Bond funds, also known as fixed-income funds, are investment vehicles that pool money from multiple investors to invest in a diversified portfolio of bonds. Bonds, in essence, represent debt instruments issued by governments, municipalities, or corporations to raise capital. When investors purchase bonds, they effectively lend money to the bond issuer in exchange for regular interest payments, usually referred to as coupon payments, and the return of the principal amount at maturity. Bond funds play a crucial role in retirement income planning due to their characteristics that align with retirees' financial objectives. Bond funds help to spread your investment across different types of bonds and issuers, thereby reducing the risk of significant losses. This diversified exposure is crucial, especially during volatile market conditions, and can provide a safety net for your retirement portfolio. One of the primary reasons for including bond funds in a retirement portfolio is their ability to generate regular income. Bonds typically pay interest semi-annually or annually, which can be a steady source of cash flow for retirees. Investors generally consider bonds to be safer investments than stocks. While they may not offer the same growth potential as equities, they do provide a degree of capital preservation, which is important for retirees who cannot afford significant losses. Government bond funds invest in securities issued by the U.S. government and its agencies. These are considered to be among the safest investments, as they are backed by the full faith and credit of the U.S. government. Municipal bond funds invest in bonds issued by states, cities, and other local entities. The interest from these bonds is typically tax-free at the federal level, which can make them attractive for investors in high tax brackets. Corporate bond funds invest in bonds issued by corporations. These funds may offer higher yields than government or municipal bond funds, but they also carry a higher risk. High-yield bond funds invest in bonds that have lower credit ratings and a higher risk of default. While these funds offer potentially higher yields, they are also more volatile and may not be suitable for all investors. International bond funds invest in bonds issued by foreign governments and corporations. These funds offer diversification but also carry risks such as foreign exchange risks and political risks. Inflation-protected bond funds invest in securities that adjust with inflation, helping protect investors' purchasing power. This can be particularly beneficial for retirees who are concerned about inflation eroding their savings. Your age and risk tolerance play a crucial role in determining how much of your portfolio should be allocated to bond funds. The closer you are to retirement, the more you might want to consider shifting towards bonds to help preserve capital and generate income. Asset allocation and diversification are essential strategies to manage risk and optimize returns. A well-diversified portfolio should include a mix of different asset classes, including stocks, bonds, and potentially other investments like real estate. Interest rates have a significant impact on bond prices. When rates rise, bond prices fall, and vice versa. Therefore, it's essential to consider the current interest rate environment and expectations for future rate changes when investing in bond funds. Different types of bond funds have different tax implications. For example, the interest from municipal bonds is typically tax-free at the federal level, which can be beneficial for investors in higher tax brackets. It's important to understand the tax implications of your investments and consider consulting with a tax advisor. Choosing the right bond funds for your retirement income involves evaluating several key factors. These include the fund's track record and performance, the fund manager's expertise, the expense ratio, yield, duration and maturity, and credit quality. Reviewing a fund's past performance can provide insights into how it may perform in the future. However, past