Retirement tax minimization strategies are financial planning techniques aimed at reducing tax liabilities during retirement. These strategies help retirees preserve more of their hard-earned savings and create a more secure retirement. Tax planning is crucial for a comfortable retirement because taxes can significantly impact a retiree's income and assets. By implementing effective tax minimization strategies, retirees can maintain a higher standard of living and protect their wealth for future generations. Common tax minimization strategies include maximizing contributions to tax-advantaged retirement accounts, tax-efficient investing, and income shifting. These strategies help retirees save on taxes both before and after retirement, thus optimizing their retirement income. Maximizing contributions to tax-advantaged retirement accounts is a key pre-retirement tax minimization strategy, as these accounts provide tax benefits that can help individuals save more for retirement. 401(k) and 403(b) plans are employer-sponsored retirement accounts that offer significant tax advantages. By contributing to these accounts, individuals can reduce their taxable income and defer taxes on investment earnings until retirement. Traditional and Roth IRAs are individual retirement accounts that offer different tax benefits. Traditional IRAs provide tax-deductible contributions and tax-deferred growth, while Roth IRAs offer tax-free growth and withdrawals in retirement. Health Savings Accounts (HSAs) are tax-advantaged accounts used to save for medical expenses. By contributing to an HSA, individuals can reduce their taxable income, enjoy tax-free growth, and make tax-free withdrawals for qualified medical expenses. Tax-efficient investing involves selecting investments that generate lower tax liabilities. By adopting tax-efficient investing strategies, individuals can potentially increase their after-tax returns and accumulate more wealth for retirement. An asset location strategy involves strategically placing investments in taxable or tax-advantaged accounts based on their tax efficiency. By holding tax-inefficient investments in tax-advantaged accounts, investors can reduce their overall tax burden. Tax-loss harvesting is the practice of selling underperforming investments at a loss to offset capital gains taxes. By strategically realizing losses, investors can lower their tax liability and potentially enhance their overall portfolio returns. Low-turnover investments, such as index funds and exchange-traded funds (ETFs), generate fewer taxable events due to their passive management. By investing in low-turnover funds, individuals can minimize capital gains taxes and potentially increase their after-tax returns. Income shifting and tax deductions are strategies that help individuals reduce their taxable income, thus lowering their tax liabilities and increasing their retirement savings. Spousal IRA contributions allow working spouses to contribute to a non-working spouse's IRA, potentially doubling the couple's tax-advantaged retirement savings. This strategy can help couples reduce their taxable income and save more for retirement. Self-employed individuals can take advantage of various business deductions to reduce their taxable income. By claiming eligible business expenses, self-employed taxpayers can lower their tax liabilities and increase their retirement savings. Strategic withdrawal plans help retirees minimize taxes by efficiently managing withdrawals from their retirement accounts, thus maximizing their retirement income. Required Minimum Distributions (RMDs) are mandatory withdrawals from traditional IRAs and 401(k) accounts that start at age 72. By understanding RMD rules and planning withdrawals accordingly, retirees can minimize taxes and avoid penalties. Balancing withdrawals from taxable, tax-deferred, and tax-free accounts allows retirees to manage their tax liabilities. By strategically withdrawing from different account types, retirees can minimize taxes and optimize their retirement income. Roth IRA conversions involve moving funds from a traditional IRA to a Roth IRA, and paying taxes on the conversion. By converting funds strategically, retirees can potentially minimize taxes and enjoy tax-free withdrawals in retirement. Understanding the taxation of Social Security benefits is essential for retirees to minimize their tax liabilities and maximize their retirement income. Social Security benefits may be partially taxable, depending on a retiree's income level. By understanding the tax implications, retirees can plan their income sources and withdrawals to minimize taxes on their benefits. The timing of Social Security benefits claims can affect the taxation of benefits and the overall retirement income. By strategically deciding when to claim benefits, retirees can optimize their income and reduce taxes. Tax-efficient charitable giving strategies allow retirees to support their favorite causes while minimizing taxes on their retirement income. Qualified Charitable Distributions (QCDs) are tax-free withdrawals from an IRA made directly to a qualified charity. By using QCDs, retirees can satisfy their RMDs, lower their taxable income, and support their favorite causes. Donor-advised funds are charitable giving vehicles that offer tax benefits for contributions. By contributing to a donor-advised fund, retirees can receive an immediate tax deduction and recommend grants to their preferred charities over time. Trusts can be an effective tool for tax minimization and estate planning, allowing retirees to transfer assets to their heirs while minimizing taxes. An Irrevocable Life Insurance Trust (ILIT) is a trust that holds a life insurance policy, removing the policy proceeds from the grantor's taxable estate. By using an ILIT, retirees can provide liquidity for estate taxes and protect their assets for their heirs. A Charitable Remainder Trust (CRT) is a trust that pays income to beneficiaries for a specified period and then donates the remaining assets to a charity. With a CRT, retirees can receive income during their lifetime, reduce taxes, and support their favorite causes. Gifting strategies help retirees transfer wealth to their heirs while minimizing gift and estate taxes. It allows individuals to gift a certain amount each year to any number of recipients without incurring gift tax. By utilizing the annual exclusion, retirees can transfer wealth to their heirs and reduce their taxable estate. It is the total amount an individual can gift during their lifetime without incurring gift tax. By strategically using the exemption, retirees can transfer significant wealth to their heirs and minimize estate taxes. The basis step-up rules for inherited assets allow heirs to receive a step-up in the cost basis of the assets, potentially reducing capital gains taxes. By understanding and taking advantage of these rules, retirees can minimize taxes for their heirs. Retirement tax minimization strategies aim to reduce tax liabilities and create a secure retirement. They are crucial for retirees to reduce their tax liabilities and protect their retirement income. By implementing pre-retirement strategies such as maximizing contributions to tax-advantaged retirement accounts, tax-efficient investing, and income shifting, individuals can reduce their taxable income and optimize their retirement savings. Post-retirement strategies such as strategic withdrawal plans, understanding Social Security benefits taxation, tax-efficient charitable giving, and estate and legacy planning can help retirees manage their taxes and create a more secure retirement. It is important to regularly review and update these strategies with the help of a tax professional or financial planner to ensure their effectiveness and adapt to changing circumstances. Staying informed about tax laws and regulations is also crucial for retirees to maintain their tax minimization strategies and continue to optimize their retirement income.What Are Retirement Tax Minimization Strategies?

