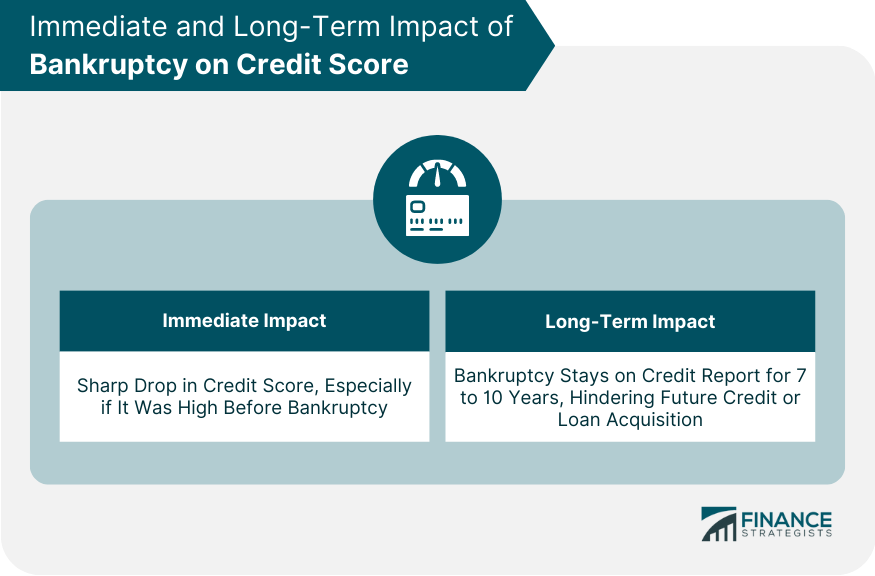

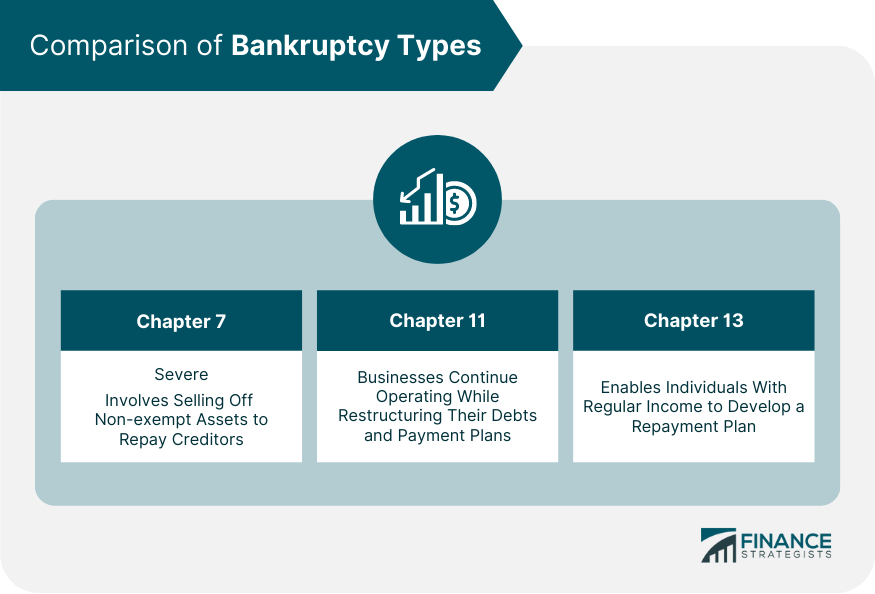

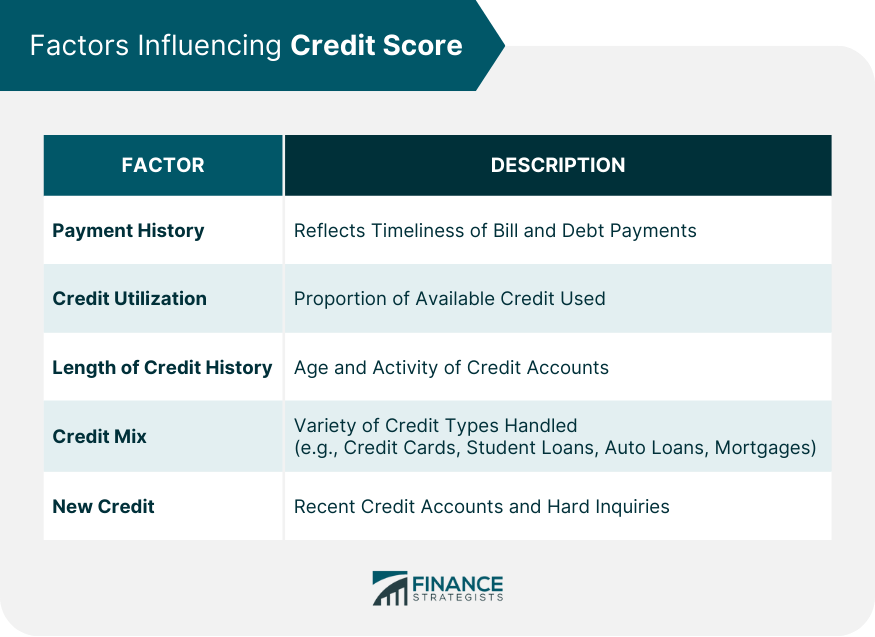

Filing for bankruptcy can significantly impact your credit score, marking it with a serious financial setback. Upon filing, you'll likely see a sharp drop in your score, especially if it was high before. The impact is twofold: immediate and long-term. Bankruptcy stays on your credit report for seven to ten years, depending on whether you filed for Chapter 7 or Chapter 13 bankruptcy, which can hinder your ability to secure loans or credit in the future. While it's possible to rebuild your credit over time, the road to recovery after bankruptcy is often long and challenging. Immediately after declaring bankruptcy, you can expect your credit score to drop sharply. This is especially true if you had a relatively high credit score before bankruptcy. Declaring bankruptcy is seen as a last resort, which is why it has such a strong negative impact. The long-term impact of bankruptcy on your credit score is substantial. Bankruptcies can stay on your credit report for seven to ten years, depending on the type. This lingering mark can make it more difficult for you to obtain credit in the future. The different types of bankruptcy can also have varying impacts. Chapter 7 bankruptcy is generally more damaging to your credit score than Chapter 13 bankruptcy, as it involves liquidating assets and not repaying debts, while Chapter 13 involves a repayment plan. Often referred to as "liquidation bankruptcy," involves selling off your non-exempt assets to repay your creditors. This type of bankruptcy can be quite severe and is usually chosen when there is no realistic possibility of paying off the accumulated debts. Businesses commonly utilize Chapter 11 bankruptcy. It allows businesses to continue operating while restructuring their debts and payment plans under the court's supervision. This form of bankruptcy is complex and often expensive, typically utilized by corporations rather than individuals. Chapter 13 bankruptcy, also known as a "wage earner's plan," enables individuals with regular income to develop a plan to repay all or part of their debts. Debtors propose a repayment plan to make installments to creditors over three to five years. Your credit score is a numerical expression that reflects your creditworthiness and is a crucial element that lenders consider when you apply for loans or credit cards. It's determined based on the information in your credit report, and though different models may weigh factors differently, the general categories that influence your credit score are quite standard. Here are the key factors: Your payment history is one of the most influential factors, typically accounting for 35% of your FICO score. It includes the history of paying your bills on time, late payments, the frequency of these late payments, and any delinquencies or defaults. Lenders look at your payment history to determine if you've been responsible for credit in the past. Late or missed payments can significantly lower your credit score. Credit utilization refers to how much of your available credit you're using. It accounts for approximately 30% of your FICO score. If you're using a high percentage of your available credit, lenders may view this as a sign that you're overextended and may struggle to make repayments. A lower credit utilization ratio is