Revocable living trusts are legal entities created to hold and manage assets on behalf of the person who establishes the trust, known as the grantor. As the name suggests, these trusts are both revocable and created during the grantor's lifetime. The grantor has the ability to modify the trust's terms, change beneficiaries, or even terminate the trust entirely. A revocable living trust typically involves three parties: the grantor, who creates and funds the trust; the trustee, who manages the trust assets; and the beneficiaries, who receive the benefits of the trust. In many cases, the grantor may also serve as the trustee, retaining control over the trust assets during their lifetime. The primary purpose of a revocable living trust is to provide an efficient means of managing and transferring assets upon the grantor's death, without the need for probate. Probate is a court-supervised process of administering an individual's estate, which can be time-consuming and costly. By avoiding probate, a revocable living trust can save time and money for the beneficiaries and preserve privacy, as the trust's assets and terms are not subject to public disclosure. Additionally, revocable living trusts can be used for other purposes, such as providing for the management of assets in the event of the grantor's incapacity or ensuring that assets are distributed according to the grantor's wishes upon their death. A revocable living trust is established by the grantor, who transfers assets into the trust and designates a trustee to manage those assets. The trust operates under the terms outlined in a written trust agreement, which governs how the assets are to be managed and distributed to the beneficiaries. The grantor retains the ability to modify the trust's terms, appoint or remove trustees, and add or remove beneficiaries throughout their lifetime. Upon the grantor's death, the trustee is responsible for distributing the trust's assets to the designated beneficiaries according to the trust agreement's terms. This process generally occurs without the need for probate, allowing for a more efficient and private distribution of assets. One of the primary advantages of a revocable living trust is the avoidance of probate. When an individual dies with a will, their estate typically must go through the probate process, which can be time-consuming, expensive, and public. By transferring assets into a revocable living trust, these assets can be distributed directly to the beneficiaries without the need for probate, saving time and money and preserving privacy. Revocable living trusts offer a significant level of privacy, as the details of the trust, including its assets, terms, and beneficiaries, are not subject to public disclosure. In contrast, when an individual dies with a will, their estate becomes a matter of public record, including the assets and the identity of the beneficiaries. For individuals who value privacy, a revocable living trust can be an attractive estate planning option. Revocable living trusts offer considerable flexibility, as the grantor has the ability to modify the trust's terms or terminate the trust entirely during their lifetime. This allows the grantor to adapt the trust to changing circumstances or revise their estate planning goals. Additionally, because the grantor can serve as the trustee, they can retain control over the trust assets and make decisions about their management. A revocable living trust can provide for the ongoing management of assets, both during the grantor's lifetime and after their death. By appointing a trustee to manage the trust assets, the grantor can ensure that their financial affairs are handled professionally and in accordance with their wishes. This can be particularly beneficial in the event of the grantor's incapacity, as the trustee can seamlessly step in and manage the assets without the need for a court-appointed guardian or conservator. While revocable living trusts do not provide significant tax advantages during the grantor's lifetime, as the trust assets are still considered part of the grantor's taxable estate, they can offer certain estate tax benefits upon the grantor's death. For example, a properly structured trust can help married couples take full advantage of the federal estate tax exemption by creating a "credit shelter trust" or "bypass trust," which can ultimately result in lower estate taxes for the beneficiaries. The costs associated with establishing and administering a revocable living trust can be higher than those associated with a simple will. These costs may include legal fees, trustee fees, and ongoing administrative expenses. While the potential benefits of a revocable living trust may outweigh these costs for some individuals, it is important to carefully consider the financial implications of establishing a trust. Revocable living trusts can be more complex than other estate planning tools, such as a will, and may require more time and effort to establish and maintain. The trust agreement must be carefully