A surety bond is a type of bond that serves to guarantee that the principal will fulfill the terms of a contract. Within the realm of contract law, it is a legally binding agreement wherein three parties— the principal, the obligee, and the surety— are involved. Should the principal be unable to meet contractual obligations, the surety bond safeguards the interests of the obligee. However, the intricacies of surety bonds extend beyond this simplistic explanation. Primarily, a surety bond imbues confidence in the transaction, as it assures the obligee that contractual obligations will be met. It presents a risk-mitigation tool that protects the obligee from losses, if the principal fails to fulfill the contract. For instance, contractors bidding for government projects are often required to present a surety bond. This not only promotes an atmosphere of trust and reliability but also ensures adherence to professional standards and ethics. A bid bond is an essential tool for businesses seeking public contracts. It guarantees that a contractor bidding on a project will honor the bid and sign the contract if awarded. The bid bond keeps the bidding process fair and competitive. This type of bond reassures the project owner, the obligee, that they won't incur losses due to an inadequate bid. By ensuring that contractors stand by their bids, it dissuades frivolous bids and maintains the integrity of the contracting industry. Performance bonds follow bid bonds in the contractual journey. Once a contractor wins a bid, a performance bond ensures that they will execute the project as per the agreed terms. If the contractor fails to complete the project or doesn't meet the standards stipulated in the contract, the obligee can make a claim on the bond. Performance bonds inspire confidence among project owners and safeguard their interests. They act as a guarantee, ensuring that the project sees fruition as per the outlined terms, and protects the obligee against contractor default. Payment bonds secure the interests of subcontractors, laborers, and suppliers involved in a project. These bonds assure that these parties will receive their due payment for services rendered or materials supplied. They function as a safety net, ensuring that subcontractors and suppliers do not bear the financial brunt if the principal defaults on payment. This type of bond promotes ethical business practices and fosters a healthy work environment. License and permit bonds are critical in certain industries where businesses require licenses or permits to operate. These bonds guarantee that businesses adhere to laws, regulations, and professional ethics associated with their license or permit. In case of any violation, claims can be made against the bond. These bonds help uphold the industry standards. They promote ethical business practices and protect the interests of consumers and governing bodies alike. Court bonds, also known as judicial bonds, are required in certain court proceedings. They assure compliance with a court order, such as the payment of costs, or the execution of fiduciary duties. They serve to protect the interests of the opposing party against potential losses resulting from the court's decision. Court bonds instill a sense of security in the justice system. They ensure that court orders are fulfilled and safeguard the interests of the concerned parties, thereby maintaining the integrity of legal proceedings. Fidelity bonds, often used within the context of employment, offer protection to businesses against employee theft, embezzlement, or fraud. They serve as an insurance policy, shielding businesses from losses resulting from dishonest acts by their employees. Fidelity bonds are instrumental in fostering a secure work environment. They promote trust between employers and employees and protect businesses from potential financial losses. In a surety bond, the obligee is the party that receives the assurance of performance. This party is the beneficiary, typically protected against losses resulting from the principal's failure to meet contractual obligations. Obligees could range from project owners and businesses to government entities and consumers, depending on the bond type. The obligee's role is crucial as they set the bond's terms. They also have the right to claim against the bond if the principal defaults. Ultimately, the obligee is safeguarded, fostering an environment of trust and confidence in commercial transactions. The principal, in a surety bond, is the party who obtains the bond to assure performance of contractual obligations. Principals could be contractors, businesses, or individuals, depending on the bond type. They are obliged to perform as per the bond's terms. It's the principal's responsibility to fulfill all agreed-upon obligations. In case of a default, the principal must reimburse the surety for any claims paid. Thus, the principal's role underpins the functioning of the surety bond, making them a key player in the process. The surety, often an insurance company, guarantees the principal's performance to the obligee in a surety bond. The surety steps in if the principal defaults, protecting the obligee from financial loss. The surety's role is pivotal as they undertake a thorough evaluation process to determine the principal's capability to fulfill the bond's obligations. Post issuance, the surety stands as the guarantor, liable to compensate the obligee in case of a default. Obtaining a surety bond begins with an application process. The principal must provide necessary information about their business and the bond needed. Details like financial history, credit score, and business experience play a significant role in the underwriting process. The underwriting process is an evaluation of the principal's ability to meet the bond's terms. The surety assesses the principal's creditworthiness, financial stability, and industry experience. This risk assessment determines whether the surety will issue the bond and at what premium rate. Once the underwriting process is