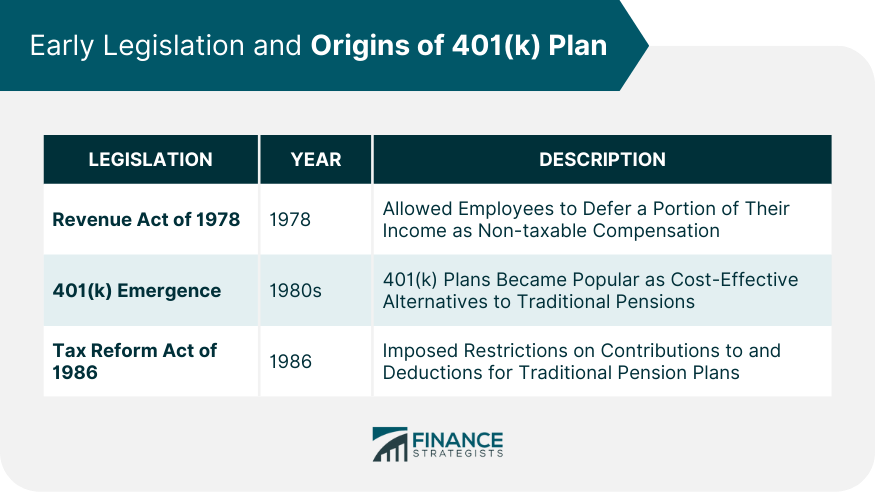

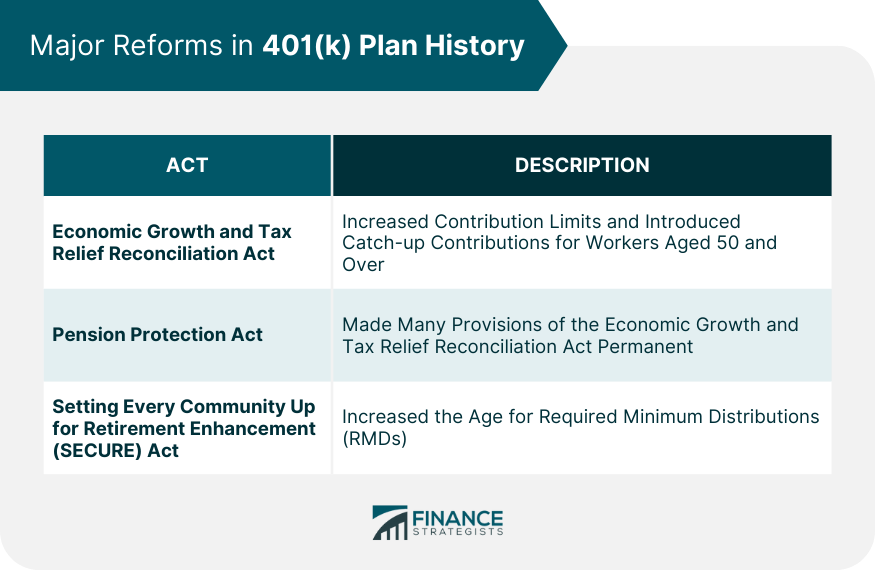

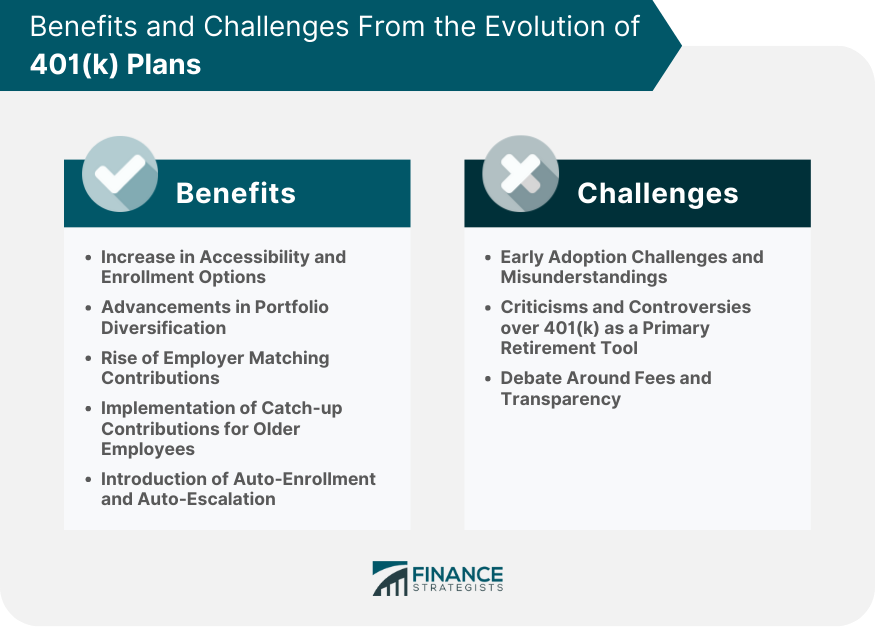

The 401(k) plan, a popular retirement savings vehicle, originated from the Revenue Act of 1978, which permitted employees to receive a portion of their income as deferred compensation. The plan gained traction in the 1980s as a cost-effective alternative to traditional pensions, especially following the Tax Reform Act of 1986. Over the years, further legislation refined the 401(k), including the Economic Growth and Tax Relief Reconciliation Act of 2001 and the Pension Protection Act of 2006, encouraging higher contribution limits, catch-up contributions, and automatic enrollment. Despite challenges like market volatility and fee transparency, the 401(k) plan remains integral to retirement planning, continuously evolving to cater to the changing retirement landscape. Understanding the history of the 401(k) plan is essential as it allows us to gain insights into the evolution of retirement savings. It also helps us understand the benefits and limitations of the 401(k) plan, shaping future regulations and improving personal financial planning. The birth of the 401(k) plan was a product of the Revenue Act of 1978. This act included a provision that allowed employees to avoid being taxed on a portion of income that they decided to receive as deferred compensation instead of direct cash payment. The 401(k) plans started gaining popularity in the 1980s as corporations saw them as a cost-effective alternative to traditional pensions. 401(k) plans shifted the financial risk from the employer to the employee, thereby gaining favor with corporations. The Tax Reform Act of 1986 further propelled 401(k) plans by placing restrictions on contributions to and deductions for traditional defined-benefit plans. This increased the attractiveness of 401(k) plans for many employers. This act significantly changed the 401(k) landscape by increasing contribution limits and offering catch-up contributions for workers aged 50 and over. It also encouraged automatic enrollment, further increasing the popularity of 401(k) plans. The Pension Protection Act of 2006 made many of the provisions in the Economic Growth and Tax Relief Reconciliation Act permanent. It also allowed employers to enroll employees automatically in 401(k) plans and to increase their contributions annually. The SECURE Act brought about significant changes, including increasing the age for required minimum distributions (RMDs) and allowing long-term, part-time workers to contribute to 401(k) plans. Financial crises, such as the 2008 economic downturn, greatly affected 401(k) investments. Many individuals saw their 401(k) balances dramatically decrease, leading to concerns about the reliance on these plans for retirement savings. Conversely, periods of economic growth led to a surge in 401(k) balances, reinforcing the popularity of these plans. Despite the