A 401(k) loan default occurs when a borrower fails to repay a loan taken from their 401(k) retirement plan within the specified time frame. This usually happens if the borrower leaves or loses their job while the loan is outstanding. In case of a default, the IRS treats the unpaid balance as a premature distribution, subject to income tax and potentially a 10% early withdrawal penalty if the borrower is under 59.5 years of age. This not only erodes the borrower's retirement savings but also results in a hefty tax bill. Furthermore, defaulted 401(k) loans can affect one's credit score and future borrowing ability. Financial advisors often recommend considering a 401(k) loan as a last resort after exhausting other loan options. Despite these risks, 401(k) loans can provide a convenient, low-interest source of funds when managed responsibly. The moment you default on a 401(k) loan, the IRS considers the unpaid balance as a distribution. This means you are likely to owe income tax on the defaulted amount, and if you are under the age of 59.5, you may also be hit with an additional 10% early withdrawal penalty. Your 401(k) plan administrator may also charge penalties and fees in the event of a default. These could include late payment fees or administrative charges, further increasing the cost of default. Perhaps the most critical impact of a 401(k) loan default is its potential to deplete your retirement savings. When you take out a loan from your 401(k), the borrowed money is no longer invested in the market, meaning you may miss out on potential growth. If you default, the unpaid balance permanently leaves your retirement account, further reducing your future retirement income. The stress of a loan default should not be underestimated. The financial burden can lead to anxiety, depression, and strained relationships, creating a cycle that can be difficult to break. To avoid a 401(k) loan default, careful repayment planning is essential. Before taking a loan, calculate the payments into your budget to ensure you can comfortably meet the obligation. You should also consider the loan's term length and the potential impact of interest rates on your repayments. Most 401(k) plans allow borrowers to set up automatic deductions from their paychecks for loan repayments. This feature can help ensure timely payments and eliminate the risk of forgetting to make a payment. Life is unpredictable, and financial setbacks can occur. Therefore, having a contingency plan can help protect against potential defaults. This might involve setting aside an emergency fund or identifying other sources of income that can be tapped during difficult times. Keeping the lines of communication open with your 401(k) plan administrator can be critical in avoiding a default. If you're having trouble making payments, they may be able to provide options or solutions you weren't aware of. Even with careful planning, you may find yourself facing an imminent 401(k) loan default. Here are some steps you can take to mitigate the impact. Some plans offer a grace period after a missed payment or even a cure period after leaving a job, during which you can repay the loan without it being considered a default. Check with your plan administrator for these options. If you're having trouble keeping up with payments, consider speaking with your plan administrator about restructuring your loan to lower the payments or extend the repayment period. Sometimes, the best course of action is to seek help from a professional. Financial advisors or credit counselors can provide advice tailored to your unique situation and help you navigate your way out of potential default. Even if a default does occur, it's not the end of the world. Here are some strategies to recover and rebuild your financial health. Remember, the IRS will likely treat your defaulted loan as a distribution, which means you'll owe income tax on the unpaid balance and potentially an early withdrawal penalty if you're under 59.5 years old. It's essential to prepare for these costs to avoid a surprise tax bill. Following a 401(k) loan default, it's crucial to focus on rebuilding your retirement savings. This might involve increasing your 401(k) contributions or exploring other savings vehicles like IRAs or HSAs. Learn from your default. Identify what led to the default and what you could have done differently. Use these lessons to prevent future defaults and make more informed financial decisions. Provide quick access to funds without risking retirement savings or incurring penalties. Plus, they are not subject to credit checks or rigorous approval processes. The main downside is that the interest earned on savings accounts is generally quite low, particularly in comparison to the potential returns from investments in a 401(k). Offer a large sum of money but put your home at risk if you can't make repayments. Interest rates are generally lower than those of personal loans, and the interest may be tax-deductible. However, if you fail to make the payments, the lender could foreclose on your home, making this a risky choice if you're unsure about your future income stability. Typically have higher interest rates than 401(k) loans but don't risk your retirement savings. They're unsecured, meaning they don't require collateral like your home or car. However, the amount you can borrow and your interest rate will heavily depend on your credit score, and unlike 401(k) loans or home equity loans, the interest is not tax-deductible. 401(k) loan defaults carry considerable implications, from immediate tax burdens and potential penalties to long-term effects on retirement savings and psychological stress. However, careful planning and communication with the plan administrator can help avoid defaulting. When faced with an imminent default, options like grace periods, loan restructuring, and professional advice might mitigate the impact. Post-default strategies focus on managing tax implications and rebuilding retirement savings, leveraging lessons learned for future decision-making. Exploring alternatives like savings accounts, home equity loans, or personal loans could also be a safer route, given the significant risks associated with 401(k) loans. The complexities of these financial decisions highlight the importance of seeking professional guidance. Don't hesitate to consult a financial advisor who can provide personalized advice based on your unique circumstances, helping you make informed decisions for a secure financial future.Overview of 401(k) Loan Defaults