complete, and if the principal is deemed capable of meeting the bond's terms, the surety issues the bond. The bond is a legal document that clearly states the obligations of each party— the principal, the obligee, and the surety. Upon issuance, the bond is transferred to the obligee. This provides the obligee with the assurance that the principal will fulfill the contractual obligations. In case of a default, the obligee can make a claim against the bond. The premium for a surety bond is a percentage of the total bond amount. It is determined during the underwriting process, based on the principal's creditworthiness and the risk associated with the bond. The premium is usually paid annually, and the principal is responsible for this payment. Additional fees may also be involved in the process, such as application fees or renewal fees. It's essential for the principal to be aware of these costs when obtaining a surety bond. Surety bonds offer significant protection by mitigating risk. They shield the obligee from potential losses if the principal fails to meet contractual obligations. This risk management tool can be instrumental in preventing financial loss, making surety bonds an attractive proposition in many business transactions. The protective nature of surety bonds extends to other parties as well, depending on the type of bond. For instance, payment bonds safeguard subcontractors and suppliers, while fidelity bonds protect businesses against dishonest acts by their employees. A surety bond enhances the credibility of the principal. It signifies that a neutral third party, the surety, has vetted the principal's ability to meet contractual obligations. This boosts the trustworthiness of the principal in the eyes of the obligee. Moreover, surety bonds engender trust within the industry. They ensure that businesses adhere to industry standards and regulations, thereby promoting professionalism and ethics. Surety bonds can also lead to cost savings. They prevent losses from contractual default, thereby saving potential expenditure for the obligee. For the principal, a surety bond might increase the chance of winning contracts, contributing to business growth and profitability. Additionally, the underwriting process often highlights areas of improvement in the principal's operations. This can lead to enhanced efficiency and reduced costs in the long run. Thus, surety bonds can have indirect economic benefits for both the principal and the obligee. One such risk is the potential liability of the principal. If the principal defaults on the bond's terms, they are liable to reimburse the surety for any claims paid. This can lead to significant financial liability for the principal. Furthermore, if the principal is unable to reimburse the surety, it may lead to legal consequences or a damaged reputation. Thus, the principal must ensure that they are capable of meeting the bond's obligations before obtaining a surety bond. If the principal defaults, the surety is obliged to compensate the obligee. This puts the surety at financial risk. Moreover, if the principal is unable to reimburse the surety, the surety might have to bear the loss. This highlights the importance of a thorough underwriting process to assess the principal's ability to fulfill the bond's terms. While it's less common, there's also a risk of default by the obligee. For instance, an obligee might wrongfully declare a principal in default and make a claim against the bond. Such scenarios can lead to unnecessary complications and financial strain for the principal and the surety. Therefore, all parties involved should act in good faith and adhere to the bond's terms to minimize potential risks. When selecting a surety bond, one of the primary considerations should be the financial stability of the surety. The surety must have a solid financial footing to fulfill its obligations in case of a default by the principal. Principals can refer to the surety's financial ratings from reputable rating agencies, such as A.M. Best or Standard & Poor's, to gauge their financial strength. This can provide a reliable measure of the surety's ability to meet their obligations. Principals should thoroughly evaluate the terms and conditions of the bond before agreeing to them. These terms stipulate the obligations of the principal and the circumstances under which a claim can be made. Understanding the bond's terms can help prevent potential disputes or misunderstandings in the future. It can also ensure that the principal is capable of fulfilling the bond's obligations. Finally, the principal should assess the obligee's requirements. Different obligees might have different bond requirements, depending on the industry, project size, or regulatory stipulations. By understanding the obligee's requirements, the principal can ensure that they select the right type of bond and meet the necessary conditions. This can help to facilitate smooth business transactions and foster good relationships with the obligee. Surety bonds provide a guarantee that contractual obligations will be fulfilled. They involve three parties: the principal, who is obligated to perform a task; the obligee, who is the recipient; and the surety, who guarantees the principal's performance. There are numerous types of surety bonds such as bid bonds ensuring the commitment of contractors to license and permit bonds ensuring regulatory compliance, these instruments help uphold standards and foster trust in commercial transactions. While surety bonds offer numerous advantages such as risk mitigation, enhanced credibility, and cost savings, they also come with potential risks. The liability of the principal, financial exposure of the surety, and potential default by the obligee are some risks associated with surety bonds. When selecting a surety bond, consider factors like the financial stability of the surety, the bond's terms and conditions, and the obligee's requirements. This can ensure a smooth bond process and foster successful business relationships.What Are Surety Bonds?