volatility, the 401(k) plans remained an essential tool for retirement savings. As the 401(k) plan evolved, more and more employers began offering it, increasing accessibility for workers across various sectors. Auto-enrollment options also boosted participation rates. Over time, the options for investment within 401(k) plans have significantly expanded, allowing for better portfolio diversification. This includes a wider range of mutual funds, index funds, and, in some cases, individual stocks. Employer matching contributions have played a critical role in encouraging employee participation in 401(k) plans. This essentially provides free money to employees, making 401(k) plans an attractive vehicle for retirement savings. Older employees benefitted from the ability to make catch-up contributions, increasing their retirement savings potential. The catch-up contribution limit for those over 50 was a significant milestone in the history of 401(k) plans. Auto-enrollment and auto-escalation features were introduced to increase participation rates and savings levels in 401(k) plans. These features automatically enroll employees in the plan and gradually increase their contribution rates over time. The early years of the 401(k) plan saw low adoption rates due to a lack of understanding. Many employees didn't understand the potential benefits of the plan, leading to skepticism and hesitation. Over the years, there have been criticisms over the suitability of the 401(k) plan as a primary retirement savings vehicle. This stems from the potential for market volatility and the financial risk borne by the employee, unlike traditional pension plans. The fees associated with 401(k) plans and the lack of transparency around them have been a long-standing issue. High fees can significantly erode retirement savings over time, leading to calls for increased transparency and regulation. The evolution of 401(k) plans, initiated by the Revenue Act of 1978, has greatly shaped the retirement savings landscape. Key legislative reforms like the Tax Reform Act of 1986, the Economic Growth and Tax Relief Reconciliation Act of 2001, the Pension Protection Act of 2006, and the SECURE Act of 2019 have played pivotal roles in refining and popularizing 401(k) plans. These reforms have increased contribution limits, introduced catch-up contributions, encouraged automatic enrollment, and broadened eligibility. While 401(k) plans have faced challenges such as market volatility, fee transparency, and criticisms over their suitability as a primary retirement tool, their evolution has also brought significant benefits. These include increased accessibility, diverse investment options, employer matching contributions, and catch-up contributions. In the current landscape, technology is further transforming 401(k) plans, enhancing accessibility and ease of management, and sustaining their relevance in retirement planning.What Is the History of 401(k) Plans?

