The financial planning process is a systematic approach to managing one's finances. It involves evaluating an individual's or family's current financial situation, identifying financial goals, creating a plan to achieve those goals, implementing the plan, and regularly monitoring and adjusting the plan as needed. The process can help individuals make informed decisions about their money, which can have a significant impact on their quality of life. The financial planning process typically includes several key steps, such as gathering financial information, setting financial goals, analyzing the financial situation, developing a financial plan, implementing the plan, monitoring the plan, and making adjustments as needed. By following this process, individuals can create a roadmap for achieving their financial objectives, such as saving for retirement, paying off debt, buying a home, or funding a child's education. The process can be done on one's own, or with the help of a financial planner, who can provide expertise and guidance in areas such as investment planning, retirement planning, tax planning, and risk management. The financial planning process is an ongoing one, as financial situations and goals can change over time, and it's important to regularly review and adjust the plan as necessary. Short-term goals typically range from three months to three years. Examples include building an emergency fund, paying off credit card debt, and saving for a vacation. Medium-term goals have a time horizon of three to ten years. Examples include saving for a down payment on a house, funding a child's education, or starting a business. Long-term goals have a time horizon of more than ten years. Examples include saving for retirement, paying off a mortgage, or leaving a legacy. Collect relevant personal information, such as age, marital status, number of dependents, and employment status. Compile a list of all financial assets (e.g., savings, investments, real estate) and liabilities (e.g., loans, credit card debt). Record all sources of income and monthly expenses to understand your cash flow. Calculate net worth by subtracting total liabilities from total assets. Analyze income and expenses to identify patterns, potential savings, and areas for improvement. Calculate the debt-to-income ratio by dividing total monthly debt payments by gross monthly income. This ratio helps assess overall financial health. Evaluate your risk tolerance based on factors such as age, investment horizon, and financial goals. Create a budget to manage income, expenses, and savings effectively. Develop an investment strategy that aligns with your risk tolerance and financial goals. Implement strategies to minimize tax liabilities and maximize tax-advantaged opportunities. Evaluate and obtain appropriate insurance coverage to protect against potential financial losses. Create a retirement plan that meets your desired lifestyle and financial needs in retirement. Develop an estate plan that ensures the efficient transfer of assets to beneficiaries and minimizes potential tax liabilities. Determine which financial goals and strategies are most important and should be addressed first. Allocate financial resources (e.g., savings, investments) to achieve your financial goals effectively. Consult financial professionals, such as financial planners or investment advisors, to ensure a well-informed financial plan. Conduct regular reviews of your financial plan to track progress and make adjustments as needed. Update your financial plan to account for changes in personal circumstances or external factors, such as job loss, marriage, or economic conditions. Revise financial goals and strategies to align with your evolving financial situation and priorities. Financial planners help clients create comprehensive financial plans tailored to their unique goals and circumstances. CPAs provide tax planning and preparation services, as well as financial advice on various aspects of personal finance. Investment advisors assist clients in developing and managing investment portfolios based on their risk tolerance and financial objectives. Insurance agents help clients identify their insurance needs and select appropriate coverage to protect against potential financial losses. Estate planning attorneys assist clients in creating estate plans, including wills and trusts, to ensure the efficient transfer of assets and minimize potential tax liabilities. Delaying financial planning can lead to missed opportunities and increased financial stress. Start planning early to maximize your financial potential. A well-diversified investment portfolio can help reduce risk and increase the potential for long-term returns. Avoid concentrating your investments in a single asset class or market sector. Failing to obtain adequate insurance coverage can leave you vulnerable to financial losses. Regularly review your insurance needs and adjust coverage as necessary. Neglecting retirement planning can result in insufficient savings to maintain your desired lifestyle during retirement. Start saving early and regularly review your retirement plan. Failing to create an estate plan can lead to confusion and disputes among your beneficiaries. Consult an estate planning attorney to develop a plan that reflects your wishes and minimizes potential tax liabilities. The financial planning process is essential for achieving financial goals and maintaining overall financial well-being. By establishing goals, gathering and analyzing financial data, developing a plan, implementing it, and regularly monitoring and adjusting the plan, individuals can take control of their personal finances. Seeking the advice of financial professionals and avoiding common mistakes can further enhance the effectiveness of the financial planning process.What Is the Financial Planning Process?