performance is not a guarantee of future results, so this should only be one factor in your decision. Consider the fund manager's experience and expertise. A skilled manager with a proven track record can add value to a bond fund. The expense ratio is the cost of owning a fund, and it can eat into your returns over time. Look for funds with lower expense ratios to maximize your potential income. The yield is the income generated by the fund, expressed as a percentage of the investment. A higher yield can mean more income, but it may also come with higher risk. The duration and maturity of a bond fund can impact its sensitivity to interest rate changes. Longer-duration and longer-maturity funds are generally more sensitive to interest rate changes, which can affect your income. The credit quality of the bonds in a fund can impact the fund's risk and return. Higher credit quality bonds are less likely to default, but they may offer lower yields. Choosing the best bond funds for retirement income depends on your individual circumstances and risk tolerance. However, here are a few funds that have been recognized for their solid performance and potential for income. A popular choice for income-focused investors. AGG provides exposure to a broad range of U.S. investment-grade bonds, including government, corporate, and mortgage-backed securities. Its diversification and low expenses make it a solid foundation for any retirement portfolio. Another strong contender. BND aims to track the performance of the Bloomberg Barclays U.S. Aggregate Float Adjusted Index, providing broad exposure to U.S. investment-grade bonds. With a low expense ratio and a history of steady returns, BND can serve as a reliable income generator in retirement. This fund seeks to replicate the performance of the Bloomberg Barclays U.S. Aggregate Bond Index, encompassing a wide array of high-quality U.S. bonds. Its low fees and steady income make it an excellent choice for those seeking reliable returns in their retirement years. It offers a similar strategy to the aforementioned funds, aiming to mirror the performance of the Bloomberg Barclays U.S. Aggregate Bond Index. With its competitive expense ratio and broad exposure to the U.S. bond market, SWAGX has a proven track record of delivering consistent income, making it a worthy addition to a retirement portfolio. Interest Rate Risk: This is the risk that bond prices will fall as interest rates rise. This is particularly relevant for longer-term bonds, which are more sensitive to interest rate changes. Credit Risk: This is the risk that the issuer of a bond will default on their payment obligations. This risk is higher for corporate and high-yield bonds. Inflation Risk: The risk that inflation will erode the purchasing power of your investment returns. Inflation-protected bonds can help mitigate this risk. Liquidity Risk: The risk that you may not be able to sell your bond fund shares at a fair price. Some types of bond funds, particularly those that invest in lower-quality or more obscure bonds, may have higher liquidity risk. Foreign Exchange Risk: Applies to international bond funds. It's the risk that changes in currency exchange rates will affect the value of your investment. Selecting the best bond funds for retirement income requires careful consideration of various factors, such as the fund's performance, the manager's expertise, and risk tolerance. Popular choices for retirement income include the iShares Core U.S. Aggregate Bond ETF, Vanguard Total Bond Market ETF, Fidelity U.S. Bond Index Fund, and Schwab U.S. Aggregate Bond Index Fund (SWAGX) due to their diversified exposure, low costs, and steady income generation. Bond funds can help diversify your portfolio, offer regular income streams, and protect your capital. However, understanding different bond fund types and their risks, including interest rate, credit, and inflation risk, is critical. Lastly, always remember to align your investment choices with your retirement goals and consider consulting with a financial advisor for personalized advice.Overview of Bond Funds