better for your credit score. The length of your credit history makes up about 15% of your FICO score. This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts. Also, it includes the length of time since different accounts were last used. A longer credit history can positively impact your credit score. Credit mix takes into account the different types of credit you're using or have used in the past, including credit cards, student loans, auto loans, and mortgages. It comprises 10% of your FICO score. Lenders like to see a mix of credit, as it shows that you can handle different types of debt. New credit refers to recently opened credit accounts and inquiries into your credit by lenders, also known as "hard" inquiries. Bankruptcy is reported on your credit report as a public record, which can significantly damage your creditworthiness in the eyes of lenders. Once you file for bankruptcy, it appears in the public records section of your credit report. Every account that was included in the bankruptcy will also be marked as such. These notations inform future creditors that the debt has been discharged through bankruptcy. Bankruptcy information can stay on your credit report for up to 10 years for Chapter 7 and up to 7 years for Chapter 13, after which it should automatically fall off your report. The extended presence of bankruptcy on your credit report could limit your access to credit and even affect potential employment and housing opportunities. While bankruptcy's impact on your credit score is severe, it's not the end of the road. With time, patience, and responsible financial management, it's possible to rehabilitate your credit score. Post-bankruptcy, it's crucial to minimize any further negative impacts on your credit score. This can be done by ensuring bills are paid on time, avoiding accumulating further debt, and gradually rebuilding your credit by using a secured credit card or loan. Bankruptcy should be a wake-up call to manage finances more carefully. Budgeting, living within your means, and establishing an emergency fund are crucial steps to avoid future financial crises. The road to credit score rehabilitation is not quick, but with diligent effort, you can start to see improvements within a few years. Small, manageable lines of credit, paid off consistently, can demonstrate to lenders that you are a reliable borrower, helping to gradually rebuild your credit score. The implications of bankruptcy on a credit score are considerable and multifaceted, marking a significant financial downturn. Upon filing, an immediate drop in credit score is almost inevitable. This is followed by long-term effects, with bankruptcy records lingering on your credit report for seven to ten years, affecting future credit applications. The road to recovery is arduous, yet possible, emphasizing responsible financial management, punctual bill payments, and restrained borrowing. This journey, although strenuous, allows the rebuilding of a credit score over time. Crucially, understanding the influence of factors like payment history, credit utilization, length of credit history, credit mix, and new credit on your score is vital for better financial management. Ultimately, while bankruptcy signals a severe financial crisis, it can also serve as a springboard toward more prudent financial habits and eventual credit rehabilitation.How Bankruptcy Affects Credit Score Overview