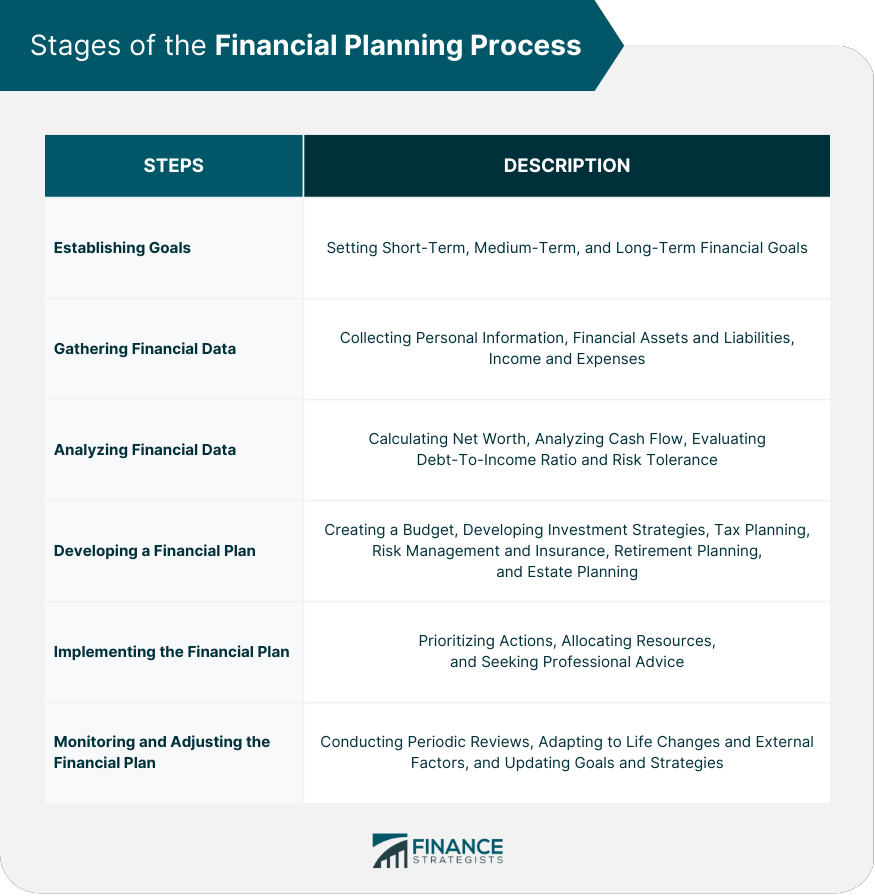

Stages of the Financial Planning Process

Establishing Goals

Short-Term Goals

Medium-Term Goals

Long-Term Goals

Gathering Financial Data

Personal Information

Financial Assets and Liabilities

Income and Expenses

Analyzing Financial Data

Net Worth Calculation

Cash Flow Analysis

Debt-To-Income Ratio

Risk Tolerance Assessment

Developing a Financial Plan

Budgeting and Cash Flow Management

Investment Strategies

Tax Planning

Risk Management and Insurance

Retirement Planning

Estate Planning

Implementing the Financial Plan

Prioritizing Actions

Allocating Resources

Seeking Professional Advice

Monitoring and Adjusting the Financial Plan

Periodic Reviews

Adapting to Life Changes and External Factors

Updating Goals and Strategies

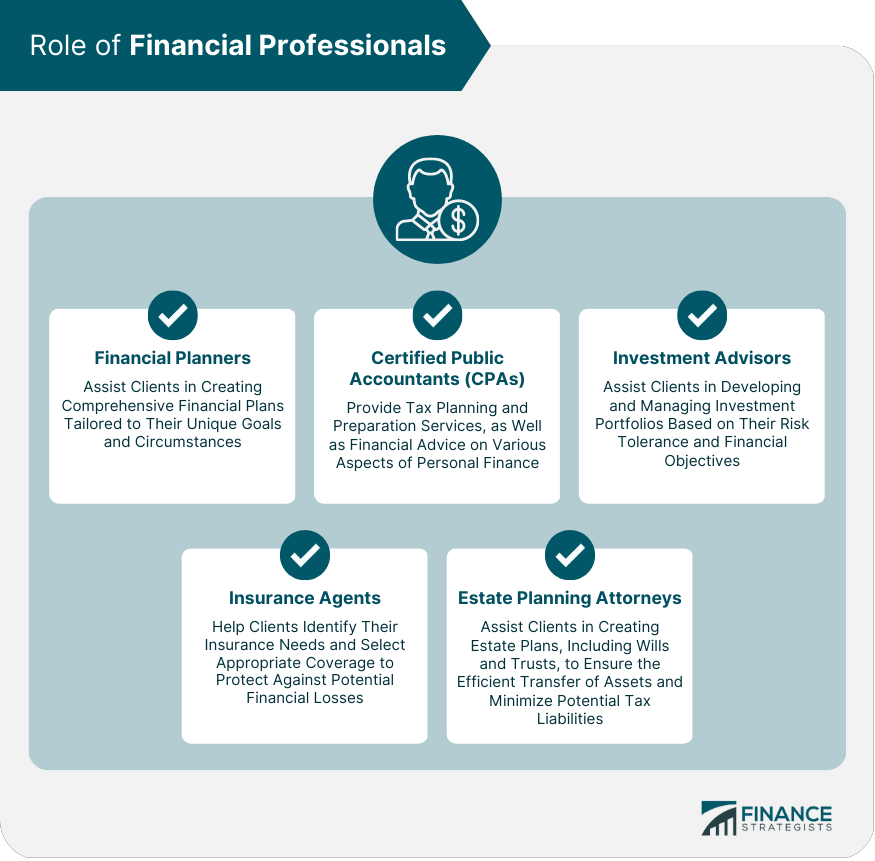

Role of Financial Professionals

Financial Planners

Certified Public Accountants (CPAs)

Investment Advisors

Insurance Agents

Estate Planning Attorneys

Common Financial Planning Mistakes

Procrastination

Lack of Diversification

Insufficient Insurance Coverage

Inadequate Retirement Planning

Neglecting Estate Planning

Conclusion

Financial Planning Process FAQs

The Financial Planning Process is a comprehensive and ongoing approach to managing one's finances. It involves evaluating one's current financial situation, identifying financial goals, creating a plan to achieve those goals, implementing the plan, and regularly monitoring and adjusting the plan as needed.

The Financial Planning Process is important because it helps individuals and families make informed decisions about their money, which can have a significant impact on their quality of life. It provides a roadmap for achieving financial goals, such as buying a home, saving for retirement, or paying for a child's education.

The steps in the Financial Planning Process typically include: (1) gathering financial information, (2) setting financial goals, (3) analyzing the financial situation, (4) developing a financial plan, (5) implementing the plan, (6) monitoring the plan, and (7) making adjustments as needed.

While it is possible to go through the Financial Planning Process on your own, many people find it helpful to work with a financial planner. A financial planner can provide expertise and guidance in areas such as investment planning, retirement planning, tax planning, and risk management.

It is recommended that you review your financial plan at least once a year or whenever there is a significant change in your financial situation, such as a change in income or an unexpected expense. Regular reviews can help ensure that your plan remains relevant and effective in helping you achieve your financial goals.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.