Cost segregation is a strategic tax planning tool businesses and real estate owners use to accelerate depreciation deductions on their property. By identifying and separating tangible personal property and land improvements from the building structure, taxpayers can allocate costs to different asset classes with shorter depreciation periods. This results in accelerated tax deductions and increased cash flow for the business or property owner. The main purpose of cost segregation is to optimize cash flow by maximizing tax savings. It is particularly useful for property owners who have recently constructed, purchased, or renovated a building. By leveraging cost segregation, taxpayers can significantly reduce their tax liability, improve cash flow, and potentially enhance the overall return on investment. Cost segregation is crucial in business and property owners' tax planning and cash flow optimization. Taxpayers can take advantage of accelerated depreciation deductions by reallocating costs to asset classes with shorter depreciation periods. This lowers the taxable income and increases the net present value of the tax savings, which can be reinvested back into the business. Cost segregation can improve financial performance by increasing the available cash flow. This additional cash flow can be used to fund operations, repay debt, invest in new opportunities, or distribute to shareholders. In short, cost segregation is a valuable tool for financial management and strategic decision-making. Tangible personal property (TPP) refers to assets that are not permanently attached to the building structure and can be removed without causing damage. Examples of TPP include machinery, equipment, furniture, and fixtures. These assets typically have shorter depreciation periods ranging from 5 to 15 years. Under the Modified Accelerated Cost Recovery System (MACRS), tangible personal property is generally depreciated using the double-declining balance method, which provides larger depreciation deductions in the earlier years of the asset's life. By segregating and reallocating costs to TPP, taxpayers can take advantage of accelerated depreciation and generate significant tax savings. Land improvements are enhancements made to a piece of land, such as landscaping, parking lots, sidewalks, or fencing. These improvements generally have a depreciation period of 15 years under MACRS, making them another attractive asset class for cost segregation purposes. Since land improvements depreciate faster than the building structure, allocating costs to this category can result in accelerated tax deductions and improved cash flow. Properly identifying and classifying land improvements is essential for maximizing the benefits of cost segregation. Building structures are a property's physical components, such as walls, roofs, and foundations. Under MACRS, the depreciation period for non-residential buildings is 39 years, while residential rental properties have a 27.5-year depreciation period. This is significantly longer than the depreciation periods for tangible personal property and land improvements. By allocating costs to the building structure, taxpayers can spread depreciation deductions over a longer period, resulting in smaller annual deductions. However, when cost segregation is applied, some of these costs can be reallocated to shorter-lived assets, increasing tax savings and cash flow. The land is the underlying property on which a building is constructed. Unlike other components in a cost segregation study, the land is not depreciable. This means that any costs allocated to land will not generate depreciation deductions for tax purposes. Accommodating costs between land and other asset categories is essential during a cost segregation study. Over-allocating costs to land can result in missed opportunities for tax savings, while under-allocating can lead to audit risks and potential tax penalties. A cost segregation study is a detailed engineering and accounting analysis that identifies and reallocates costs to various asset categories based on their respective depreciation periods. The primary purpose of a cost segregation study is to optimize tax savings and cash flow by accelerating depreciation deductions. The benefits of conducting a cost segregation study include the following: Maximizing tax savings by identifying and reallocating costs to shorter-lived assets. Improving cash flow by accelerating depreciation deductions. Enhancing the overall return on investment for property owners. Facilitating accurate asset tracking and management. Identifying potential tax credits and incentives for energy efficiency or other qualifying activities. Cost segregation studies require a multidisciplinary team of professionals with engineering, accounting, and tax law expertise. Engineers typically have experience in construction, architecture, or related fields and are responsible for identifying and classifying assets. Accountants and tax professionals are responsible for ensuring compliance with tax regulations and proper allocation of costs. It is essential to work with experienced professionals to ensure the accuracy and reliability of the cost segregation study. Inaccurate studies can lead to missed tax savings or increased audit risks, negating the potential benefits of cost segregation. A comprehensive cost segregation study typically includes the following components: Preliminary Analysis: An initial assessment determines a cost segregation study's feasibility and potential benefits. This involves a high-level review of the property and its cost components and estimating the potential tax savings and cash flow improvements. Data Collection: Relevant data, such as construction documents, purchase agreements, invoices, and asset registers, is collected and reviewed. This information identifies and classifies the assets and appropriately allocates costs. Engineering Analysis: A detailed