403(b) withdrawal options refer to the various ways a participant in a 403(b) retirement plan can access their saved funds. These options, which include regular distributions, early distributions, loans, hardship withdrawals, and rollovers, serve the purpose of providing financial flexibility, especially during retirement or in times of financial hardship. They are crucial for readers, particularly those who participate in a 403(b) plan, as these options directly impact their financial and retirement planning strategies. However, each option comes with potential tax implications and other consequences, underscoring the importance of careful decision-making. Understanding 403(b) withdrawal options, therefore, forms a significant part of successful retirement planning and financial management. Understanding how 403(b) withdrawal options work is crucial to making informed decisions about your retirement savings. Normal distributions from a 403(b) plan can begin without penalty once the account holder reaches the age of 59 ½. At this point, withdrawals are subject to ordinary income tax but are not subject to the 10% early withdrawal penalty. Early distributions refer to withdrawals made before the age of 59 ½. These distributions are not only subject to ordinary income tax, but they also often incur a 10% early withdrawal penalty unless they qualify for an exception. RMDs are the minimum amounts that retirement plan account owners must withdraw annually starting with the year they reach 73. The RMD rules are designed to ensure that savers don't just accumulate retirement accounts but actually spend them in their retirement. Some 403(b) plans allow for loans or hardship withdrawals. Loans must be repaid within a specified period, typically five years. Hardship withdrawals are allowed for immediate and heavy financial need, according to IRS guidelines. Account holders can choose to roll over their 403(b) funds into another eligible retirement account such as a 401(k) or an IRA. This allows for continued tax-deferred growth of the retirement funds. The flexibility of 403(b) withdrawal options offers several benefits. Having various withdrawal options provides flexibility and accessibility, allowing individuals to tailor their retirement income to their specific needs and circumstances. Rollovers allow for the continued tax-deferred growth of retirement funds, which can enhance the overall value of your retirement savings. Hardship withdrawals can provide financial relief in emergencies, ensuring that individuals can access their funds when they need them the most. If you take out a loan from your 403(b) account, the repayments, including interest, go back into your account, essentially paying yourself back. While 403(b) withdrawal options offer flexibility, they also come with potential drawbacks. Early distributions before age 59 ½ typically incur a 10% early withdrawal penalty, which can significantly reduce your retirement savings. Large withdrawals could push an individual into a higher tax bracket for that year, resulting in a higher tax obligation. Early distributions, loans, and hardship withdrawals can significantly reduce the overall value of your retirement savings and impact your long-term financial security. If withdrawals are too large or start too early, there is a risk of outliving retirement savings, leaving individuals financially vulnerable in their later years. Successfully managing 403(b) withdrawal options often involves strategic planning and understanding the implications of each choice. Each withdrawal option carries different tax implications, including potential income tax and early withdrawal penalties. Understanding these can help minimize tax obligations and avoid unexpected tax bills. Having a solid retirement income plan can help ensure that withdrawals are appropriately sized and timed to provide a steady income stream throughout retirement. Given the complexity of tax rules and retirement planning, seeking advice from a financial advisor can be beneficial. They can provide personalized guidance based on your unique circumstances and retirement goals. Understanding the legal aspects associated with 403(b) withdrawal options is critical to avoid penalties and ensure compliance with regulations. The IRS has specific guidelines governing early distributions, loans, hardship withdrawals, and rollovers from 403(b) accounts. These guidelines outline the qualifying circumstances for each withdrawal option, potential penalties, and tax implications. The Employee Retirement Income Security Act (ERISA) governs most retirement plans, including some 403(b) plans. ERISA stipulates minimum standards for retirement plans and protects the interests of employee benefit plan participants and their beneficiaries. State laws can also affect 403(b) withdrawal options. Some states may offer additional protections for retirement accounts in the event of bankruptcy or lawsuits. It's important to understand the state-specific regulations that apply to your retirement savings. Loans and hardship withdrawals from 403(b) plans can provide needed funds in emergencies, but they also have important considerations. Some 403(b) plans permit loans. When you borrow from your 403(b), you're required to pay interest on the loan, and the repayment goes back into your account. However, if you fail to repay the loan, it's considered a distribution and is subject to taxes and possibly penalties. Also, if you leave your job, the loan often becomes due much sooner. Hardship withdrawals from a 403(b) plan are subject to specific IRS criteria, including medical expenses, home purchase, education costs, eviction prevention, funeral expenses, and home repairs. However, hardship withdrawals permanently reduce your retirement savings and are subject to income tax and potentially an early withdrawal penalty. Understanding your 403(b) withdrawal options is crucial for effective retirement planning. With options such as regular distributions, early distributions, loans, hardship withdrawals, and rollovers, you have the flexibility to manage your retirement savings according to your specific needs. Withdrawal options for 403(b) plan offer benefits like accessibility and tax-deferred growth but come with drawbacks such as penalties, tax implications, impact on retirement savings, and longevity risk. It's essential to understand the tax implications, plan your retirement income strategically, and consider seeking professional advice. Also, staying compliant with IRS guidelines, ERISA, and state laws is vital. Always remember your retirement decisions today will significantly impact your financial comfort in the future. Make those decisions wisely.403(b) Withdrawal Options Overview

