A Unified Managed Account is a customizable investment management service that combines multiple investment strategies and asset classes into a single account. Unified Managed Accounts have emerged as a popular investment management solution for high-net-worth individuals and institutions. They offer a comprehensive and efficient way to manage a diverse range of investment strategies, asset classes, and investment vehicles within a single account. The main purpose of a UMA is to provide investors with greater flexibility, transparency, and efficiency in managing their investments. Rather than maintaining separate accounts for different investment strategies or asset classes, a UMA allows investors to consolidate their holdings and receive a comprehensive view of their investment portfolio. This consolidated approach simplifies administrative tasks, enhances reporting capabilities, and enables more effective investment decision-making. UMAs are professionally managed investment accounts that consolidate multiple investment strategies and products into one account. They provide a holistic approach to investment management, offering investors a single, unified view of their portfolio, simplifying performance tracking, reporting, and administration. UMAs comprise various investment strategies, asset classes, and investment vehicles, including: UMAs can accommodate a wide range of investment strategies, such as active management, passive management, and alternative investments, providing investors with a diversified and flexible investment approach. UMAs can incorporate multiple asset classes, such as equities, fixed income, real estate, commodities, and alternative investments, facilitating a well-diversified and balanced portfolio. UMAs can hold various investment vehicles, including individual stocks, bonds, exchange-traded funds (ETFs), mutual funds, and separately managed accounts (SMAs), allowing investors to access a broad range of investment opportunities. UMAs offer several advantages over traditional managed accounts, such as: Simplified account administration and reporting Improved tax management Enhanced customization and flexibility Access to a broader range of investment strategies and products Setting up a UMA involves working with a financial advisor to create an account with a custodian or brokerage firm. The advisor will gather information about the investor's financial goals, risk tolerance, time horizon, and tax situation to develop a customized investment plan. An IPS is a critical component of the UMA account setup process, outlining the investor's investment objectives, risk tolerance, time horizon, and other relevant factors. The IPS serves as a roadmap for the financial advisor and investment managers, guiding the investment strategy and decision-making process. UMAs offer a high degree of customization to meet the unique needs and preferences of each investor. Customization factors include: Investors with different risk tolerances can tailor their UMA portfolios to align with their risk appetite, balancing potential returns with the desired level of risk. UMAs can be customized to meet various investment objectives, such as capital preservation, income generation, capital appreciation, or a combination of these goals. The investment time horizon plays a crucial role in determining the appropriate asset allocation and investment strategies within a UMA. UMAs can be designed to optimize after-tax returns, taking into account the investor's tax situation and preferences. The asset allocation process in UMAs involves selecting the appropriate mix of asset classes and investment strategies to achieve the investor's investment objectives while managing risk. Financial advisors and investment managers work together to construct a diversified portfolio that aligns with the investor's IPS. UMAs provide access to a wide range of investment managers, offering expertise in various asset classes and investment strategies. The selection process involves conducting due diligence on the managers, evaluating their investment philosophy, process, and performance. Financial advisors and investment consultants conduct thorough research and due diligence on investment managers, assessing their investment approach, historical performance, risk management, and organizational stability. This process helps ensure that the selected managers align with the investor's investment objectives and risk profile. UMAs can accommodate both active and passive investment management strategies. Active management seeks to outperform the market by selecting individual securities or making tactical asset allocation decisions. Passive management, on the other hand, aims to replicate the performance of a market index through index-tracking investment vehicles, such as ETFs or index funds. Ongoing performance evaluation and monitoring are essential components of the investment management process in UMAs. Financial advisors and investment consultants regularly review the performance of the selected managers, benchmarking their results against relevant market indices and peer groups. This process helps identify underperforming managers and determine if changes to the investment lineup