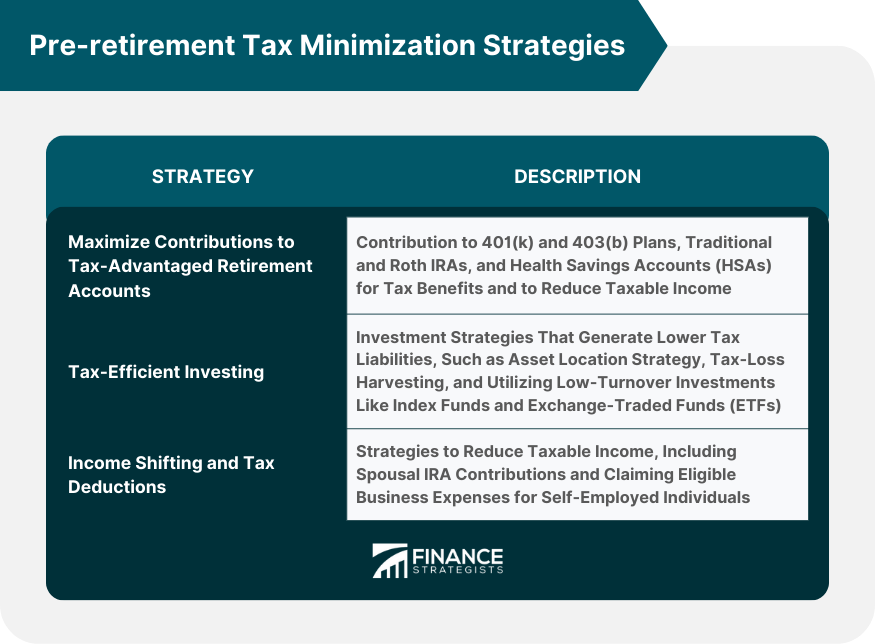

Pre-retirement Tax Minimization Strategies

Maximize Contributions to Tax-Advantaged Retirement Accounts

401(k) and 403(b) Plans

Traditional and Roth IRAs

Health Savings Accounts (HSAs)

