An offshore bank account is a bank account that a person or company opens in a country outside their own. This practice, known as offshore banking, is not necessarily illegal or suspicious, as it is often portrayed in movies and popular culture. Many law-abiding citizens and businesses make use of offshore banking for legitimate reasons. The primary purpose of opening an offshore bank account is to take advantage of certain financial and legal benefits that may not be available in one's home country. These benefits can include stronger privacy protections, access to better banking or investment options, and potential tax benefits. The importance of offshore banking can vary greatly depending on an individual's or a business's financial situation and goals. For instance, a multi-national company might need offshore banking for easy international transactions, while an individual might find tax savings or asset protection to be a key benefit. Setting up an offshore bank account often involves more steps compared to opening a domestic account. It typically starts with researching and selecting an appropriate offshore jurisdiction. This would involve communicating with banks in the chosen jurisdiction, providing the required documentation, and adhering to the due diligence procedures set by the bank. The exact steps and prerequisites can differ substantially depending on the jurisdiction and the specific bank. Offshore banks offer many of the same services as domestic banks. This includes the following services: 1. Regular Checking and Savings Accounts: These accounts function similarly to domestic accounts, allowing individuals to deposit, withdraw, and manage their funds. 2. Credit and Debit Cards: Enable account holders to make purchases and access funds worldwide. These cards may come with additional benefits such as travel insurance, reward programs, and enhanced security features. 3. Investment Services: Provide a range of investment options to suit the diverse needs of their clients. These can include investment accounts, brokerage services, and access to global financial markets. Clients may have the opportunity to invest in stocks, bonds, mutual funds, and other investment instruments. 4. Multi-Currency Accounts: Offshore banks allow clients to manage funds in various currencies, facilitating international transactions and mitigating foreign exchange risks. 5. International Wire Transfer Services: These services enable clients to send and receive funds internationally, whether for personal or business purposes. 6. Wealth Management Services: These services include portfolio management, tax planning, estate planning, and asset protection strategies tailored to the unique requirements of international clients. 7. Offshore Trusts and Foundations: These structures can provide asset protection, estate planning benefits, and confidentiality for clients seeking to safeguard their wealth and pass it on to future generations. 8. Private Banking: These services typically include personalized financial advice, tailored investment strategies, and exclusive access to premium banking products and services. Adherence to both local and international laws is an essential aspect of offshore banking. It's mandatory that both the account holder and the offshore bank abide by all relevant laws. These can cover laws concerning taxation, anti-money laundering, financial disclosure, and others. Ensuring compliance helps maintain the legality of the offshore account and avoids any potential legal complications in the future. Offshore banking requires adherence to both the tax laws of the account holder's home country and the tax regulations of the offshore jurisdiction. This ensures that any applicable taxes are properly reported and paid, preventing potential tax evasion issues. These accounts are subject to stringent AML laws and regulations. They are obligated to implement robust measures to detect and prevent money laundering, terrorism financing, and other illicit activities. The requirements may vary depending on the jurisdiction, but typically, offshore account holders are required to provide accurate and comprehensive information about their financial activities. This includes disclosing the sources of funds deposited into the offshore account and complying with reporting obligations to the relevant authorities. Deciding on the right jurisdiction is a critical first step in establishing an offshore bank account. The perfect jurisdiction will depend on a variety of factors. These can include the account holder's financial goals, the political and economic stability of the jurisdiction, its banking regulations, and how it is perceived in the international community. It's wise to conduct thorough research or consult with a financial advisor to make an informed decision. Establishing an offshore bank account involves presenting certain documentation and undergoing a verification process. Typically, this includes proof of identity, proof of address, and paperwork related to the source of the funds to be deposited in the account. Each jurisdiction