An annuity is a financial product that provides a stream of income to an individual in exchange for a lump sum payment or a series of payments made over time. When an individual decides to purchase an annuity, they often do not think about how they will exit the investment when the time comes. There are several scenarios where an individual may want to exit their annuity. It is also important to know how to get out of an annuity when the need arises. There are some common ways to exit an annuity including: An annuity surrender occurs when the owner of the annuity terminates the contract before the end of the contract term. This option is available for fixed, indexed, and variable annuities. However, surrendering an annuity may come with surrender charges and fees. These charges are designed to discourage the annuity owner from surrendering the annuity and can be substantial. The amount of the surrender charge is usually a percentage of the account value, and it decreases over time. The main advantage of surrendering an annuity is that it provides the annuity owner with quick access to their funds. The annuity owner can use the funds to pay off debt, cover emergency expenses, or invest in other financial products that better align with their goals. However, surrendering an annuity may not be the best option for individuals who have had the annuity for a long time because the surrender charge decreases over time. It may also be disadvantageous for individuals who are looking for a steady stream of income during retirement. Another way to exit an annuity is through an annuity exchange. An annuity exchange allows the annuity owner to transfer the cash value of their current annuity to a new annuity without incurring taxes or penalties. Annuity exchanges are available for indexed, fixed and variable annuities, and there are various types of annuity exchanges available. The most common type of annuity exchange is the 1035 exchange. This allows the annuity owner to transfer the cash value of their current annuity to a new annuity without triggering taxes or penalties. The main advantage of an annuity exchange is that it allows the annuity owner to maintain the tax-deferred status of their annuity while also giving them the ability to switch to an annuity that better aligns with their financial goals. Additionally, an annuity exchange may not have any surrender charges or fees, making it a cost-effective way to exit an annuity. However, annuity exchanges may come with new surrender charges or fees, and the new annuity may have a new contract term that resets the surrender charge schedule. Selling an annuity is another option for individuals who want to exit an annuity. An annuity sale occurs when the annuity owner sells their annuity to a third-party buyer for a lump sum of cash. The buyer then assumes ownership of the annuity and receives the future payments. The secondary annuity market is the market where annuities are bought and sold, and it allows the annuity owner to exit the annuity before the contract term ends. The main advantage of selling an annuity is that it provides the annuity owner with a lump sum of cash. The owner can use the cash to pay off debt, invest in other financial products, or cover emergency expenses. Additionally, the annuity owner can use the funds from the sale to purchase a new annuity that better aligns with their financial goals. Selling an annuity may come with a significant discount. The buyer of the annuity will only pay a lump sum of cash that is less than the present value of the future payments. Additionally, selling an annuity may have tax implications, and the annuity owner may have to pay taxes on the gains from the sale. Knowing when to get out of an annuity is a crucial decision for annuity owners, and it is a decision that should be made with careful consideration. If an annuity is underperforming or not meeting the owner's expectations, it may be time to consider exiting the investment. This scenario is especially true for variable annuities, where the performance is tied to the performance of the underlying investments. When the owner is experiencing financial hardship, they may want to exit their annuity to access the cash value of the investment. This scenario is common during an economic downturn, where individuals may need cash to cover emergency expenses or pay off debt. As an individual's financial goals change, their annuity may no longer align with their objectives. For example, if an individual initially purchased an annuity to generate income during retirement, but their retirement plans have changed, they may want to exit the investment. Annuities can come with high fees and charges, which can eat into an individual's returns. If an annuity owner is unhappy with the fees associated with their annuity, they may want to consider exiting the investment. If an individual inherits an annuity, they may want to exit the investment to access the cash value or invest the funds in a product that better aligns with their financial goals. Exiting an annuity may come with tax implications. Surrendering an annuity before the age of 59 ½ can result in a 10% early withdrawal penalty on top of the income tax due on the gains. Additionally, selling an annuity may trigger taxes on the gains from the sale. The amount of taxes due will depend on the owner's tax bracket and the length of time they have held the annuity. In some cases, annuity exchanges may also come with tax implications if the new annuity has different terms than the old annuity. To avoid or minimize the tax implications of exiting an annuity, individuals should take advantage of tax services. They can help the individual understand their tax liability and determine the best way to exit the annuity. Exiting an annuity may not be the best option for everyone. There are alternative strategies that individuals can use to meet their financial goals without exiting the annuity. One alternative is to take partial withdrawals from the annuity. This strategy allows the annuity owner to withdraw a portion of their account value while leaving the rest of the account intact. Another alternative is to use the annuity as collateral for a loan. This strategy allows the annuity owner to access the cash value of their annuity without surrendering the annuity. An annuity is a financial product that provides a stream of income to an individual in exchange for a lump sum payment or a series of payments made over time. Getting out of an annuity can be a challenging decision for annuity owners. However, there are various options available for exiting an annuity, including surrendering, exchanging, and selling the annuity. Knowing when to get out of an annuity is also crucial. There are several scenarios where an individual may want to exit their annuity, such as dissatisfaction with performance, financial hardship, changing financial goals, high fees, and inheritance. However, it is essential to consider the consequences of exiting an annuity, such as surrender charges, taxes, and the loss of future income. Additionally, there are potential alternatives to exiting an annuity, such as taking partial withdrawals or using the annuity as collateral for a loan. These alternatives can allow annuity owners to meet their financial goals without surrendering, exchanging, or selling their annuity. Each option comes with its own set of advantages and disadvantages, and individuals should consult with a financial advisor before making any decisions regarding their annuity.Overview of an Annuity