are necessary. Rebalancing is the process of periodically adjusting the portfolio's asset allocation to maintain its target risk profile and investment objectives. This may involve selling assets that have performed well and buying underperforming assets, or replacing underperforming investment managers. Rebalancing helps ensure that the UMA remains aligned with the investor's IPS and risk tolerance. UMAs rely on advanced portfolio management systems to facilitate efficient investment management, trading, and reporting. These systems allow financial advisors and investment managers to monitor the portfolio's performance, risk, and compliance with the IPS. UMAs offer streamlined trading and execution capabilities, enabling financial advisors and investment managers to efficiently implement investment decisions across multiple strategies and asset classes. Performance reporting and analytics are critical components of the UMA experience, providing investors with a clear and comprehensive view of their portfolio's performance, risk, and asset allocation. These tools help investors track their progress toward their investment objectives and make informed decisions about their UMA. UMAs often include account aggregation and data management capabilities, allowing investors to consolidate and monitor their financial assets across multiple accounts and institutions. This feature provides a holistic view of the investor's financial situation and simplifies the financial planning process and reporting process. UMAs facilitate enhanced client communication and reporting, providing investors with regular updates on their portfolio's performance, asset allocation, and investment strategy. This transparency helps build trust and confidence in the investment management process. UMAs typically involve several fee components, including: Investment management fees are charged by the investment managers for managing the portfolio's assets. These fees can vary depending on the investment strategy and asset class. Platform fees are charged by the custodian or brokerage firm for providing the UMA platform, including trading, reporting, and technology services. Advisor fees compensate the financial advisor for their advice and ongoing portfolio management services. UMAs often have a fee structure that is competitive with other investment management options, such as mutual funds, ETFs, and SMAs. The fee transparency and the ability to negotiate fees with the financial advisor and investment managers can result in cost savings for the investor. UMAs can employ tax-aware investing strategies, such as tax-efficient asset location, tax-exempt securities, and tax-advantaged investment vehicles, to help optimize after-tax returns. UMAs can include tax-efficient investment vehicles, such as ETFs and tax-managed mutual funds, which are designed to minimize the impact of taxes on investment returns. Tax-loss harvesting is a strategy employed within UMAs to offset capital gains with capital losses by selling underperforming assets and reinvesting the proceeds in similar assets. This process can help minimize the investor's tax liability while maintaining the desired asset allocation and risk profile. UMAs simplify tax reporting and compliance by consolidating investment transactions, capital gains, and losses within a single account. Financial advisors and custodians provide investors with the necessary tax documents and support to ensure accurate and timely tax filings. UMAs are subject to various regulatory requirements and oversight, depending on the jurisdiction and the specific investment strategies and products included within the account. These regulations aim to protect investors and ensure the integrity of the financial system. Financial advisors and investment managers have a fiduciary responsibility to act in the best interest of their clients when recommending and managing UMAs. This includes ensuring that the investment strategies, products, and fees are suitable and appropriate for the investor's financial situation, goals, and risk tolerance. UMAs are subject to AML and KYC requirements, which involve verifying the identity of the investor and monitoring account activity for suspicious transactions. These requirements help prevent money laundering, terrorist financing, and other illegal activities within the financial system. Unified Managed Accounts have become an increasingly popular investment management solution for investors seeking a comprehensive, flexible, and tax-efficient approach to managing their wealth. By understanding the structure, customization, investment management, technology, fees, tax management, and regulatory considerations of UMAs, investors and financial advisors can make informed decisions about whether a UMA is an appropriate solution for their investment needs. It's important for investors to carefully evaluate the features, fees, and investment management expertise associated with UMAs before selecting a provider. Working with a trusted financial advisor or investment professional can help investors navigate the complexities of UMAs and determine if they align with their investment objectives and preferences.What Is a Unified Managed Account (UMA)?