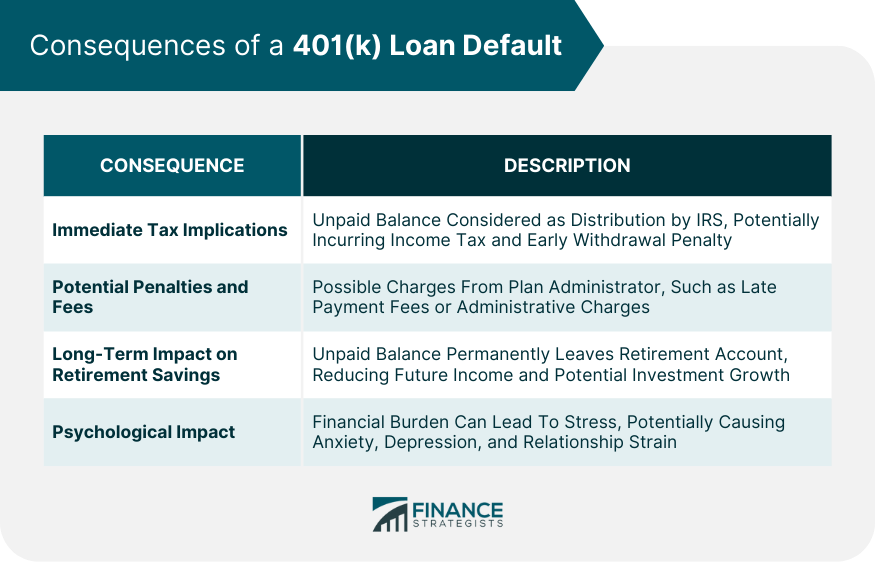

Consequences of a 401(k) Loan Default

Immediate Tax Implications

Potential Penalties and Fees

Long-Term Impact on Retirement Savings

Psychological Impact

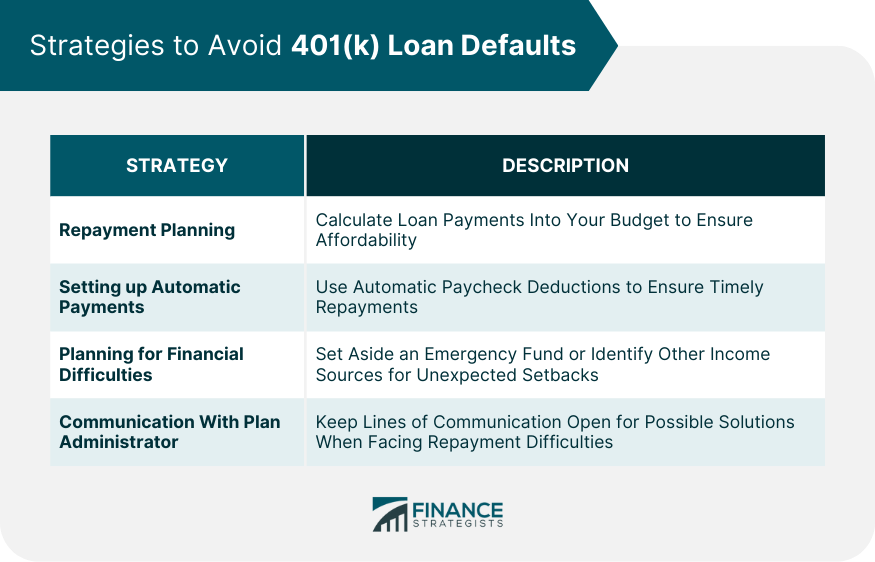

How to Avoid 401(k) Loan Defaults

Repayment Planning

Setting up Automatic Payments

Planning for Financial Difficulties

Communicating With Plan Administrator

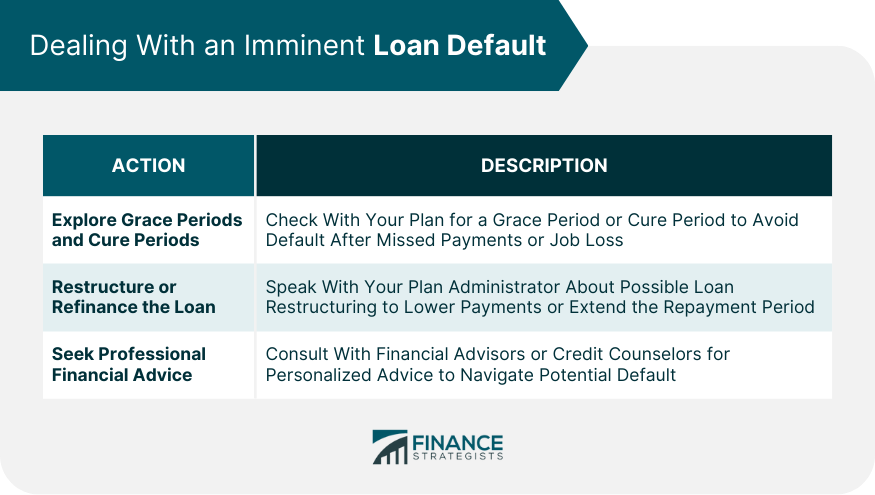

Dealing With an Imminent Loan Default

Explore Grace Periods and Cure Periods

Restructure or Refinance the Loan

Seek Professional Financial Advice

After a 401(k) Loan Default

Handle the Tax Implications

Rebuild Your Retirement Savings

Lessons Learned and Prevention of Future Defaults

Alternatives to a 401(k) Loan

Savings Accounts

Home Equity Loans

Personal Loans

The Bottom Line

401(k) Loan Defaults FAQs

A 401(k) loan default occurs when a borrower fails to meet the repayment terms of their 401(k) loan, leading to significant tax implications and potential penalties.

Defaulting on a 401(k) loan can result in immediate tax implications, potential penalties and fees, a long-term impact on retirement savings, and psychological stress.

To avoid a default, plan your repayment strategy carefully, set up automatic payments, prepare for unexpected financial difficulties, and maintain open communication with your plan administrator.

If a default seems imminent, explore grace or cure periods, consider restructuring or refinancing the loan, and seek professional financial advice.

Yes, alternatives to a 401(k) loan include other sources of emergency funds like savings accounts, home equity loans, or personal loans, each with their own pros and cons.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.