and bank will have specific requirements, and in some instances, the bank may necessitate a personal visit to complete the account opening process. After successfully opening an offshore bank account, there are several ongoing maintenance requirements that the account holder needs to consider. Account holders must maintain a minimum balance set by the offshore bank, failure to which may result in penalties or fees. It is crucial to stay informed about the specified minimum balance threshold and ensure that the account remains funded accordingly. Transaction charges are another aspect of ongoing maintenance that account holders need to consider. Offshore banks may impose fees for various transactions such as withdrawals, transfers, and currency conversions. Account management fees are also part of the ongoing maintenance obligations. These fees cover the administrative costs of maintaining the offshore account and can vary depending on the bank and services provided. Not fulfilling these requirements can lead to penalties or even result in the closure of the account. The reporting requirements may involve disclosing the existence of the offshore account, providing details of transactions, and reporting any income or gains generated from the account. The specific forms and procedures for reporting can vary depending on the home country's tax laws and regulations. To ensure compliance, account holders are advised to consult with tax service professionals or seek guidance from qualified advisors familiar with the reporting obligations in their jurisdiction. Keeping accurate and thorough records of transactions, account statements, and any relevant documentation is crucial for fulfilling reporting requirements. Failing to comply with these reporting requirements can result in severe penalties, hence the importance of staying updated with the reporting regulations. Despite the legitimate reasons for offshore banking, it can sometimes carry a stigma of illegality or tax evasion due to misconceptions. It is, therefore, crucial for individuals and businesses to be transparent about their offshore banking activities and ensure full compliance with all applicable laws to evade this reputational risk. Several offshore jurisdictions have stringent banking secrecy laws, preventing banks from disclosing account information to third parties. This level of privacy is often not available with domestic bank accounts, making it a key benefit for many offshore account holders. In certain jurisdictions, offshore accounts can offer legal means of protecting assets from lawsuits, creditors, or judgments in the account holder's home country. However, it's important to understand that offshore accounts are not meant to be used for hiding assets illegally or evading legitimate debts. Proper legal advice is essential to ensure the correct usage of these accounts. By moving money to a jurisdiction with lower tax rates or more favorable tax laws, individuals and businesses can potentially reduce their tax liability. However, it is crucial to note that tax laws are complex and vary by country, and that tax evasion is illegal. By holding funds in different currencies, individuals and businesses can protect themselves against currency fluctuations in their home country. This can be particularly beneficial for those with international financial interests. Navigating the laws and regulations of multiple countries can be complex and time-consuming, and failure to comply with these laws can result in severe penalties. These can include account setup fees, ongoing account management fees, international transaction fees, and more. These costs can add up, and in some cases, they may outweigh the financial benefits of offshore banking. While many offshore jurisdictions are politically and economically stable, others are not. The risk of political instability, economic crises, or regulatory changes in the offshore jurisdiction can pose risks to the funds held in offshore accounts. An offshore bank account offers financial and legal advantages as a legitimate account opened in a foreign country. Offshore banks provide a range of services, including regular accounts, credit and debit cards, investments, multi-currency accounts, wire transfers, wealth management, trusts, and private banking. Adhering to local and international laws is crucial throughout the process. Setting up an offshore account involves carefully choosing the appropriate jurisdiction, submitting required documents, and completing verification procedures. Ongoing maintenance, reporting obligations, and addressing reputational risks are essential considerations. Offshore banking brings benefits such as enhanced privacy, asset protection, potential tax advantages, and currency diversification. However, it also carries limitations, including legal complexities, higher costs, and the potential risk of financial instability in certain offshore jurisdictions. Prior consideration of both the advantages and limitations is important before proceeding with opening an offshore account.What Is an Offshore Bank Account?

