A pension scheme is a structured financial plan designed to provide individuals with a stable income after retirement. These schemes are typically funded through contributions made during the individual’s working years. They act as a safety net for retirees, ensuring a continuous flow of income even after they stop earning a regular salary. The primary purpose of pension schemes is to provide financial security and stability in the post-retirement phase of an individual's life. They are crucial in safeguarding retirees against poverty and maintaining their standard of living. Pension schemes also play a significant role in the broader economy by mobilizing long-term savings for investment purposes. Pension schemes can be broadly categorized into defined benefit plans and defined contribution plans. Defined benefit plans promise a specific payout at retirement, often based on salary and years of service, while defined contribution plans depend on contributions and investment returns. Each type has its own set of rules, benefits, and risks. The funding of pension schemes involves regular contributions from either the employer, the employee, or both. These contributions are typically a percentage of the employee’s salary. The structure of these contributions plays a significant role in determining the final retirement benefits. The calculation of benefits in a pension scheme depends on several factors, including the type of plan, the individual’s salary, years of service, and the contribution structure. Defined benefit plans use a formula to calculate the retirement payout, whereas defined contribution plans rely on the accumulated contributions and investment returns. The management of pension funds is a critical aspect that involves investing contributions to grow the fund over time. This investment is usually handled by professional fund managers who allocate assets across various classes like stocks, bonds, and real estate to achieve growth while managing risk. When it comes to receiving pension benefits, retirees typically have options like lump-sum payments, annuities, or a combination of both. The choice of payout can significantly impact their financial security in retirement. Understanding these options and their implications is crucial for effective retirement planning. Pension schemes provide a reliable source of income in retirement, ensuring that individuals can maintain their lifestyle even when they stop earning a regular income. This financial security is a significant advantage, as it reduces reliance on savings and helps manage living costs in retirement. Many pension schemes offer tax benefits, either at the time of contribution, during the accumulation phase, or at the time of withdrawal. These tax advantages can significantly enhance the value of the retirement fund, making pension schemes an attractive option for retirement savings. In many pension schemes, especially those sponsored by employers, the employer contributes a certain percentage towards the employee’s pension fund. This not only enhances the retirement benefits but also provides an incentive for employees to stay with the company. Some pension schemes offer inflation protection, either through indexed payouts or other mechanisms. This feature helps to ensure that the purchasing power of the retirement income does not diminish over time due to inflation. In many pension schemes, especially defined benefit plans, individuals have little to no control over how their contributions are invested. This lack of control can be a significant drawback for those who prefer to have more say in their investment choices. Pension schemes are susceptible to risks of underfunding or mismanagement. If a pension fund is not managed properly or does not have enough assets to meet its future liabilities, it can lead to reduced payouts for retirees. Pension schemes often have strict rules regarding when and how benefits can be withdrawn. This inflexibility can be a disadvantage, particularly in situations where an individual might need access to funds before retirement due to emergencies or other needs. For employer-sponsored pension plans, the retiree's benefits are often linked to the employer's financial health. If the company faces financial difficulties, it may affect the stability and reliability of the pension benefits. When choosing a pension scheme, it’s essential to carefully evaluate several key factors to ensure that the selected plan aligns with your individual needs and retirement goals. Firstly, the type of pension plan is crucial – whether it’s a defined benefit plan, which offers a guaranteed payout, or a defined contribution plan, where the benefits depend on the investment's performance. Each type has its advantages and implications for retirement income. Additionally, the contribution structure – how much and how often you and potentially your employer contribute – significantly impacts the final pension amount. The investment strategy of the pension fund is another vital consideration. It’s important to assess how the fund is managed, the types of assets it invests in, and its historical performance, as this can affect the growth of your contributions over time. Payout options, such as lump-sum or annuity, and their flexibility should also be considered, as they determine how you receive your benefits upon retirement. Finally, evaluating the pension scheme's overall stability and reputation, which includes looking into its financial health and track record, provides insight into its reliability and the security of your future benefits. Comparing different pension schemes is not just about looking at the potential returns but also understanding the associated risks, fees, and the fine print that could affect your retirement income. Benefits, such as employer contributions and tax advantages, should be weighed against any potential risks, like the volatility of investments or the possibility of the fund underperforming. Fees are another critical aspect to consider, as high management or administrative fees can significantly erode your retirement savings over time. Additionally, the performance history of a pension scheme can give you an idea about its reliability and efficiency in managing investments. This comparison should be thorough and consider your current financial situation, anticipated retirement age, and expected standard of living during retirement. It’s about finding a balance between the potential for growth, the level of risk you’re comfortable with, and the reliability of the scheme. Given the long-term impact and the complexity of pension schemes, consulting with a financial advisor is highly recommended. A professional advisor can offer insights and guidance tailored to your specific financial situation, retirement goals, and risk tolerance. They can help you navigate through the myriad of options available, breaking down complex financial jargon and simplifying the decision-making process. A financial advisor can also assist in projecting your future financial needs, taking into account factors like inflation, healthcare costs, and life expectancy, to ensure that the chosen pension scheme adequately covers your retirement years. Pension schemes are a vital component of retirement planning, offering financial security and stability post-retirement. Whether it's a defined benefit or a defined contribution plan, understanding the nuances of each type is essential. Regular contributions, wise investment strategies, and considering payout options are key to maximizing retirement benefits. While pension schemes offer significant advantages like tax benefits, employer contributions, and inflation protection, it's important to be aware of potential drawbacks such as limited investment control and dependency on the employer's financial health. Making an informed decision requires a thorough comparison of different pension options, considering factors like risks, fees, and performance history. Given the complexity of these decisions, seeking professional financial advice is highly recommended to ensure a pension scheme aligns with personal retirement goals and financial circumstances, securing a stable and comfortable retirement.What Is a Pension Scheme?

