Pension income planning is the process of making informed decisions about managing and allocating retirement resources to ensure financial stability and sustainability throughout one's retirement years. Pension income planning involves analyzing different sources of retirement income, such as social security benefits, pension plans, personal savings, and investments, and creating a strategic plan to maximize these resources. It requires individuals to evaluate their financial needs, goals, and risk tolerance in retirement, as well as consider various factors such as life expectancy, inflation, and tax implications. The importance of pension income planning cannot be overstated, as it plays a crucial role in ensuring a comfortable and worry-free retirement. Firstly, pension income planning helps retirees manage their expenses and maintain their desired lifestyle without the risk of outliving their resources. It also enables them to adjust their spending patterns and investment strategies as their circumstances and market conditions change. Additionally, effective pension income planning can minimize tax liabilities and protect retirement assets from potential creditors, thus preserving wealth for future generations. A defined benefit plan is a type of employer-sponsored retirement plan in which the employer promises to pay a specified benefit to employees upon retirement. Under a defined benefit plan, the employer calculates the retirement benefit based on a predetermined formula that usually factors in the employee's years of service, age, and salary. The employer then contributes to the plan and assumes the investment risk, meaning that the employee is not responsible for investment decisions or performance. Benefits under a defined benefit plan are generally paid out as a lifetime annuity, providing a steady and predictable stream of income in retirement. A defined contribution plan is another type of employer-sponsored retirement plan that allows employees to make contributions to their individual accounts. Unlike defined benefit plans, the retirement benefit in a defined contribution plan is not predetermined. Instead, the employee's retirement income depends on the contributions made and the investment performance of their account. Common examples of defined contribution plans include 401(k) and 403(b) plans. Employees typically have control over their investment choices and bear the investment risk. Upon retirement, the accumulated balance can be withdrawn as a lump sum, converted to an annuity, or used for systematic withdrawals, depending on the plan's provisions and the retiree's preferences. A cash balance plan is a hybrid pension plan that combines features of both defined benefit and defined contribution plans. In a cash balance plan, each employee has an individual account that is credited with a specified percentage of their salary, known as the pay credit, and an interest credit based on a predetermined rate. The employer is responsible for funding the plan and bears the investment risk, as in defined benefit plans. However, unlike traditional defined benefit plans, the employee's retirement benefit is determined by the account balance, similar to defined contribution plans. Upon retirement or separation from the employer, the employee can receive the account balance as a lump sum or convert it to an annuity. Estimating one's retirement income needs is a crucial step in pension income planning. To determine retirement income needs, factors such as desired lifestyle, life expectancy, and anticipated expenses should be taken into account. A common rule of thumb is to aim for approximately 70-80% of pre-retirement income to maintain a similar lifestyle during retirement. However, this may vary based on individual circumstances and preferences. Retirees should also account for factors such as inflation and potential changes in expenses, such as increased healthcare costs or reduced mortgage payments. Identifying all potential sources of income during retirement is essential to develop a comprehensive pension income plan. Common sources of retirement income include social security benefits, employer-sponsored pension plans, personal savings, and investments. In addition to these traditional sources, retirees might also consider alternative income streams such as rental income, part-time work, or income from a small business. It is essential to accurately estimate the amount and timing of each income source to develop a realistic and sustainable retirement income plan. After determining retirement income needs and identifying all potential income sources, it is essential to evaluate if there are any income gaps. An income gap occurs when the projected retirement income falls short of the estimated retirement expenses. If an income gap exists, individuals may need to reassess their retirement goals, increase savings, or adjust their investment strategies to bridge the gap. Alternatively, they might consider delaying retirement, working part-time during retirement, or finding ways to reduce expenses to ensure financial stability throughout their retirement years. Choosing the right pension payout option is a critical decision that can significantly impact a retiree's financial security. Common payout options include lump-sum payments, annuities, or systematic withdrawals. Lump-sum payments involve receiving the entire pension balance at once, which provides flexibility but also exposes the retiree to market risks and the possibility of outliving their savings. Annuities, on the other hand, provide a guaranteed stream of income for life or a specified period, offering stability but less flexibility. Systematic withdrawals allow retirees to draw a fixed amount from their pension accounts regularly, providing a balance between flexibility and stability. The optimal payout option depends on factors such as the retiree's financial needs, risk tolerance, and life expectancy. The timing of claiming social security benefits can significantly impact the amount of income received during retirement. Retirees can start claiming benefits as early as age 62, but the longer they wait (up to age 70), the higher the monthly benefit will be. Claiming benefits early can provide immediate income but results in a permanently reduced benefit. Conversely, delaying benefits increases the monthly amount but might require using personal savings to cover expenses in the meantime. It is crucial to consider factors such as life expectancy, financial needs, and other income sources when deciding the optimal claiming strategy. A well-crafted investment allocation and withdrawal strategy can help retirees manage their retirement assets effectively and minimize the risk of outliving their savings. Investment allocation involves distributing assets across various investment types (stocks, bonds, cash) based on an individual's risk tolerance, financial goals, and time horizon. During retirement, individuals should gradually shift their investment allocation towards more conservative investments to preserve capital and reduce volatility. Withdrawal strategies involve determining the optimal amount and sequence of withdrawals from different accounts to maximize retirement income and minimize taxes. Retirees should carefully monitor their withdrawal rates and adjust them as needed to ensure the sustainability of their retirement assets. Longevity risk refers to the possibility of outliving one's retirement savings. To manage longevity risk, retirees can employ various strategies, such as annuitizing a portion of their assets, investing in longevity insurance, or adopting a more conservative withdrawal rate from their retirement accounts. Annuitizing a portion of assets can provide a guaranteed income stream for life, reducing the risk of outliving savings. Longevity insurance, also known as a deferred income annuity, involves purchasing an annuity that starts paying benefits at a later age, such as 85, providing a safety net in case of an unexpectedly long life. Adopting a more conservative withdrawal rate from retirement accounts can help preserve assets and extend their lifespan. It is essential to periodically reassess one's financial situation and adjust strategies as needed to manage longevity risk effectively. The tax treatment of pension income varies depending on the type of pension plan and the payout option chosen. Generally, pension income from a defined benefit plan or a cash balance plan is taxable as ordinary income, whereas withdrawals from a defined contribution plan may be taxed differently based on the type of contributions made (pre-tax or after-tax). Withdrawals from a traditional 401(k) or IRA, which are funded with pre-tax contributions, are taxed as ordinary income. On the other hand, withdrawals from a Roth 401(k) or Roth IRA, which are funded with after-tax contributions, are tax-free as long as certain conditions are met. It is crucial to understand the tax implications of different pension types and payout options to make informed decisions and minimize tax liabilities. Tax-efficient pension income planning involves structuring retirement income and withdrawals to minimize tax liabilities and maximize after-tax income. Strategies for tax-efficient pension income planning include strategically timing withdrawals from different accounts, converting traditional retirement accounts to Roth accounts, and utilizing tax-advantaged investment vehicles. By timing withdrawals from different accounts, retirees can control their taxable income and potentially reduce their tax rate. Converting traditional retirement accounts to Roth accounts can result in tax-free withdrawals during retirement, although taxes must be paid on the converted amount. Utilizing tax-advantaged investment vehicles, such as municipal bonds or tax-managed mutual funds, can help reduce the tax impact on investment income. It is essential to consult with a tax professional or financial advisor to develop a tax-efficient pension income plan tailored to one's unique circumstances. Pension income planning is a crucial process for managing retirement resources to ensure financial stability and sustainability in one's retirement years. It involves analyzing different sources of retirement income, such as social security benefits, pension plans, personal savings, and investments, and creating a strategic plan to maximize these resources. There are three main types of pension plans: defined benefit, defined contribution, and cash balance plans. Individuals should evaluate their financial needs, goals, and risk tolerance in retirement and consider various factors such as life expectancy, inflation, and tax implications to choose the best plan for their circumstances. To optimize pension income, retirees should conduct a retirement income needs assessment, identify all potential income sources, evaluate income gaps, and adopt pension payout options, social security claiming strategies, investment allocation and withdrawal strategies, and longevity risk management strategies. Pension income planning is a comprehensive and ongoing process that requires careful consideration and planning to ensure a comfortable and worry-free retirement. Overview of Pension Income Planning

