Annuities serve as a reliable income source, offering protection against the risk of depleting savings in retirement. They are contracts between individuals and insurance companies, where premiums are paid in exchange for periodic payments. Various types of annuities exist, each with its own features and benefits, all aimed at providing a steady income during retirement. Proper management and integration into a broader financial strategy can enhance retirement security. The age of 59 ½ holds significance in annuities and retirement planning, as it marks the threshold for penalty-free withdrawals from tax-deferred retirement accounts, including annuities. Early withdrawals before age 59 ½ incur income taxes and a 10% penalty. This reduces the withdrawn amount and may affect long-term retirement plans. While unexpected circumstances may prompt early annuity withdrawals, it is crucial to understand the potential consequences and explore alternative options, considering personal financial crises, medical emergencies, or unforeseen expenses. Life can be unpredictable, and personal financial crises can strike when least expected. Events such as job loss, bankruptcy, or significant reductions in income can prompt individuals to explore all available resources to stay financially afloat. During these times, one might turn to their annuity for withdrawals to cover immediate living expenses. This might include basic needs such as housing, food, and utilities or paying off high-interest debts like credit cards to prevent further financial turmoil. Health is another unpredictable aspect of life. Major health issues or medical emergencies can lead to staggering expenses, often beyond what insurance may cover. These costs can quickly deplete savings and create substantial debt if not addressed promptly. Such expenses could range from hospital bills, medication costs, long-term care facilities, or any other health-related costs not covered by insurance. Life's unpredictability can also bring about unforeseen large expenses that can shake one's financial stability. These can include emergency home repairs, such as fixing a damaged roof after a storm or replacing a failing heating system in the dead of winter. Other unexpected expenses could be legal fees due to a sudden legal issue or needing to help a family member in financial distress. Fixed annuities offer a guaranteed rate of return. Withdrawals from a fixed annuity before 59 ½ typically come with a surrender charge, which decreases over time. Variable annuities invest your premiums in a selection of sub-accounts. The account's value can fluctuate based on the performance of these investments, adding a level of risk to your returns. Early withdrawal penalties apply similarly to fixed annuities. Indexed annuities tie your return to a specific market index, such as the S&P 500. They offer a guaranteed minimum return and the chance for higher returns if the market performs well. Like other annuities, early withdrawal penalties apply. Substantially Equal Periodic Payments (SEPP) is a distribution method that allows individuals to take money out of their annuity or retirement account without paying the 10% early withdrawal penalty, even if they are under 59 ½ years old. These withdrawals must follow a specific schedule set by the Internal Revenue Service (IRS), following one of three methods: the Required Minimum Distribution (RMD) method, the Fixed Amortization Method, or the Fixed Annuitization Method. Under these methods, you must withdraw at least five "substantially equal periodic payments" spread over five years, or until you reach the age of 59 ½, whichever comes last. Not adhering to the SEPP schedule could lead to penalties, making it important to fully understand this exception before pursuing it. Another exception to the early withdrawal penalty is in cases of permanent disability. The IRS definition of disability requires that the individual must be unable to engage in any substantial gainful activity due to a physical or mental impairment. If you meet this definition and can prove it with the required documentation, you may be eligible to withdraw from your annuity without incurring the 10% penalty. Similarly, the annuity owner's death cases waive the 10% early withdrawal penalty. This allows the owner's heirs or beneficiaries to withdraw from the annuity without being subjected to the early withdrawal penalty, although other taxes may still apply. If annuity payments are part of a qualified retirement plan like a 401(k) or an IRA, the penalty may not apply under specific circumstances. The IRS rules state that if you separate from the job associated with your retirement plan in or after the year you reach the age of 55, you can take distributions from that plan without paying the 10% early withdrawal penalty. This rule does not apply to IRAs or plans into which you've rolled your retirement assets. Each retirement plan may have its own set of rules and restrictions, so it's important to understand your specific plan's guidelines before making a withdrawal. In all these cases, while the 10% early withdrawal penalty may be waived, regular income taxes on the withdrawals still apply. Moving your annuity funds to another retirement account through a rollover or transfer may avoid early withdrawal penalties. Annuitization is when the annuity's accumulated value is converted into a series of regular payments. This strategy can provide a steady income and minimize penalties, as some portion of each payment may be considered a return of principal. This strategy involves making regular, substantially equal periodic payments (SEPPs) based on your life expectancy. It can be a complex strategy, but it can provide income before 59 ½ without the 10% penalty if executed correctly. Immediate Access to Funds: Early withdrawals can provide immediate relief during financial hardship or unexpected expenses. Potential Exceptions to Penalties: There are specific circumstances, such as disability, death, or setting up Substantially Equal Periodic Payments (SEPP), where penalties may not apply. Penalties and Taxes: Early withdrawals typically incur a 10% penalty in addition to being taxed as ordinary income, which can considerably diminish the net withdrawal amount. Reduced Retirement Income: Since the value of your annuity decreases with early withdrawals, it can significantly reduce the steady income you were expecting in retirement. Impact on Compound Growth: The power of compounding is best realized over time. Early withdrawals reduce the amount of capital in the account that could otherwise continue to grow. Possible Reduction in Death Benefits: If your annuity includes a death benefit, early withdrawals could decrease the value of this benefit, impacting your dependents or heirs. Potential Surrender Charges: Depending on the terms of your annuity, early withdrawals may also come with surrender charges from the issuing insurance company. Annuity withdrawals before 59 ½ can be a lifeline in times of financial distress, but they come with significant costs and potential long-term impacts. Careful planning and consultation with a financial advisor can help minimize these risks. Proper planning and strategic use of financial instruments, such as annuities, can make your retirement years more secure and comfortable. Consider all available options and seek professional advice before making significant financial decisions. An insurance broker can offer invaluable guidance, helping to balance the need for immediate funds with long-term financial security. Remember, your decisions today can significantly impact your financial comfort in retirement.Overview of Annuity Withdrawals Before 59 ½