Purpose and Importance

Types of Pension Schemes

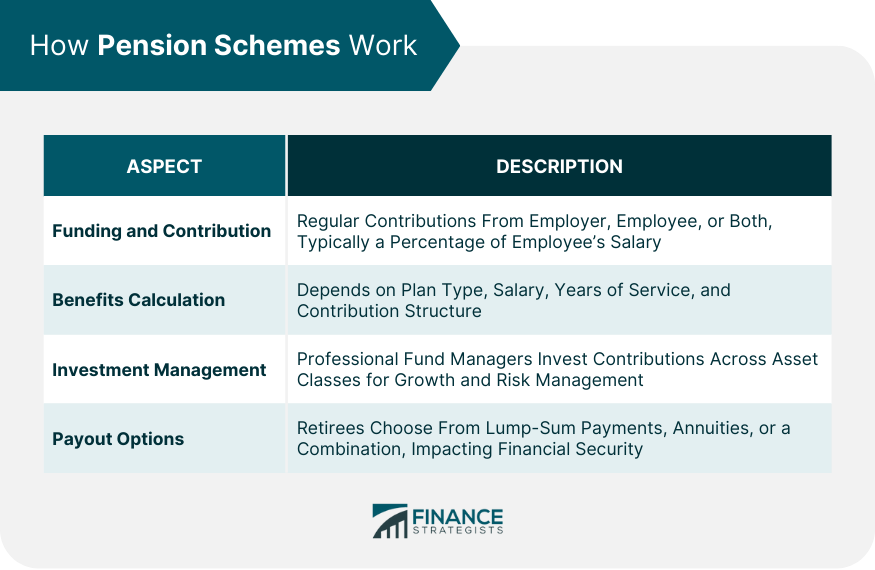

How Pension Schemes Work

Funding and Contribution Structure

Benefits Calculation

Investment Management

Payout Options and Retirement Withdrawals

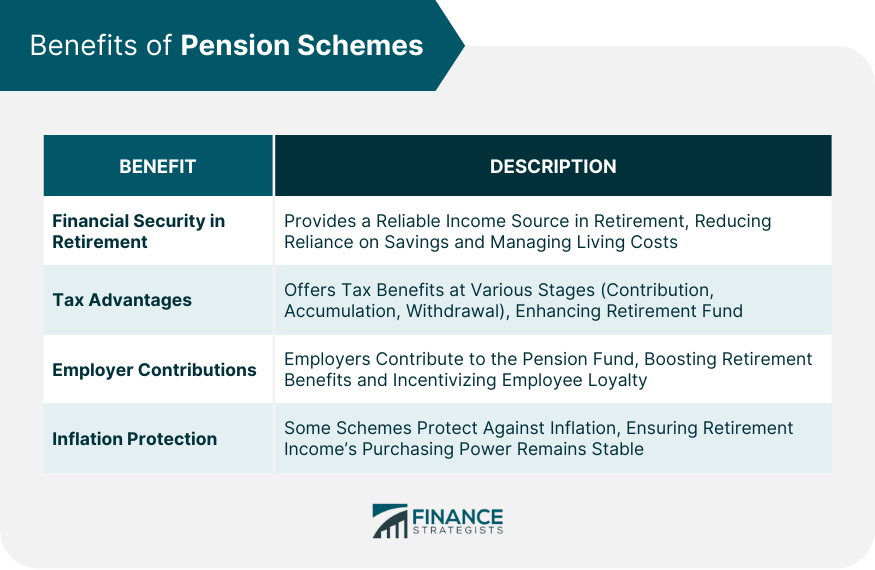

Benefits of Pension Schemes

Financial Security in Retirement

Tax Advantages

Employer Contributions

Inflation Protection

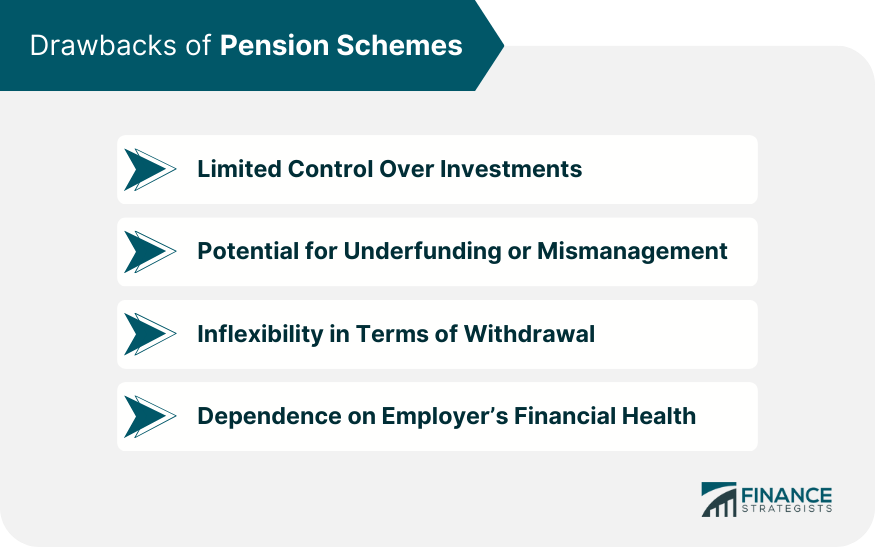

Drawbacks of Pension Schemes

Limited Control Over Investments

Potential for Underfunding or Mismanagement

Inflexibility in Terms of Withdrawal

Dependence on Employer’s Financial Health

Choosing the Right Pension Scheme

Factors to Consider

Comparing Different Pension Options

Seeking Professional Advice

Bottom Line

Pension Scheme FAQs

The main types of pension schemes are defined benefit plans, which offer a guaranteed payout based on salary and years of service, and defined contribution plans, where benefits depend on contributions and investment returns.

Pension schemes are usually funded through regular contributions made by either the employer, the employee, or both, which are then invested to grow over time, providing income during retirement.

Many pension schemes offer tax benefits such as tax-free contributions, tax-deferred growth of investments, and tax-efficient withdrawals, depending on the scheme and local tax laws.

Control over investments varies: Defined benefit plans typically offer little to no control, whereas defined contribution plans often allow more personal choice in investment options.

When selecting a pension scheme, consider factors like the type of plan (defined benefit or contribution), contribution structure, investment strategy, payout options, scheme’s stability and reputation, as well as personal retirement goals and financial needs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.