Gross Net Written Premium Income is a critical financial metric in the insurance industry. It represents the total premiums an insurance company writes over a specific period, typically a year, minus the premiums it cedes to reinsurance. In essence, it denotes the insurer's total potential revenue from underwriting activities after accounting for reinsurance costs. The purpose of this metric is to assess the insurer's underwriting activity, which directly contributes to its profitability. GNWPI is of paramount importance as it indicates an insurer's capacity to underwrite risk and its financial health. Regulators, investors, and policyholders closely monitor it to gauge the insurer's ability to meet its claim liabilities and its financial strength. In essence, GNWPI Income serves as a key performance indicator in the insurance sector. To calculate the Net Written Premium, the cost of reinsurance is subtracted from the Gross Written Premium. In the calculation of Net Written Premium, Ceded Premiums (premiums passed to reinsurers) are subtracted, and Assumed Premiums (premiums accepted from another insurer or reinsurer) are added. This process allows the insurance company to spread its risks and maintain its financial stability. The GNWPI forms the base from which an insurance company pays its expenses, claims, and profits. A higher GNWPI generally signifies better profitability, assuming the insurer has properly priced its policies and managed its risks. Regulators and investors closely monitor GNWPI as it plays a significant role in solvency analysis. A decrease in Net Written Premium may indicate an increased reliance on reinsurance and potentially higher risks. GNWPI also impacts the level of reserves an insurance company must maintain to cover potential claims. It affects the policyholder surplus, which is the difference between an insurer's assets and liabilities. A healthier surplus indicates a more financially secure insurer. GNWPI is essential in insurance underwriting. It can influence underwriting profitability, the underwriting cycle, and reinsurance decisions. An insurer's underwriting profitability is determined by comparing its GNWPI to its incurred losses and underwriting expenses. If the GNWPI exceeds these costs, the insurer has an underwriting profit. GNWPI also influences the underwriting cycle, which is the cyclical pattern of insurance pricing, sales, and profitability. Changes in GNWPI can reflect shifts in the underwriting cycle, influencing strategic decisions. The balance between Gross Written Premium and Net Written Premium can influence an insurer's reinsurance decisions. For example, if an insurer has a high Gross Written Premium but a low Net Written Premium, it may indicate a heavy reliance on reinsurance, prompting a review of the company's reinsurance strategy. GNWPI has several regulatory implications, influencing regulations, impacting the Solvency II Directive, and playing a role in Risk-Based Capital (RBC) calculations. Regulators monitor GNWPI to ensure that insurance companies are adequately capitalized and able to meet their claims liabilities. It's a critical component in assessing an insurer's financial strength and stability. In the European Union, the Solvency II Directive uses GNWPI as one of the factors in calculating an insurer's Solvency Capital Requirement, which is the number of funds an insurer must hold to reduce the risk of insolvency. In the United States, the National Association of Insurance Commissioners (NAIC) uses GNWPI in its Risk-Based Capital (RBC) calculations. These calculations determine the minimum amount of capital an insurer must hold to support its overall business operations considering its size and risk profile. Tools commonly used in analyzing GNWPI include ratio analysis and trend analysis. The former involves comparing GNWPI to other financial metrics, while the latter involves observing changes in GNWPI over time. The interpretation of these analyses can provide insights into the insurer's financial health, profitability, and risk profile. For example, a steady increase in GNWPI may suggest growth in the insurer's business, while a decline may indicate potential financial difficulties or increased competition. However, there are challenges in the analysis. Changes in GNWPI can be due to various factors, such as changes in underwriting practices, reinsurance strategy, or market conditions. Thus, it's important to understand the context in which changes occur. Technological advancements is likely to have a significant impact on GNWPI. For example, InsurTech innovations can improve risk assessment and pricing accuracy, potentially increasing GNWPI. Regulatory changes can also affect GNWPI. For example, changes to capital requirements or the treatment of reinsurance could impact the balance between Gross and Net Written Premiums. Despite these challenges, insurers, analysts, and investors continuously strive to forecast future trends in GNWPI using various models and scenarios. These forecasts can inform strategic decisions, investment choices, and regulatory responses. Gross Net Written Premium Income (GNWPI) stands as a fundamental financial indicator, representing the balance between total premiums written and the premiums ceded to reinsurance over a certain period. This metric not only determines an insurer's revenue from underwriting activities but also shapes its profitability, solvency, and financial strength. Critical to underwriting processes, it influences profitability, the underwriting cycle, and reinsurance strategies. Moreover, GNWPI has far-reaching regulatory implications, feeding into solvency assessments and risk-based capital calculations. Analyzing this measure is crucial, despite potential challenges, as it offers vital insights into the insurer's financial health. Looking ahead, technological advancements and regulatory changes are set to significantly shape the future trajectory of GNWPI. All in all, this measure remains an invaluable tool for insurers, investors, and regulators alike.What Is Gross Net Written Premium Income (GNWPI)?