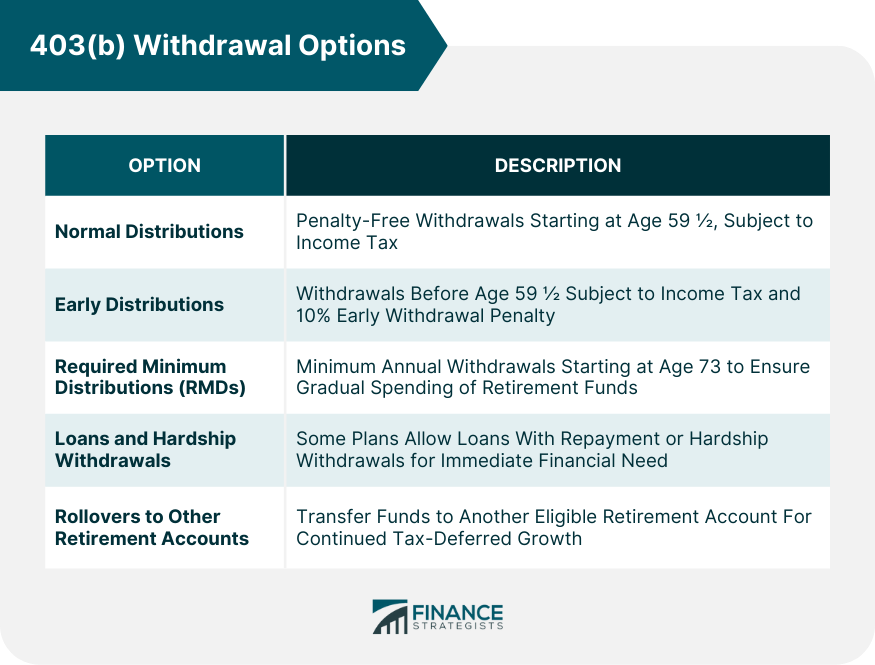

403(b) Withdrawal Options

Normal Distributions

Early Distributions

Required Minimum Distributions (RMDs)