Reasons for Early Annuity Withdrawals

Personal Financial Crises

Medical Emergencies

Unforeseen Large Expenses

Types of Annuities and Their Withdrawal Rules

Fixed Annuities

Variable Annuities

Indexed Annuities

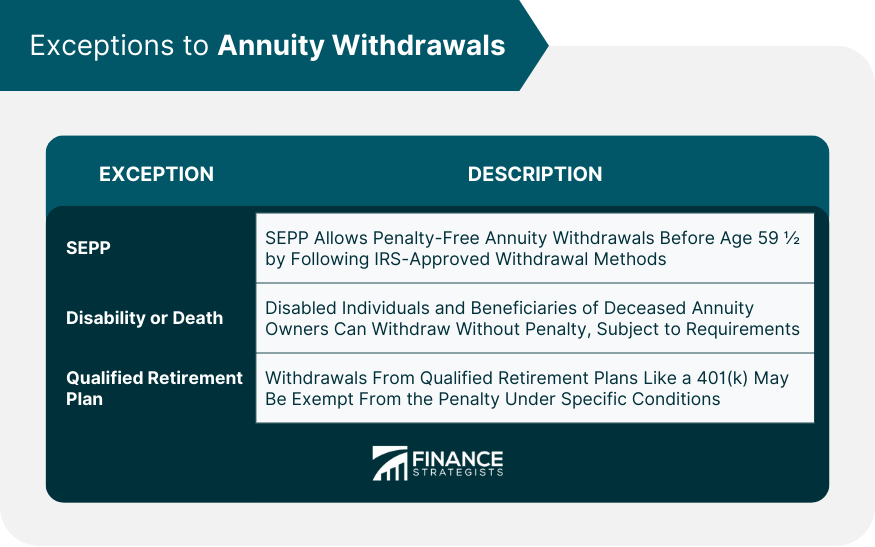

Exceptions to the Rule for Annuity Withdrawals Before 59 ½

Substantially Equal Periodic Payments (SEPP)

Disability or Death

Annuity Payments From a Qualified Retirement Plan

Strategies to Minimize Penalties on Annuity Withdrawals Before 59 ½

Rollovers and Transfers

Annuitization Strategy

72(t) SEPP Strategy

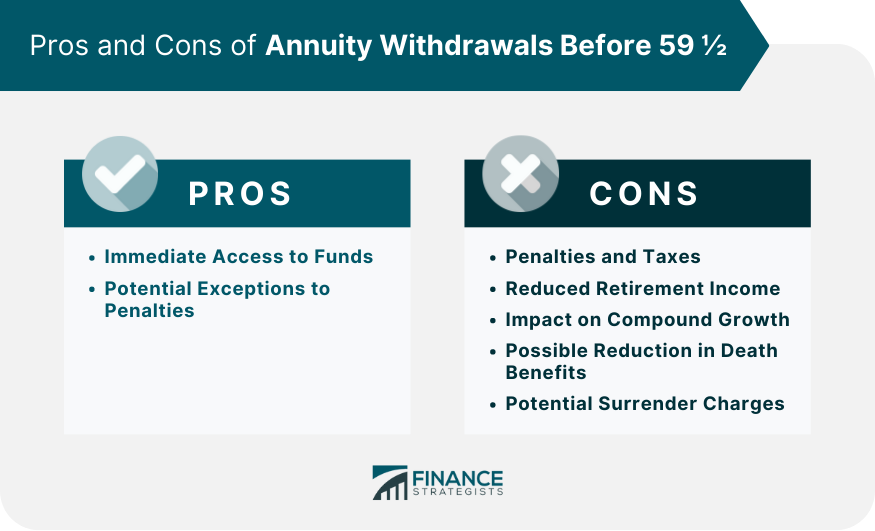

Pros and Cons of Annuity Withdrawals Before 59 ½

Pros

Cons

Conclusion

Annuity Withdrawals Before 59 ½ FAQs

When you make annuity withdrawals before the age of 59 ½, these are subject to regular income tax plus a 10% early withdrawal penalty unless you meet certain exceptions such as disability or setting up Substantially Equal Periodic Payments (SEPPs).

The IRS allows exceptions to the 10% early withdrawal penalty in certain situations. These include cases of death, disability, and taking Substantially Equal Periodic Payments (SEPPs) under rule 72(t).

No, all earnings from annuity withdrawals before 59 ½ are taxable as ordinary income in the year you withdraw. Additionally, a 10% penalty is usually added if you withdraw before this age unless you meet one of the IRS exceptions.

Annuity withdrawals before 59 ½ reduce the overall value of your annuity, which can significantly decrease the amount of income you receive in retirement. This is due to both the reduced principal in the annuity and the taxes and penalties incurred during early withdrawal.

Strategies to minimize penalties on annuity withdrawals before 59 ½ include taking Substantially Equal Periodic Payments (SEPPs), transferring or rolling over the annuity into another retirement account, or sometimes, annuitizing the contract. Always consult with a financial advisor before making these decisions to understand the potential impact on your overall financial plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.