Overview of Unified Managed Accounts

Concept and Structure of UMAs

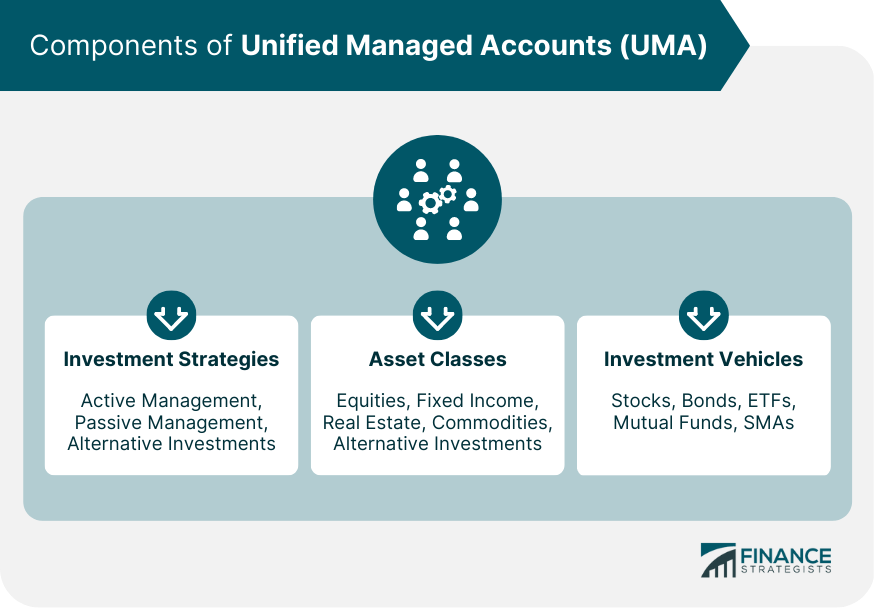

Components of UMAs

Investment Strategies

Asset Classes

Investment Vehicles

Comparison With Traditional Managed Accounts

UMA Account Setup and Customization

Establishing a UMA Account

Developing an Investment Policy Statement (IPS)

Customizing the UMA

Risk Tolerance

Investment Objectives

Time Horizon

Tax Considerations

Asset Allocation and Portfolio Construction

Investment Management in UMAs

Selection of Investment Managers

Manager Research and Due Diligence

Active vs Passive Management

Manager Performance Evaluation and Monitoring

Rebalancing and Manager Replacement

UMA Technology and Operations

Portfolio Management Systems

Trading and Execution

Performance Reporting and Analytics

Account Aggregation and Data Management

Client Communication and Reporting

Fee Structure and Costs

UMA Fee Components

Investment Management Fees

Platform Fees

Advisor Fees

Comparison With Other Investment Management Options

Tax Management in UMAs

Tax-Aware Investing Strategies

Tax-Efficient Investment Vehicles

Tax-Loss Harvesting

Tax Reporting and Compliance

Regulatory and Compliance Considerations

UMA Regulatory Environment

Client Suitability and Fiduciary Responsibilities

Anti-money Laundering (AML) and Know Your Customer (KYC) Requirements

Conclusion

Unified Managed Account (UMA) FAQs

A Unified Managed Account (UMA) is an investment portfolio that combines multiple investment strategies, such as stocks, bonds, and ETFs, into a single account. The UMA platform allows for customized portfolio management and tax efficiency.

The benefits of investing in a UMA include greater flexibility and control over your investments, increased tax efficiency, and the ability to access a wider range of investment strategies. UMAs also offer streamlined account management and reporting.

Unlike a mutual fund, a UMA allows for greater customization and flexibility in investment strategy. UMAs also offer tax benefits that mutual funds may not provide, such as tax loss harvesting and the ability to allocate assets based on tax efficiency.

UMAs are suitable for investors looking for a customized investment strategy and increased control over their portfolio. They are particularly beneficial for high net worth individuals and families, as well as institutions with large investment portfolios.

A UMA platform combines multiple investment strategies into a single account, allowing for more customization and control over the portfolio. The platform may be managed by an investment advisor, who can make investment decisions based on the client's goals, risk tolerance, and other factors. The UMA platform also offers tax management tools and reporting capabilities to help investors optimize their portfolio.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.