Loans and Hardship Withdrawals

Rollovers to Other Retirement Accounts

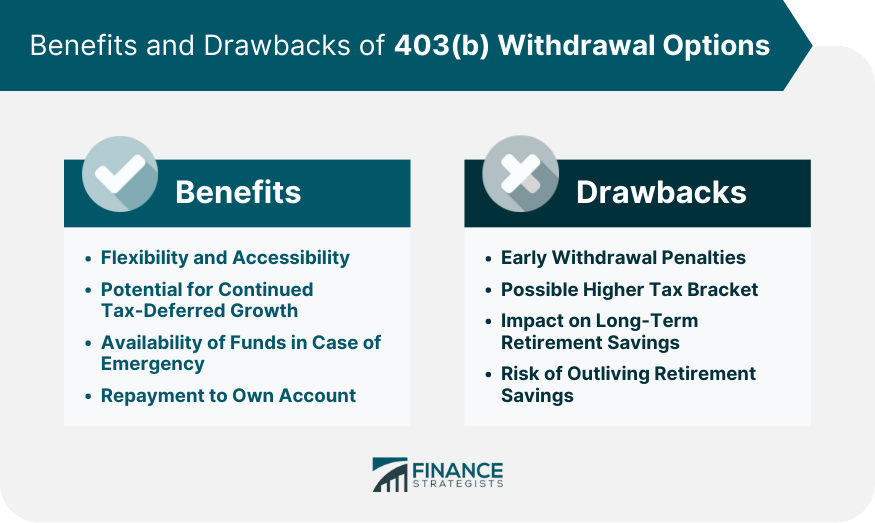

Benefits of Various 403(b) Withdrawal Options

Flexibility and Accessibility

Potential for Continued Tax-Deferred Growth

Availability of Funds in Case of Emergency

Repayment to Own Account

Drawbacks of 403(b) Withdrawal Options

Early Withdrawal Penalties

Possible Higher Tax Bracket

Impact on Long-term Retirement Savings

Risk of Outliving Retirement Savings

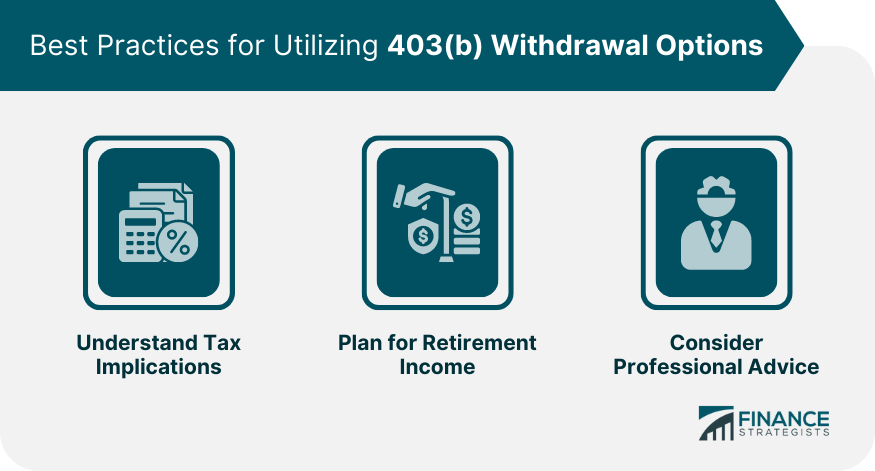

Best Practices for Utilizing 403(b) Withdrawal Options

Understanding Tax Implications

Planning for Retirement Income

Considering Professional Advice

Legal Implications and Considerations for 403(b) Withdrawal Options

IRS Guidelines

Employee Retirement Income Security Act (ERISA)

Compliance With State Laws

Considerations for Loans and Hardship Withdrawals

Taking Loans From 403(b) Account

Hardship Withdrawals From 403(b) Account

Conclusion

403(b) Withdrawal Options FAQs

The various 403(b) withdrawal options include normal distributions, early distributions, loans, hardship withdrawals, and rollovers to other retirement accounts. Each option has different tax implications and potential penalties.

Regular distributions from your 403(b) plan can begin without penalty once you reach the age of 59 ½. However, other withdrawal options like loans or hardship withdrawals might be available without penalties depending on your plan's terms and IRS guidelines.

403(b) withdrawal options can significantly impact your retirement savings. Early distributions, loans, and hardship withdrawals can reduce the overall value of your savings. Moreover, large withdrawals can push you into a higher tax bracket, increasing your tax liability.

The IRS guidelines, Employee Retirement Income Security Act (ERISA), and state laws all play a role in governing 403(b) withdrawal options. These regulations outline the qualifying circumstances for each withdrawal option, potential penalties, and tax implications and provide protections for retirement account holders.

Given the complexity of tax rules and retirement planning, it is beneficial to seek advice from a financial advisor when considering 403(b) withdrawal options. They can provide personalized guidance based on your unique circumstances and retirement goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.