Annuity beneficiary designations are decisions made by the annuitant (the owner of the annuity) to specify who will receive the annuity proceeds upon their death. These designations help ensure a smooth and efficient transfer of annuity benefits to the intended recipients, avoiding probate and potential disputes. The annuitant can name individuals, entities, or trusts as beneficiaries, and there are different types of beneficiaries, such as primary, contingent, revocable, and irrevocable. Properly designating annuity beneficiaries is critical to financial planning and estate management. The primary purpose of naming a beneficiary is to ensure a smooth and efficient transfer of annuity proceeds upon the annuitant's death. Designating a beneficiary helps avoid probate and ensures the annuity benefits reach the intended recipient without unnecessary delays or legal complications. The tax treatment of annuity proceeds varies depending on the type of annuity, the beneficiary's relationship to the annuitant, and the distribution method chosen. Beneficiaries may be subject to income taxes on the annuity proceeds they receive, so it is important to consider tax implications when designating beneficiaries. When an annuitant dies, the beneficiary is responsible for notifying the annuity company and providing necessary documentation, such as a death certificate. Depending on the annuity contract terms and applicable tax laws, the beneficiary must also choose a distribution method, which may include lump-sum payments or continued annuity payments. Primary beneficiaries are the first in line to receive annuity proceeds upon the annuitant's death. An annuitant can name one or multiple primary beneficiaries and can also allocate specific percentages of the annuity proceeds to each. Contingent beneficiaries receive annuity proceeds if the primary beneficiary is unable or unwilling to accept the benefits. Naming contingent beneficiaries helps ensure the annuity proceeds are distributed according to the annuitant's wishes if the primary beneficiaries predecease the annuitant or cannot receive the benefits. The annuitant can change revocable beneficiaries at any time without the beneficiary's consent. In contrast, irrevocable beneficiaries cannot be removed or replaced without the beneficiary's consent, offering them greater protection and control over the annuity proceeds. An annuitant can name a trust as a beneficiary, which can provide additional control and flexibility in distributing annuity proceeds. Trusts are legal entities that can hold and manage assets for the benefit of one or more beneficiaries according to the trust's terms. The annuitant's relationship with the beneficiary is an important factor to consider. Typical beneficiaries include spouses, children, relatives, friends, or charitable organizations. The annuitant should consider the beneficiary's financial needs and ability to manage the annuity proceeds responsibly. When designating beneficiaries, the annuitant should consider the beneficiary's age and life expectancy. Younger beneficiaries may have a longer life expectancy, increasing the likelihood of receiving the annuity benefits. The annuitant should consider the financial needs and goals of the beneficiaries when designating them. For example, suppose a beneficiary has significant financial obligations, such as student loans or a mortgage. In that case, the annuitant may choose to allocate a larger portion of the annuity proceeds to that beneficiary. The annuitant should consider the potential tax implications for the chosen beneficiaries. The tax treatment of annuity proceeds may differ depending on the beneficiary's relationship to the annuitant and the chosen distribution method. Consulting with a tax services professional can help understand and plan for potential tax liabilities. To designate beneficiaries, the annuitant must complete a beneficiary designation form provided by the annuity company. This form typically requires the annuitant to provide the beneficiary's full name, Social Security number, date of birth, and contact information. The annuitant must also specify the type of beneficiary (primary or contingent) and the allocation percentage, if applicable. Annuitants must review and update their beneficiary designations regularly, especially after significant life events such as marriage, divorce, childbirth, or beneficiary death. Keeping beneficiary designations up-to-date ensures that the annuity proceeds are distributed according to the annuitant's current wishes. Regularly reviewing and updating beneficiary information helps avoid potential disputes and ensures that the annuity proceeds are distributed efficiently upon the annuitant's death. Annuitants should also inform their beneficiaries of their designation so they are aware of their responsibilities and the annuity's terms and conditions. One common mistake is failing to name a beneficiary for the annuity. In this case, the annuity proceeds may be subject to probate, which can be a lengthy and expensive process. Additionally, the proceeds may be distributed according to state intestacy laws, which may not align with the annuitant's wishes. Another common mistake is to update beneficiary information after significant life events, such as marriage or divorce. This oversight can result in unintended consequences, such as the annuity proceeds being distributed to an ex-spouse or not being distributed to a new spouse or child. Annuitants should be cautious when designating beneficiaries to avoid unintentionally disinheriting loved ones. For example, if an annuitant names their children as primary beneficiaries but later remarries and wants to include their new spouse, they must update the beneficiary designation to reflect this change. Failing to consider the tax implications for beneficiaries can result in an unexpected tax burden for the beneficiary. Annuitants should consult with a tax professional to ensure they understand the potential tax consequences for their chosen beneficiaries. In some states, spouses have certain rights regarding annuity beneficiary designations. For example, a spouse may be entitled to a portion of the annuity proceeds even if they are not named as a beneficiary. Annuitants should know their state's spousal rights and consider these when designating beneficiaries. Annuity beneficiary designations may offer some protection from creditors. In most cases, annuity proceeds payable to a named beneficiary are not considered part of the annuitant's estate and are therefore protected from the annuitant's creditors. Inheritance disputes can arise when the annuity beneficiary designations need to be clarified or updated. To prevent such disputes, annuitants should ensure their beneficiary designations are clear, current, and in line with their wishes. Designating annuity beneficiaries is a crucial aspect of financial planning that ensures the efficient transfer of annuity proceeds upon the annuitant's death. By understanding the importance of annuity beneficiary designations, the different types of beneficiaries, and factors to consider when choosing beneficiaries, annuitants can make informed decisions that align with their financial goals and protect their loved ones' financial futures. Regularly reviewing and updating beneficiary information, especially after significant life events, is essential to avoid potential disputes and ensure that the annuity proceeds are distributed according to the annuitant's wishes. Additionally, considering the tax implications for beneficiaries and understanding the rights and protections offered by annuity beneficiary designations can help annuitants make the best decisions for themselves and their beneficiaries. By making informed annuity beneficiary designations, annuitants can provide financial security for their loved ones and help them navigate the challenges that may arise upon the annuitant's death, ensuring that their legacy is preserved and their wishes are fulfilled. To ensure that you make the most informed decisions about your annuity beneficiary designations, consider hiring an insurance broker with expertise in annuities. A professional insurance broker can help you navigate the complex world of annuities, provide personalized guidance, and ensure that your financial goals and your loved ones' futures are well-protected. What Are Annuity Beneficiary Designations?