Calculation of GNWPI

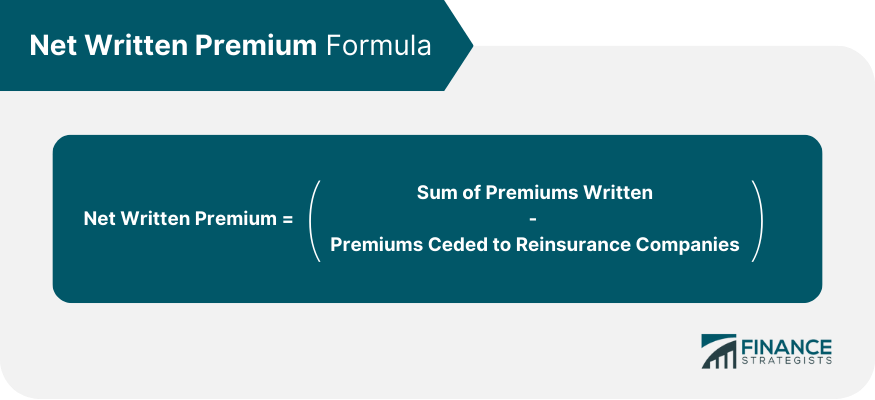

Formula for Calculating Net Written Premium

Role of Ceded and Assumed Premiums

Role of GNWPI in Insurance Accounting

Contribution to Insurance Profitability

Implication in Solvency Analysis

Impact on Reserves and Policyholder Surplus

Importance of GNWPI in Underwriting

Use in Determining Underwriting Profitability

Influence on the Underwriting Cycle

Effect on Reinsurance Decisions

Regulatory Implications of GNWPI

Regulation of GNWPI

Impact on Solvency II Directive

Role in Risk-Based Capital (RBC) Calculations

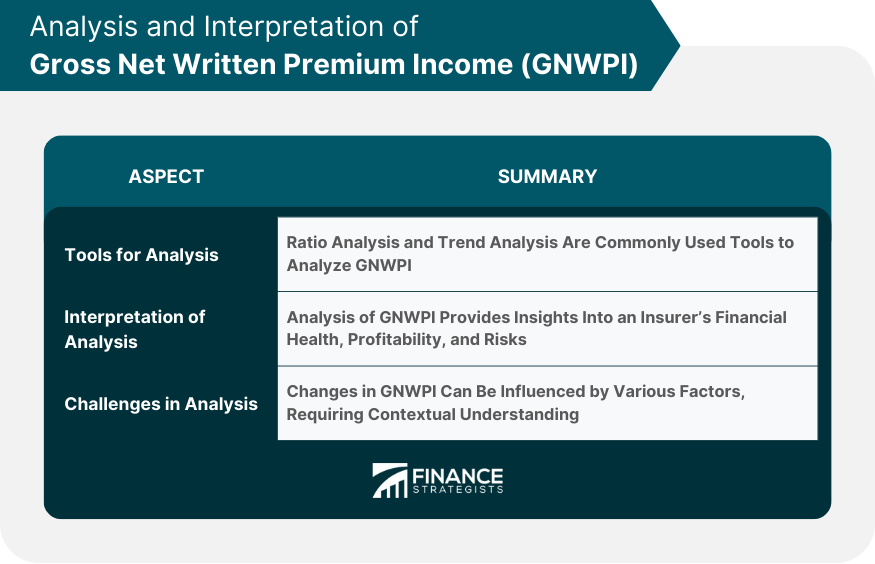

Analysis and Interpretation of GNWPI

Tools for Analysis - Ratio Analysis, Trend Analysis

Interpretation of Analysis

Challenges in Analysis

Future Trends and Predictions Related to GNWPI

Impact of Technological Advancements

Influence of Regulatory Changes

Forecasting Future Trends

Final Thoughts

Gross Net Written Premium Income FAQs

Gross Net Written Premium Income (GNWPI) is the total premiums an insurance company writes during a specific period, less the premiums it cedes to reinsurance. It represents the insurer's base revenue from underwriting activities.

Gross Net Written Premium Income (GNWPI) is a key performance indicator for insurance companies as it directly impacts their profitability. It helps determine the insurer's ability to meet its claims liabilities and provides insights into the insurer's risk profile and financial strength.

Gross Net Written Premium Income (GNWPI) is calculated by subtracting the cost of reinsurance from the total premiums received from all policies written during a specific period. The formula is Net Written Premium = Gross Written Premium - Cost of Reinsurance.

Gross Net Written Premium Income (GNWPI) influences underwriting profitability, the underwriting cycle, and reinsurance decisions. It's an indicator of an insurer's underwriting risk, guiding its strategic decisions related to risk acceptance, policy pricing, and reinsurance.

Gross Net Written Premium Income (GNWPI) plays a critical role in regulatory compliance. Regulators monitor this metric to ensure insurance companies are adequately capitalized and can meet their claims liabilities. It's also used in the calculation of Solvency Capital Requirements in the EU and Risk-Based Capital (RBC) in the US.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.