engineering analysis is conducted to identify and classify the various assets, including tangible personal property, land improvements, and building structures. Asset Classification: Assets are classified into their respective asset categories based on their depreciation periods. This is a critical step in the cost segregation process, as it determines the allocation of costs and subsequent tax savings. Cost Allocations: Costs are allocated to the identified asset categories based on engineering estimates, actual costs, or other appropriate methods. Proper cost allocation is crucial for ensuring the accuracy and reliability of the cost segregation study. Documentation and Report Preparation: A comprehensive report detailing the cost segregation study's methodology, findings, and conclusions is prepared. Accelerated depreciation is a key benefit of cost segregation, allowing taxpayers to claim larger depreciation deductions in the earlier years of an asset's life. Under the Modified Accelerated Cost Recovery System (MACRS), most assets are depreciated using the double-declining balance method, which results in accelerated depreciation. Taxpayers can use accelerated depreciation and generate significant tax savings by reallocating costs to shorter-lived assets through a cost segregation study. This lowers the taxable income and increases the net present value of the tax savings, which can be reinvested back into the business. Cost segregation can also be used in conjunction with other tax deferral strategies to optimize tax savings and cash flow further. Some common strategies include: Like-Kind Exchanges (Section 1031): This provision allows taxpayers to defer capital gains taxes on the sale of a property by reinvesting the proceeds into a similar property. Opportunity Zones: These are economically distressed areas where new investments may be eligible for preferential tax treatment. Taxpayers who invest in an Opportunity Zone can defer and potentially reduce their capital gains tax liability. Cost segregation studies can help identify potential tax credits and incentives for energy efficiency, historical preservation, or other qualifying activities. Some common tax credits and incentives include: Energy-Efficient Property Credits: Tax credits may be available for businesses and property owners who invest in energy-efficient property, such as solar panels, wind turbines, or geothermal heat pumps. Rehabilitation Tax Credits: These credits are available for taxpayers rehabilitating qualified historic buildings or structures. While cost segregation can provide significant tax benefits, it is important to be aware of potential audit risks and ensure compliance with applicable tax regulations. The IRS has issued guidelines and audit techniques for cost segregation studies, and taxpayers should ensure their studies are conducted in accordance with these guidelines. Working with experienced professionals and maintaining thorough documentation can help mitigate audit risks and ensure the accuracy and reliability of the cost segregation study. In the event of an audit, having a well-prepared and documented study can help support the taxpayer's position and minimize potential tax penalties. The Tax Cuts and Jobs Act (TCJA), enacted in 2017, introduced several changes to the tax code that can impact cost segregation studies. Some key provisions include: Increased Bonus Depreciation: The TCJA allows for 100% bonus depreciation on qualified property acquired and placed in service after September 27, 2017, and before January 1, 2023. Changes to Qualified Improvement Property (QIP): The TCJA initially intended to classify QIP as a 15-year property eligible for bonus depreciation. However, a drafting error resulted in QIP being classified as a 39-year property. The CARES Act, enacted in response to the COVID-19 pandemic, included several tax provisions that can impact cost segregation studies: Correction of the QIP Drafting Error: As mentioned above, the CARES Act corrected the QIP classification error in the TCJA, making QIP eligible for 15-year depreciation and 100% bonus depreciation retroactively from 2018. Net Operating Loss (NOL) Carrybacks: The CARES Act temporarily allows businesses to carry back NOLs generated in tax years 2018, 2019, and 2020 for up to five years. The IRS has issued guidance and rulings related to cost segregation, providing taxpayers with a framework for conducting studies and ensuring compliance with tax regulations. Some key guidance and rulings include: Cost Segregation Audit Techniques Guide (ATG): The IRS published the ATG to provide guidelines for conducting cost segregation studies and to assist IRS examiners in auditing these studies. Private Letter Rulings (PLRs) and Revenue Rulings: The IRS has issued several PLRs and Revenue Rulings related to cost segregation, providing clarification and guidance on various issues. Tax laws and regulations constantly evolve, and taxpayers must stay current with any legislative or regulatory changes impacting their cost segregation studies. Working with experienced tax professionals can help taxpayers navigate these changes and ensure their cost segregation studies remain compliant and effective in maximizing tax savings and cash flow. Cost segregation is an essential tax planning tool for businesses and property owners looking to optimize cash flow and maximize tax savings. By conducting a thorough cost segregation study, taxpayers can accelerate depreciation deductions, reduce tax liability, and improve overall financial performance. It is crucial to work with experienced professionals and stay current with legislative and regulatory developments to ensure the accuracy and reliability of cost segregation studies. By doing so, taxpayers can capitalize on the numerous benefits of cost segregation and make more informed decisions about their financial management and strategic investments.What Is Cost Segregation?