Tax-Efficient Investing

Asset Location Strategy

Tax-Loss Harvesting

Utilizing Low-Turnover Investments

Income Shifting and Tax Deductions

Spousal IRA Contributions

Business Deductions for Self-Employed Individuals

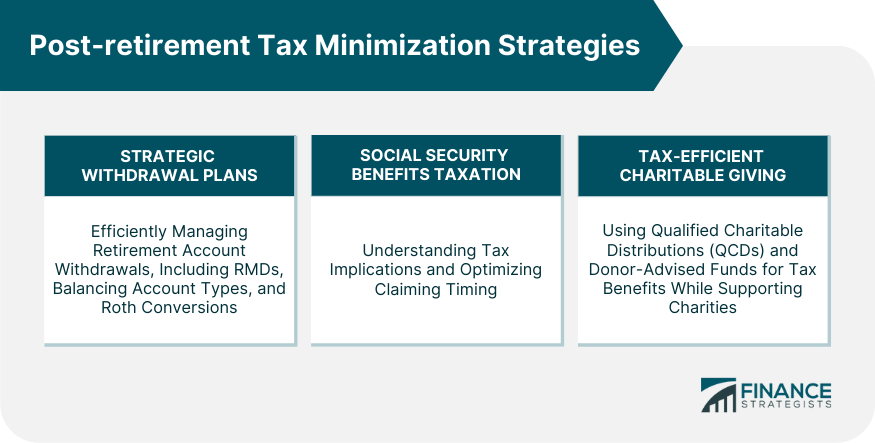

Post-retirement Tax Minimization Strategies

Strategic Withdrawal Plans

Traditional IRA and 401(k) Required Minimum Distributions (RMDs)

Balancing Withdrawals from Taxable, Tax-Deferred, and Tax-Free Accounts

Roth IRA Conversions

Social Security Benefits Taxation

Understanding the Tax Implications

Timing of Social Security Benefits Claiming

Tax-Efficient Charitable Giving

Qualified Charitable Distributions (QCDs)

Donor-Advised Funds

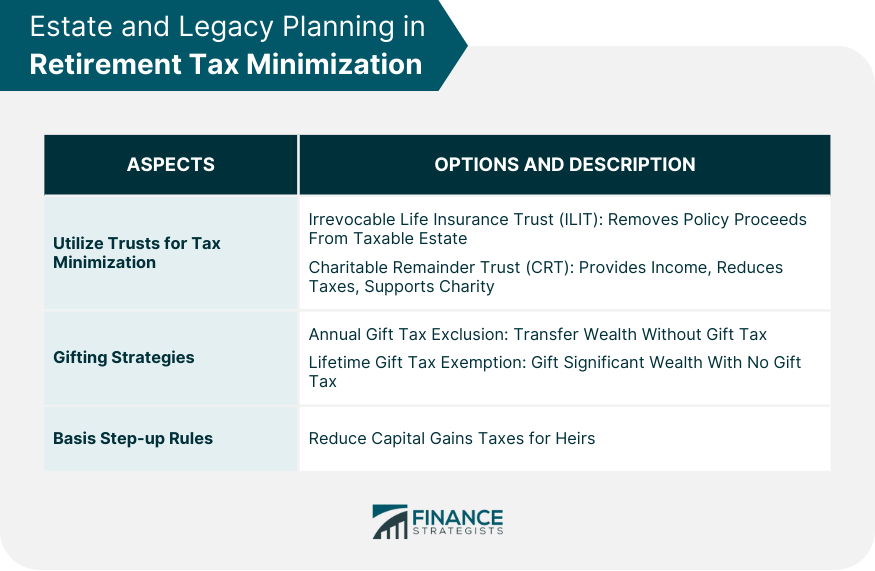

Estate and Legacy Planning in Retirement Tax Minimization

Utilizing Trusts for Tax Minimization

Irrevocable Life Insurance Trust (ILIT)

Charitable Remainder Trust (CRT)

Gifting Strategies

Annual Gift Tax Exclusion

Lifetime Gift Tax Exemption

Basis Step-Up Rules for Inherited Assets

Final Thoughts

Retirement Tax Minimization Strategies FAQs

Key pre-retirement tax minimization strategies include maximizing contributions to tax-advantaged retirement accounts like 401(k)s, 403(b)s, traditional and Roth IRAs, and Health Savings Accounts (HSAs); adopting tax-efficient investing practices like asset location, tax-loss harvesting, and utilizing low-turnover investments; and leveraging income shifting and tax deductions like spousal IRA contributions and business deductions for self-employed individuals.

Post-retirement tax minimization strategies for managing withdrawals involve implementing strategic withdrawal plans, such as taking required minimum distributions (RMDs) from traditional IRAs and 401(k)s, balancing withdrawals from taxable, tax-deferred, and tax-free accounts, and considering Roth IRA conversions to optimize income and reduce taxes.

Social Security benefits taxation is an important aspect of retirement tax minimization strategies. Understanding the tax implications of benefits and strategically timing their claiming can help retirees optimize their income and minimize taxes on Social Security benefits.

Retirees can use tax-efficient charitable giving methods, such as qualified charitable distributions (QCDs) from IRAs and contributions to donor-advised funds, as part of their retirement tax minimization strategies. These methods allow retirees to support their favorite causes while potentially reducing taxes on their retirement income.

Working with tax professionals or financial planners is essential for navigating the complexities of retirement tax planning. They can help identify and implement appropriate tax minimization strategies tailored to each individual's situation, ensure regular reviews and updates of these strategies, and assist retirees in staying informed about changing tax laws and regulations.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.