How Offshore Bank Accounts Work

Opening an Offshore Account

Types of Services Offered

Compliance With Local and International Laws

Taxation

Anti-money Laundering (AML)

Financial Disclosure

Setting up an Offshore Bank Account

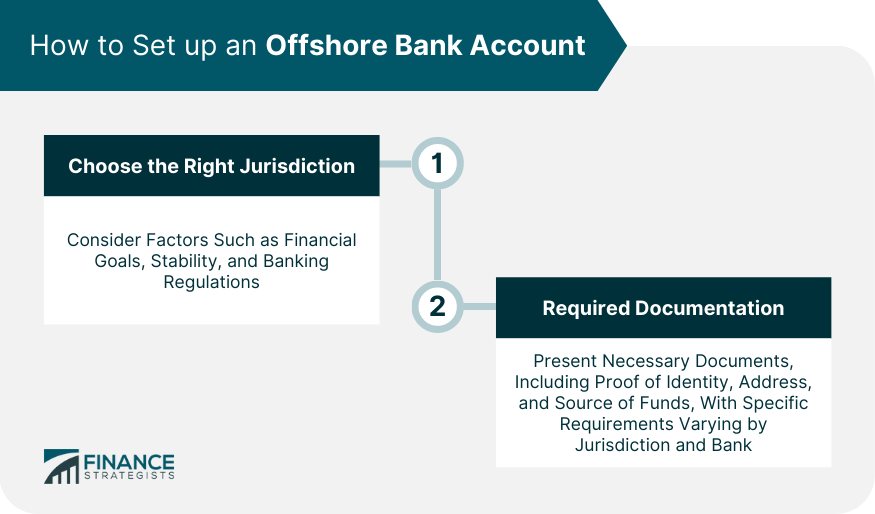

Choose the Right Jurisdiction

Required Documentation and Verification

Maintaining an Offshore Bank Account

Ongoing Maintenance Requirements

Reporting and Compliance Considerations

Addressing Reputational Risk

Benefits of Offshore Bank Accounts

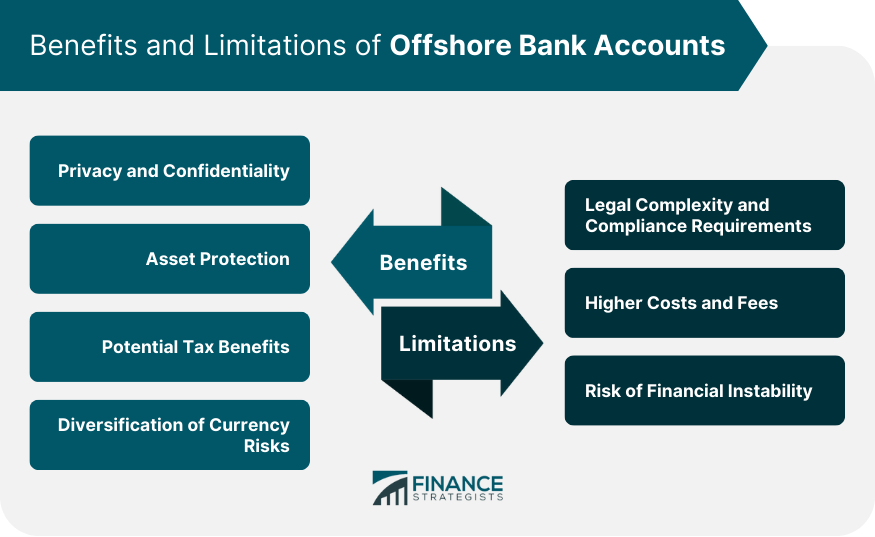

Privacy and Confidentiality

Asset Protection

Potential Tax Benefits

Diversification of Currency Risks

Limitations of Offshore Bank Accounts

Legal Complexity and Compliance Requirements

Higher Costs and Fees

Risk of Financial Instability

Conclusion

Offshore Bank Account FAQs

An offshore bank account is a financial account held in a foreign country by an individual or entity outside their home country.

Yes, offshore bank accounts are legal when used for legitimate purposes. However, it's important to comply with relevant local and international laws and regulations.

Opening an offshore bank account can offer advantages such as increased privacy, asset protection, potential tax benefits, access to a broader range of financial services, and diversification of currency risks.

To open an offshore bank account, you typically need to research and select an appropriate jurisdiction, provide required documentation (such as proof of identity and address), and adhere to the due diligence procedures of the chosen bank.

Some risks and limitations of offshore bank accounts include legal complexities, higher costs, and fees, potential risks associated with financial instability in certain jurisdictions, and the need to comply with reporting requirements in your home country. It's important to fully understand these risks and limitations before opening an offshore account.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.