The Role of Beneficiaries in Annuities

Purpose of Naming a Beneficiary

Tax Implications for Beneficiaries

Responsibilities of Beneficiaries upon the Annuitant's Death

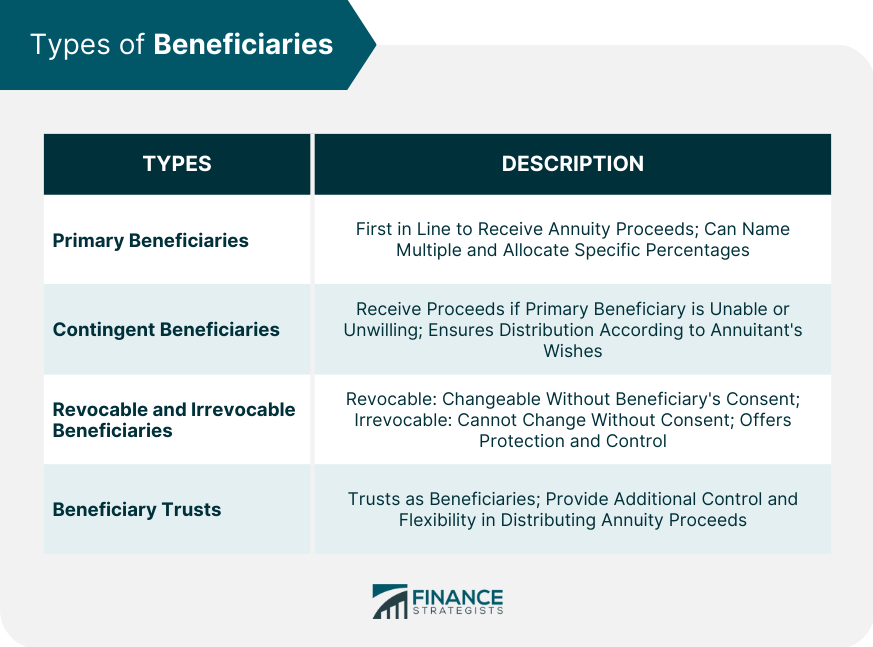

Types of Beneficiaries

Primary Beneficiaries

Contingent Beneficiaries

Revocable and Irrevocable Beneficiaries

Beneficiary Trusts

Factors to Consider When Choosing Beneficiaries

Relationship to the Annuitant

Age and Life Expectancy of Beneficiaries

Financial Needs and Goals of Beneficiaries

Tax Implications for Chosen Beneficiaries

The Process of Designating Beneficiaries

Completing the Beneficiary Designation Form

Updating Beneficiary Designations

Regularly Reviewing and Updating Beneficiary Information

Common Annuity Beneficiary Designation Mistakes

Failing to Name a Beneficiary

Not Updating Beneficiary Information After Life Events

Unintentionally Disinheriting Loved Ones

Not Considering Tax Implications for Beneficiaries

Annuity Beneficiary Rights and Protections

Spousal Rights in Annuity Beneficiary Designations

Protection From Creditors

Inheritance Rights and Disputes

Conclusion

Annuity Beneficiary Designations FAQs

Annuity beneficiary designations are the decisions made by an annuitant (the owner of the annuity) to name one or more individuals, entities, or trusts to receive the annuity proceeds upon their death. These designations are crucial because they ensure a smooth and efficient transfer of annuity benefits to the intended recipients, avoiding probate and potential disputes.

To choose the right annuity beneficiary designations, consider factors such as your relationship with potential beneficiaries, their age, life expectancy, financial needs, and goals. Also, consider the tax implications for the beneficiaries and consult a financial advisor or tax professional for guidance.

Yes, you can typically change your annuity beneficiary designations after the initial setup as long as the named beneficiaries are revocable. To make changes, contact your annuity company and complete a new beneficiary designation form. Reviewing and updating your designations regularly is essential, especially after significant life events.

There are several types of annuity beneficiary designations, including primary beneficiaries (first in line to receive benefits), contingent beneficiaries (receive benefits if primary beneficiaries cannot), and revocable or irrevocable beneficiaries (revocable beneficiaries can be changed without consent, while irrevocable beneficiaries cannot). Additionally, annuitants can designate trusts as beneficiaries for added control and flexibility.

Common mistakes to avoid when making annuity beneficiary designations include failing to name a beneficiary, not updating beneficiary information after significant life events, unintentionally disinheriting loved ones, and not considering the tax implications for your chosen beneficiaries. Regularly reviewing and updating your designations can help avoid these mistakes and ensure the efficient transfer of annuity proceeds.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.