-down and its requirements can help individuals and families plan for potential medical needs and long-term care expenses. By working with a knowledgeable professional and developing a comprehensive Medicaid plan that incorporates spend-down strategies, individuals can protect their assets and resources while accessing necessary care services. As the population continues to age and the cost of long-term care services rises, Medicaid spend-down is likely to become an increasingly important part of long-term care planning. By staying informed about changes to Medicaid policies and regulations and regularly reviewing and updating their Medicaid plan, individuals can ensure continued access to necessary care services and financial stability.Definition of Medicaid Spend-Down

How Medicaid Spend-Down Works

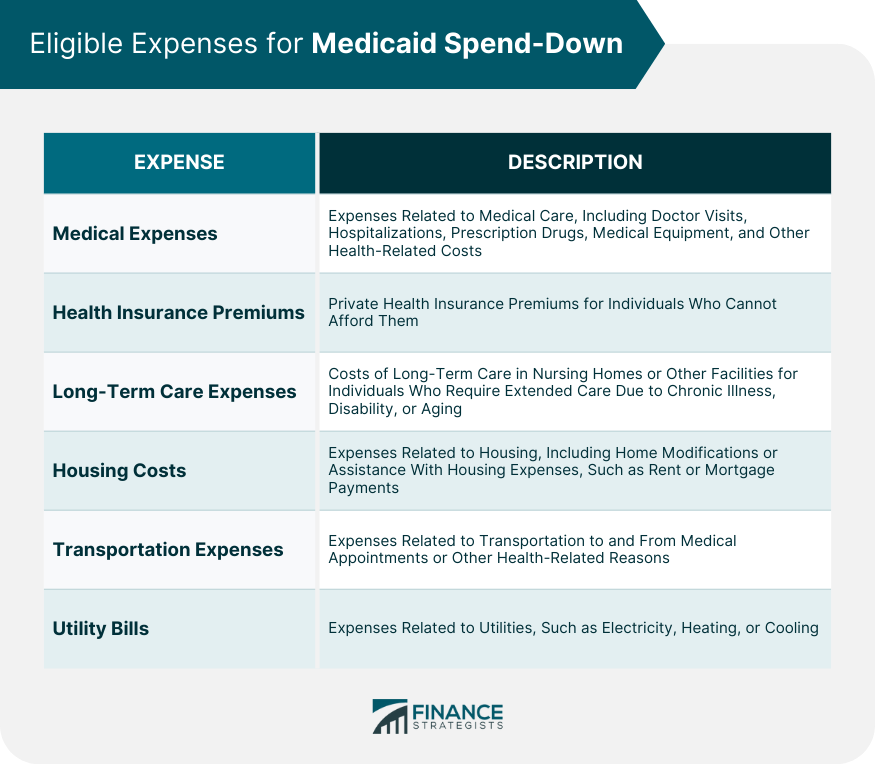

Types of Expenses Included in Medicaid Spend-Down

Medical Expenses

Health Insurance Premiums

Long-Term Care Expenses

Housing Costs

Transportation Expenses

Utility Bills

Medicaid Spend-Down and Long-Term Care

Medicaid and Long-Term Care

Medicaid Spend-Down for Long-Term Care

Medicaid Planning for Long-Term Care

Medicaid Spend-Down and Estate Planning

Medicaid Estate Recovery

Medicaid Planning Strategies

Importance of Estate Planning

Final Thoughts

Medicaid Spend-Down FAQs

Medicaid Spend-Down is a process by which individuals can use their excess income on medical expenses to become eligible for Medicaid.

Eligible expenses for Medicaid Spend-Down include medical expenses, health insurance premiums, long-term care expenses, housing costs, transportation expenses, and utility bills.

Medicaid Spend-Down works by calculating an individual's excess income and subtracting eligible expenses. If the remaining income is below the Medicaid income limit, the individual becomes eligible for Medicaid.

Individuals with income that exceeds the Medicaid income limit may be eligible for Medicaid Spend-Down if they have high medical expenses or other eligible expenses.

Planning for Medicaid Spend-Down can involve strategies such as prepaying certain expenses or transferring assets. Consulting with an attorney or financial planner can be helpful in developing a plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.