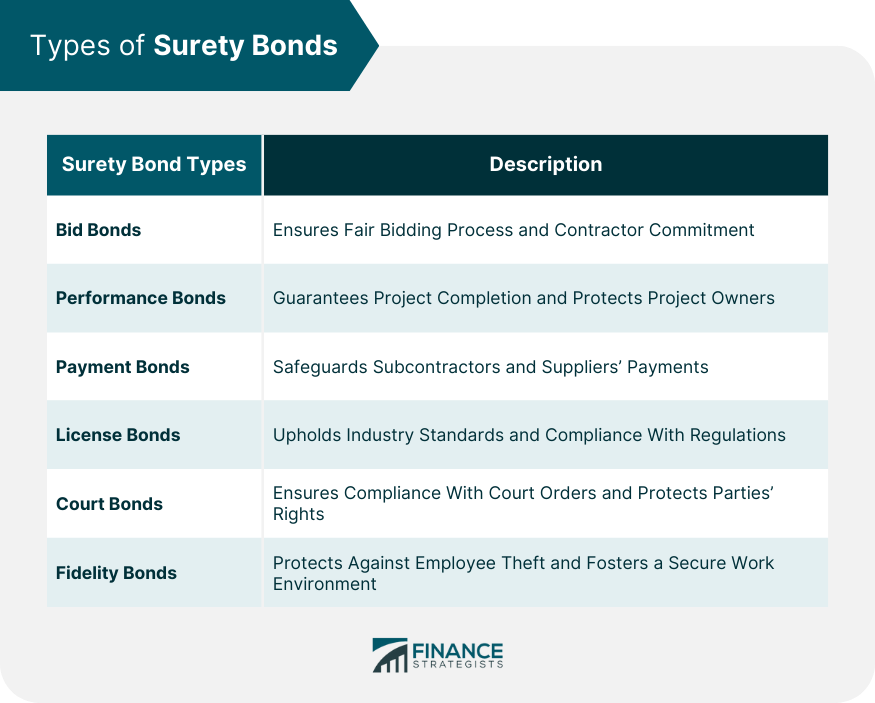

Types of Surety Bonds

Bid Bonds

Performance Bonds

Payment Bonds

License and Permit Bonds

Court Bonds

Fidelity Bonds

Roles and Parties Involved in Surety Bonds

Obligee

Principal

Surety

Process of Obtaining Surety Bonds

Application and Underwriting

Issuance of the Bond

Premiums and Fees Payment

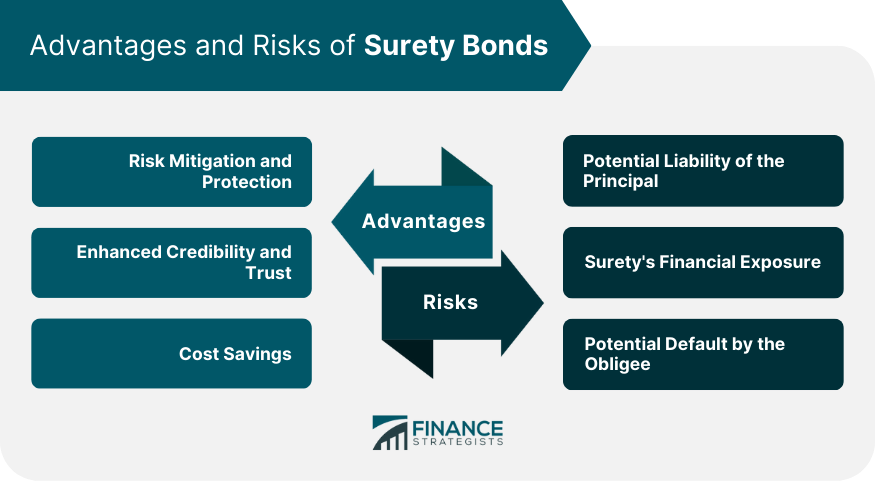

Advantages of Surety Bonds

Risk Mitigation and Protection

Enhanced Credibility and Trust

Cost Savings

Potential Risks of Surety Bonds

Potential Liability of the Principal

Surety's Financial Exposure

Potential Default by the Obligee

Considerations for Selecting Surety Bonds

Financial Stability of the Surety

Evaluation of the Bond's Terms and Conditions

Assessing the Obligee's Requirements

Conclusion

Surety Bonds FAQs

A surety bond is a legally binding contract involving three parties—the principal, the obligee, and the surety. It guarantees that the principal will fulfill the terms of a contract, with the surety compensating the obligee if the principal fails to do so.

There are various types of surety bonds including bid bonds, performance bonds, payment bonds, license and permit bonds, court bonds, and fidelity bonds. Each serves a unique purpose and protects the interests of specific parties.

A surety bond involves three parties: the principal, who needs the bond; the obligee, who requires the bond from the principal; and the surety, who provides the bond guarantee.

Surety bonds offer several benefits, including risk mitigation, enhanced credibility and trust, and potential cost savings. They protect the obligee from financial loss if the principal fails to meet contractual obligations and enhance the principal's reputation in the market.

While beneficial, surety bonds also come with potential risks. These include the potential liability of the principal, financial exposure of the surety, and potential default by the obligee. Therefore, careful consideration should be taken when entering into a surety bond agreement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.