Relevance of Bond Funds for Retirement Income

Diversification Benefits

Regular Income Streams

Potential for Capital Preservation

Understanding the Different Types of Bond Funds

Government Bond Funds

Municipal Bond Funds

Corporate Bond Funds

High-Yield Bond Funds

International Bond Funds

Inflation-Protected Bond Funds

Incorporating Bond Funds Into a Retirement Portfolio

Role of Age and Risk Tolerance

Asset Allocation and Diversification Strategies

Impact of Current and Expected Interest Rates

Tax Considerations

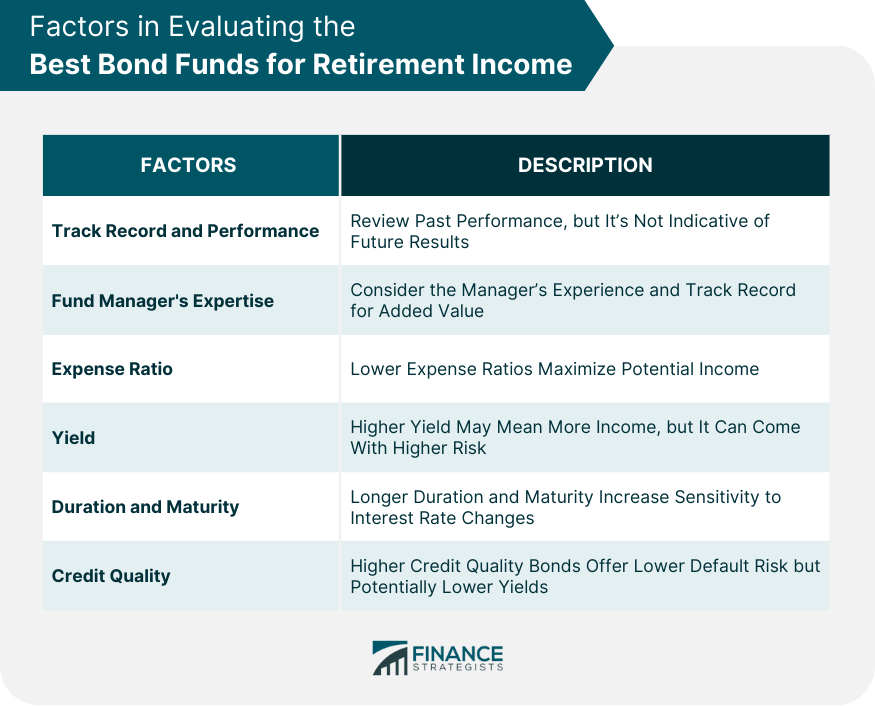

How to Evaluate the Best Bond Funds for Retirement Income

Track Record and Performance

Fund Manager's Expertise

Expense Ratio

Yield

Duration and Maturity

Credit Quality

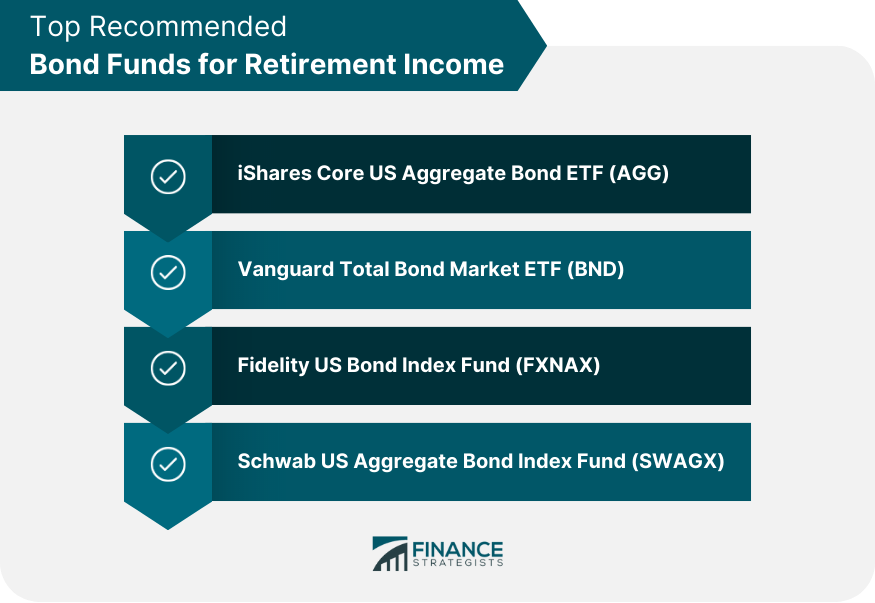

Top Recommended Bond Funds for Retirement Income

iShares Core US Aggregate Bond ETF (AGG)

Vanguard Total Bond Market ETF (BND)

Fidelity US Bond Index Fund (FXNAX)

Schwab US Aggregate Bond Index Fund (SWAGX)

Risks Involved With Investing in Bond Funds for Retirement

Conclusion

Best Bond Funds for Retirement Income FAQs

The best bond funds for retirement income are typically those that offer a solid track record, a skilled fund manager, a low expense ratio, a consistent yield, a reasonable duration and maturity, and good credit quality. They should also fit well with your personal risk tolerance and retirement goals.

The best bond funds for retirement income generate regular income through the interest payments made on the bonds they hold. These interest payments are typically distributed to fund shareholders on a monthly or semi-annual basis.

The best bond funds for retirement income provide diversification by spreading investments across different types of bonds and issuers. This can help reduce risk and provide a more stable income stream, which is particularly important during retirement.

When looking for bond funds to supplement retirement income, consider the iShares Core U.S. Aggregate Bond ETF (AGG), Vanguard Total Bond Market ETF (BND), Fidelity U.S. Bond Index Fund (FXNAX), and Schwab U.S. Aggregate Bond Index Fund (SWAGX). Each of these funds provides broad exposure to a variety of U.S. investment-grade bonds, thus offering diversified portfolios and steady income streams.

When investing in the best bond funds for retirement income, it's important to consider various risks, including interest rate risk, credit risk, inflation risk, liquidity risk, and foreign exchange risk (for international bond funds). Understanding these risks can help you make more informed investment decisions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.