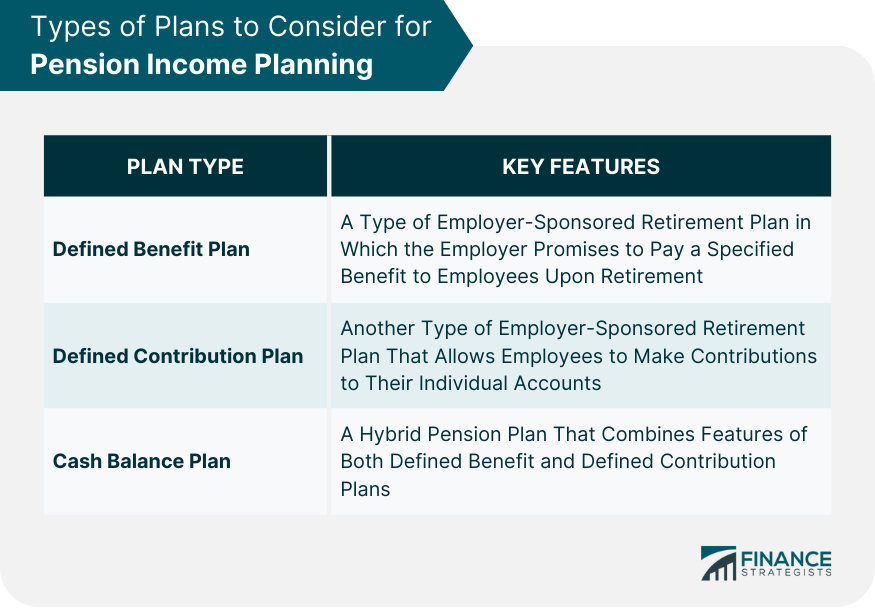

Types of Plans to Consider for Pension Income Planning

Defined Benefit Plan

Defined Contribution Plan

Cash Balance Plan

Needs Assessment as Part of Pension Income Planning

Determining Retirement Income Needs

Identifying Income Sources

Evaluating Income Gaps

Optimization Strategies for Pension Income Planning

Pension Payout Options

Social Security Claiming Strategies

Investment Allocation and Withdrawal Strategies

Longevity Risk Management Strategies

Taxation as Part of Pension Income Planning

Tax Treatment of Different Types of Pensions

Tax-Efficient Pension Income Planning

Conclusion

Pension Income Planning FAQs

Pension income planning involves creating a strategy to ensure a steady stream of income during retirement from pension plans.

Several factors should be considered when creating a Pension Income Planning strategy, such as retirement goals, lifestyle preferences, expected expenses, investment risk tolerance, and healthcare needs.

You can maximize your retirement income by contributing more to your pension plan, selecting a suitable pension plan, minimizing investment fees, and utilizing tax-efficient retirement income options.

Some risks associated with Pension Income Planning include investment risk, inflation risk, longevity risk, and interest rate risk, which can affect the amount of retirement income you receive.

Yes, you can make changes to your Pension Income Planning strategy after retirement, but you should proceed with caution, taking into account the potential tax and financial consequences of any modifications.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.