Components of Cost Segregation

Tangible Personal Property

Land Improvements

Building Structures

Land

Cost Segregation Study

Purpose and Benefits

Professional Requirements

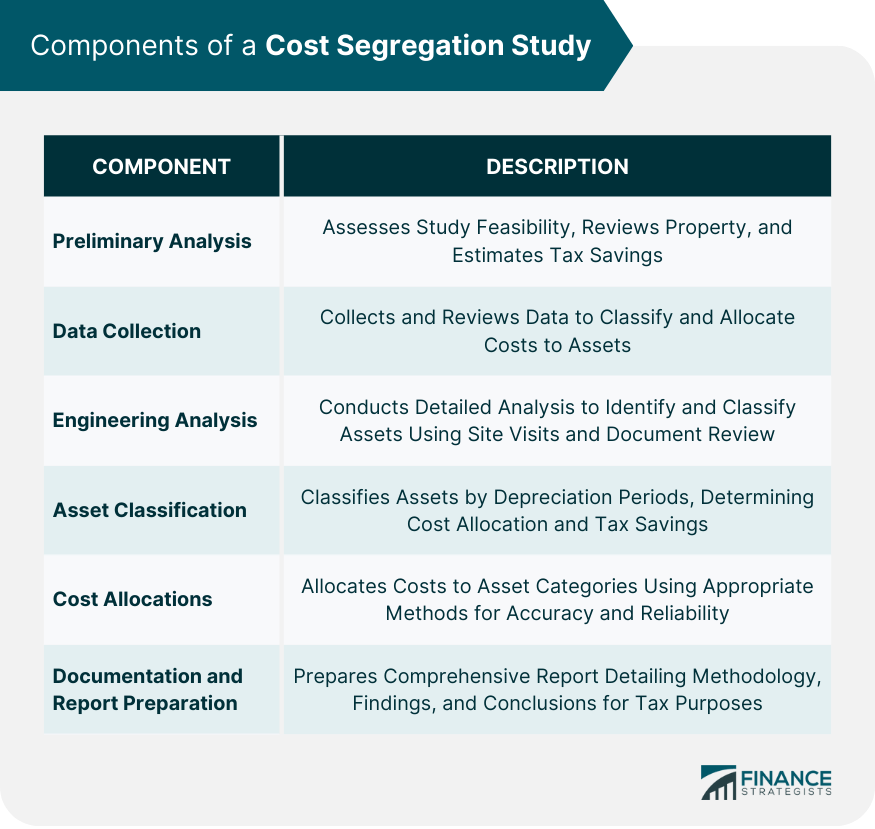

Components of a Cost Segregation Study

This process may involve site visits, interviews with construction personnel, and a thorough review of construction documents.

This report serves as documentation for tax purposes and should be prepared to withstand potential IRS scrutiny.

Tax Implications

Accelerated Depreciation

Tax Deferral Strategies

By combining cost segregation with a like-kind exchange, taxpayers can maximize depreciation deductions on the replacement property, further enhancing the tax deferral benefits.

Combining cost segregation with investments in Opportunity Zones can result in additional tax savings and increased cash flow.Tax Credits and Incentives

Cost segregation can help identify qualifying assets and maximize the tax benefits associated with these investments.

Property owners can identify qualifying rehabilitation expenditures and maximize the associated tax credits by conducting a cost segregation study.Audit Risks and Considerations

Recent Legislation and Regulatory Updates

Tax Cuts and Jobs Act (TCJA) Implications

This provision allows taxpayers to immediately deduct the full cost of eligible assets in the year they are placed in service, further enhancing the benefits of cost segregation.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed in 2020, corrected this error and made the change retroactive to 2018.CARES Act and Its Impact on Cost Segregation

This provision can enhance the tax benefits of cost segregation by allowing taxpayers to offset past taxable income with accelerated depreciation deductions.IRS Guidance and Rulings

Taxpayers should ensure their cost segregation studies adhere to the principles outlined in the ATG to minimize audit risks and ensure the accuracy and reliability of their studies.

Taxpayers should consult these rulings to ensure their cost segregation studies are conducted in accordance with IRS guidance.Future Legislative Developments

Conclusion

Cost Segregation FAQs

Cost segregation is a tax planning strategy that involves identifying and reclassifying assets within a property to accelerate depreciation deductions. By doing so, property owners can reduce their current taxable income and increase cash flow.

A cost segregation study is a detailed analysis of a property's assets to determine their appropriate depreciation categories. It involves engineering analysis, asset classification, cost allocations, and report preparation. The study allows property owners to maximize tax savings by accelerating depreciation on eligible assets.

Cost segregation studies can be conducted on various types of properties, including commercial, industrial, and residential rental properties. Properties that have undergone new construction, renovation, or acquisition may also benefit from a cost segregation study.

The tax savings from a cost segregation study result from accelerated depreciation deductions on certain assets. Property owners can reduce their taxable income, defer taxes, and improve cash flow by reclassifying assets into shorter depreciation periods. The specific savings depend on the property's assets and tax situation.

The best time to conduct a cost segregation study is typically during the year of property acquisition, construction, or renovation. However, property owners can also perform a "look-back" study on previously acquired properties to claim missed depreciation deductions and file for tax adjustments.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.