Ways to Get Out of an Annuity

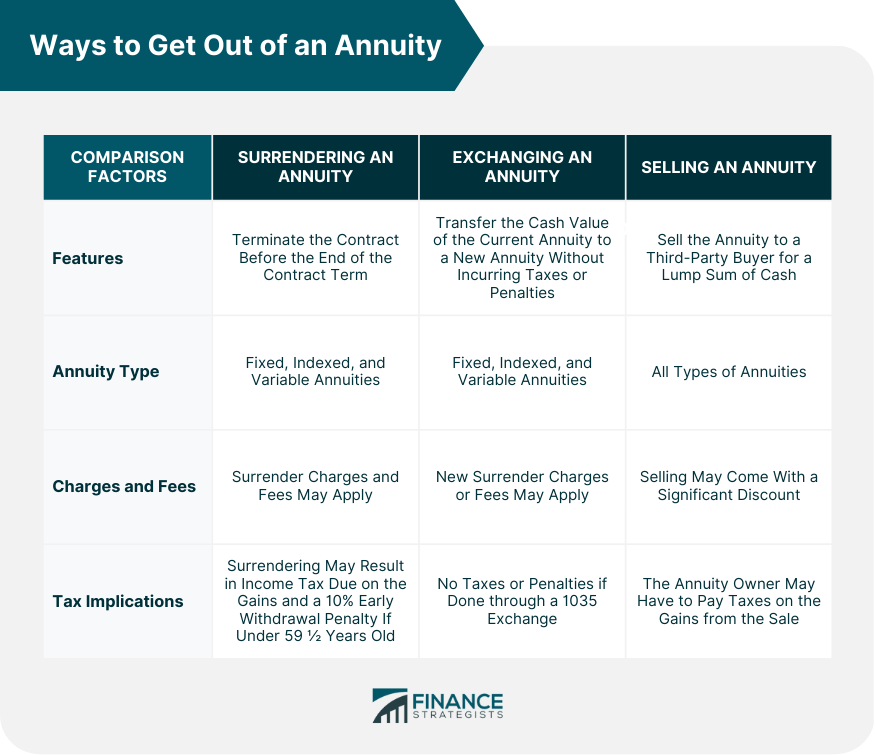

Surrendering an Annuity

Exchanging an Annuity

Selling an Annuity

When to Get Out of an Annuity

Dissatisfaction With Performance

Financial Hardship

Changing Financial Goals

High Fees

Inheritance

Tax Implications of Exiting an Annuity

Alternatives to Getting Out of an Annuity

Final Thoughts

How to Get Out of an Annuity FAQs

There are several ways to get out of an annuity, including surrendering the annuity, exchanging it, or selling it.

You may want to get out of an annuity if you're dissatisfied with its performance, experiencing financial hardship, or if your financial goals have changed.

Exiting an annuity may result in income tax due on the gains and a 10% early withdrawal penalty if you're under 59 ½ years old. Consult a tax professional for guidance.

You can consider taking partial withdrawals or using the annuity as collateral for a loan as potential alternatives to exiting an annuity.

Yes, it's crucial to consult with a financial advisor or tax professional before making any decisions regarding an annuity to ensure that the chosen option aligns with your overall financial plan.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.