Understanding Bankruptcy How Bankruptcy Affects Credit Score Overview

Immediate Impact

Long-Term Impact

Comparison of Bankruptcy Types

Chapter 7 Bankruptcy

Chapter 11 Bankruptcy

Chapter 13 Bankruptcy

Factors Influencing Credit Score

Payment History

Credit Utilization

Length of Credit History

Credit Mix

New Credit

Bankruptcy and Credit Report

How Bankruptcy is Reported

Duration of Bankruptcy on Credit Reports

Impact of Bankruptcy on Credit Score

Minimizing Negative Effects

Financial Management After Bankruptcy

Credit Score Rehabilitation

Conclusion

How Bankruptcy Affects Credit Score FAQs

Filing for bankruptcy can significantly reduce your credit score, especially if it was high before filing. The exact impact varies based on various factors, including your credit history, the amount of debt discharged, and the type of bankruptcy filed.

The length of time bankruptcy stays on your credit report depends on the type of bankruptcy. A Chapter 7 bankruptcy can stay on your report for up to 10 years, while a Chapter 13 bankruptcy can stay for up to 7 years. This means it can affect your credit score and your ability to secure new credit for many years.

After bankruptcy, you can mitigate its impact on your credit score by adopting responsible financial habits. These include paying all your bills on time, not accumulating more debt, and gradually rebuilding your credit with a secured credit card or loan.

Both types of bankruptcy significantly affect your credit score, but they do so in different ways. Chapter 7 bankruptcy, which involves liquidating assets to pay off debts, can have a more severe impact than Chapter 13 bankruptcy, which involves setting up a repayment plan.

Yes, while bankruptcy has a severe initial impact, it's possible to rehabilitate your credit score over time. With consistent efforts towards responsible financial management, including making timely payments and not accruing further debt, your credit score can gradually improve.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.