Early Legislation and Origins of 401(k) Plan

Revenue Act of 1978

Emergence and Popularity of 401(k) Plans in the 1980s

Tax Reform Act of 1986

Major Reforms in 401(k) Plan History

Economic Growth and Tax Relief Reconciliation Act of 2001

Pension Protection Act of 2006

Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019

Impact of Economic Events on the Evolution of 401(k) Plans

Impact of Financial Crises on 401(k) Investments

Effect of Economic Growth and Expansion Periods

Benefits From the Evolution of 401(k) Plans

Increase in Accessibility and Enrollment Options

Advancements in Portfolio Diversification

Rise of Employer Matching Contributions

Implementation of Catch-up Contributions for Older Employees

Introduction of Auto-Enrollment and Auto-Escalation

Challenges Encountered in the History of 401(k) Plans

Early Adoption Challenges and Misunderstandings

Criticisms and Controversies Over 401(k) as a Primary Retirement Tool

Debate Around Fees and Transparency

Conclusion

History of 401(k) Plans FAQs

The 401(k) plans first became a part of the retirement landscape following the Revenue Act of 1978. This act allowed employees to receive a portion of their compensation as deferred compensation, which would not be taxed until distributed.

The 401(k) plan started gaining popularity in the 1980s as it was seen as a cost-effective alternative to traditional pensions. The Tax Reform Act of 1986 further increased their attractiveness for many employers by placing restrictions on contributions to and deductions for traditional defined-benefit plans.

The Pension Protection Act of 2006 was a significant event in the history of 401(k) plans as it made many of the provisions in the Economic Growth and Tax Relief Reconciliation Act of 2001 permanent. Additionally, it encouraged automatic enrollment, thereby increasing participation in 401(k) plans.

The primary challenges encountered in the history of 401(k) plans include early adoption challenges due to misunderstandings about the plan, criticisms over the suitability of 401(k) as a primary retirement tool due to potential market volatility, and the debate around high fees and lack of transparency.

Technological advances have had a significant impact on the current landscape of 401(k) plans. They have made information more accessible and understandable, with online platforms and mobile apps allowing for easier tracking and management of 401(k) investments. This has encouraged more active participation in these plans.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.