drafted to ensure that it accurately reflects the grantor's wishes and complies with applicable laws and regulations. Additionally, the ongoing administration of the trust, including the management of assets and recordkeeping, can be more involved than the administration of a simple will. For a revocable living trust to be effective in avoiding probate and providing other benefits, it must be properly funded with the grantor's assets. This process can be time-consuming and may require the re-titling of assets, such as real estate, bank accounts, and investment accounts, in the name of the trust. If the trust is not fully funded, the grantor's estate may still be subject to probate for any assets that were not transferred to the trust. Unlike certain types of irrevocable trusts, revocable living trusts do not provide asset protection for the grantor. Because the grantor retains control over the trust and the ability to modify its terms, the trust assets are still considered part of the grantor's estate and can be reached by creditors or subject to legal judgments. While a revocable living trust can offer certain estate tax benefits, it does not provide significant income tax advantages during the grantor's lifetime. The grantor is generally responsible for paying taxes on the trust's income, and the trust assets are still considered part of the grantor's taxable estate. One of the first steps in creating a revocable living trust is selecting a trustee. The trustee is responsible for managing the trust assets and carrying out the terms of the trust agreement. The grantor may choose to serve as the trustee during their lifetime, appoint a trusted friend or family member, or select a professional trustee, such as a bank or trust company. The next step in establishing a revocable living trust is identifying the assets that will be transferred to the trust. These assets may include real estate, bank accounts, investment accounts, and other personal property. It is important to carefully consider which assets should be included in the trust to achieve the grantor's estate planning objectives. The trust agreement is the legal document that outlines the terms of the revocable living trust and governs how the assets are to be managed and distributed to the beneficiaries. The trust agreement should be carefully drafted by an experienced estate planning attorney to ensure that it accurately reflects the grantor's wishes and complies with applicable laws and regulations. Once the trust agreement has been drafted, the grantor must transfer the identified assets to the trust. This process, known as "funding the trust," may require the re-titling of assets, such as real estate, bank accounts, and investment accounts, in the name of the trust. Properly funding the trust is essential to ensure that the trust achieves its intended benefits, such as avoiding probate and providing for the management of assets. The trustee is responsible for managing the trust assets in accordance with the terms of the trust agreement and applicable laws. This may include investing the trust assets, paying the grantor's expenses, and distributing income or principal to the beneficiaries as directed by the trust agreement. The trustee also has a fiduciary duty to act in the best interests of the beneficiaries and to preserve and protect the trust assets. Upon the grantor's death, the trustee is responsible for distributing the trust's assets to the designated beneficiaries according to the terms of the trust agreement. This process generally occurs without the need for probate, allowing for a more efficient and private distribution of assets. The trustee may also be responsible for paying any debts or expenses of the grantor's estate and filing any required tax returns. A revocable living trust typically terminates upon the death of the grantor or upon the occurrence of a specified event outlined in the trust agreement, such as the distribution of all trust assets to the beneficiaries. At this point, the trustee is responsible for finalizing any remaining trust administration tasks and ensuring that the trust's assets have been properly distributed and accounted for. A revocable living trust is a flexible and powerful estate planning tool that can provide numerous benefits, such as avoiding probate, preserving privacy, and providing for the ongoing management of assets. However, these trusts also come with potential drawbacks, including cost, complexity, and the need for ongoing administration. Understanding how revocable living trusts work, the process of creating and funding a trust, and the advantages and disadvantages of these arrangements can help individuals make informed decisions about whether a revocable living trust is the right choice for their estate planning needs. Consulting with an experienced estate planning attorney is essential to ensure that a revocable living trust is properly established and administered in accordance with the grantor's wishes and applicable laws.What Are Revocable Living Trusts?

How Revocable Living Trusts Work

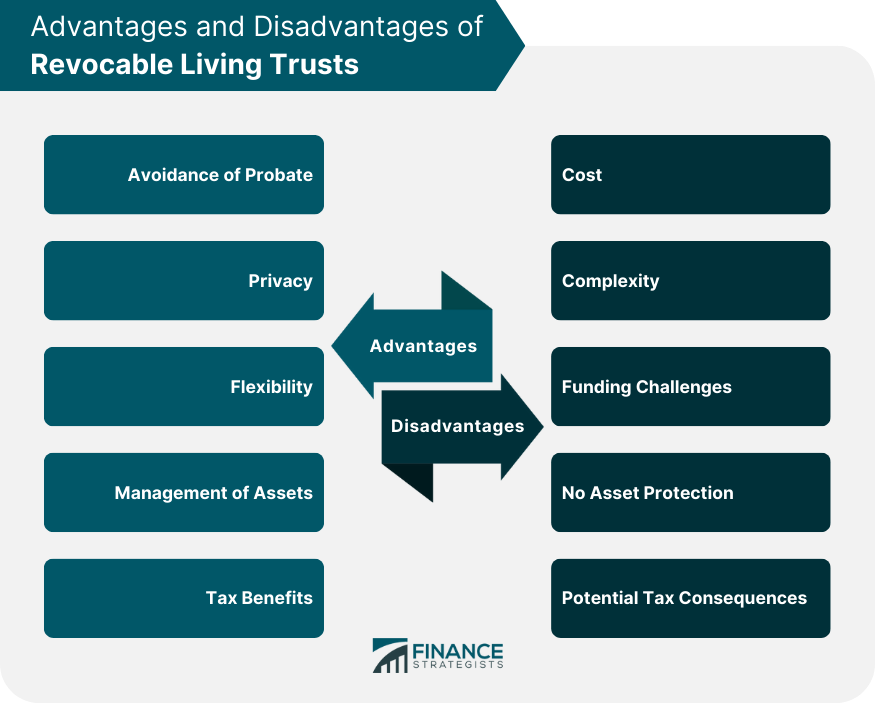

Advantages of Revocable Living Trusts

Avoidance of Probate

Privacy

Flexibility

Management of Assets

Tax Benefits

Disadvantages of Revocable Living Trusts

Cost

Complexity

Funding Challenges

No Asset Protection

Potential Tax Consequences

Creating a Revocable Living Trust

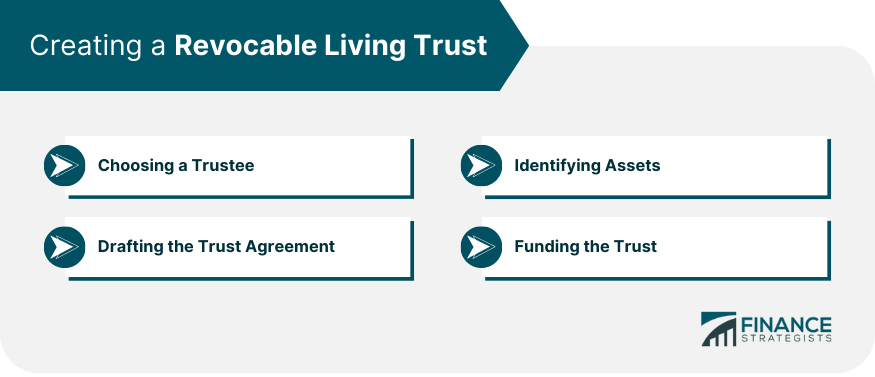

Choosing a Trustee

Identifying Assets

Drafting the Trust Agreement

Funding the Trust

Administration of Revocable Living Trusts

Duties of the Trustee

Distribution of Assets

Termination of the Trust

Bottom Line

Revocable Living Trusts FAQs

A revocable living trust is a legal arrangement where you transfer your assets to a trust that you can change or dissolve during your lifetime.

A revocable living trust can help avoid probate, protect privacy, provide flexibility, manage assets, and potentially reduce estate taxes.

The trustee can be anyone you choose, including yourself, a family member, or a professional trustee.

You can fund a revocable living trust by transferring assets such as real estate, bank accounts, and investments into the trust.

Disadvantages can include the cost and complexity of setting up the trust, potential funding challenges, no asset protection, and potential tax consequences.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.