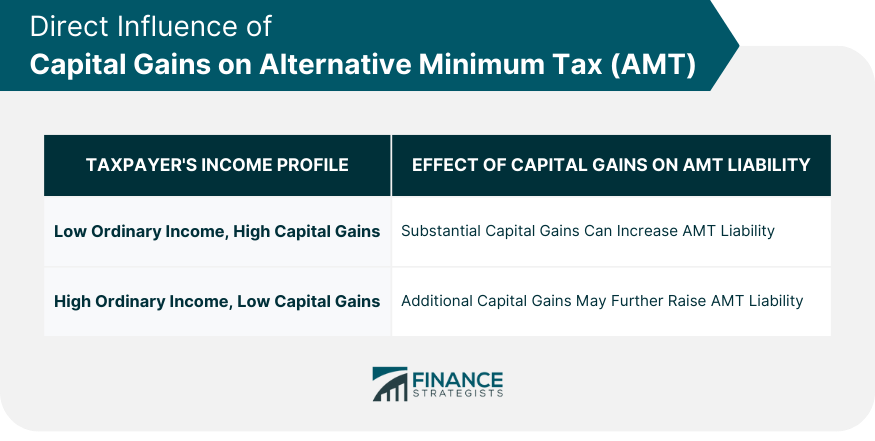

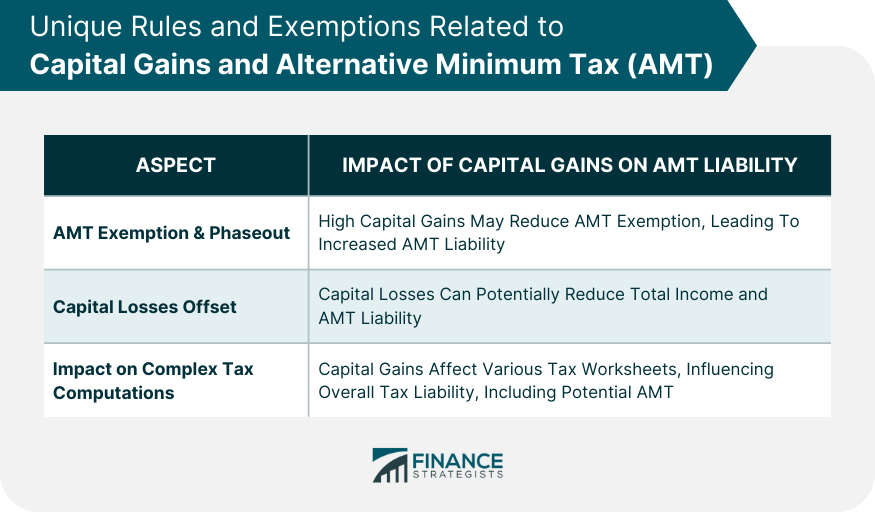

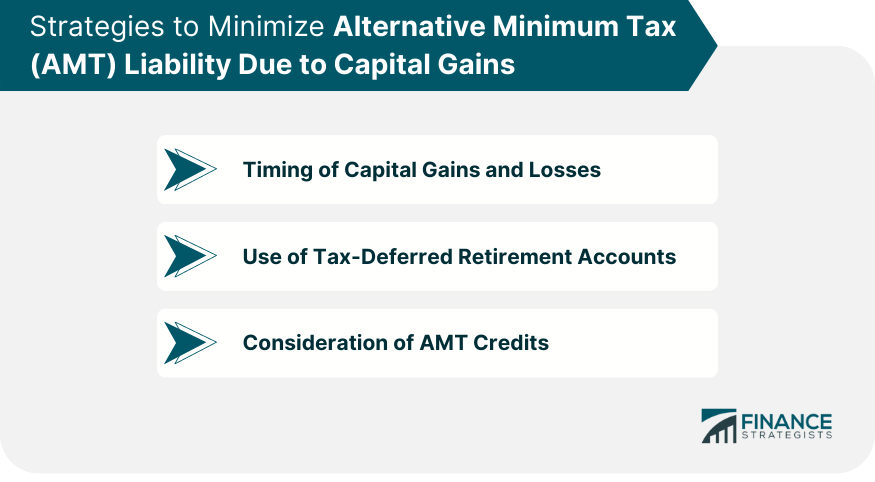

The Alternative Minimum Tax (AMT) is designed to ensure that high-income individuals and corporations pay a minimum amount of tax, regardless of deductions, credits, or exemptions. It is parallel to the standard tax system and operates with its own set of rules. In the context of AMT, both long-term and short-term capital gains are critical factors that can alter an individual's tax obligation. Long-term capital gains, derived from the sale of an asset held for more than a year, are generally taxed at a lower rate than ordinary income. Short-term capital gains, resulting from assets held for a year or less, are taxed as ordinary income. In the realm of AMT, these gains can indirectly increase AMT liability because they contribute to the taxpayer's overall income, thereby potentially pushing the taxpayer into the AMT zone if their total income exceeds the AMT exemption amount. Further, the tax rates for capital gains under the AMT system are the same as under the regular tax system. Therefore, even though the rates might not directly affect the AMT calculation, the increased income could make other income subject to the AMT, influencing the overall tax liability. To better grasp this concept, let's consider two hypothetical scenarios. First, imagine a taxpayer with a relatively low ordinary income but high capital gains. If the capital gains are substantial enough to push the taxpayer's income above the AMT exemption level, they may find themselves liable for the AMT despite their low ordinary income. The second scenario involves a high-income individual with low capital gains. In this case, although the capital gains are minor, the person's high income might already place them in the AMT zone. Any additional income, including capital gains, could potentially increase the AMT liability because it might reduce the amount of AMT exemption available to them. While capital gains may not directly cause AMT liability, they may indirectly influence it by raising the taxpayer's total income, thereby reducing the available AMT exemption. The AMT system has its own exemption amount and phaseout thresholds that differ from the regular tax system. The exemption begins to phase out at certain income levels, meaning that high income, including high capital gains, can reduce the amount of exemption and thereby increase AMT liability. On the other hand, capital losses can also play a role. If a taxpayer incurs capital losses, they can offset their capital gains, thereby potentially reducing their total income and hence their AMT liability. Capital gains not only impact the tax calculations through the standard Form 1040 but also enter into more complex computations like the Qualified Dividends and Capital Gain Tax Worksheet and the Foreign Earned Income Tax Worksheet. These worksheets ensure the proper computation of tax where specific types of income, such as qualified dividends or foreign-earned income, are involved. With capital gains factored into these computations, it can impact the overall tax liability, including the potential for AMT. One strategic way to potentially minimize AMT liability is through the timing of capital gains and losses. Since capital gains can increase the likelihood of AMT, it may be advantageous to avoid realizing significant capital gains in years when you are already close to the AMT zone. Conversely, realizing capital losses in such years might be beneficial because it can reduce your total income and potentially your AMT exposure. Another strategy involves the use of tax-deferred retirement accounts like a 401(k) or an IRA. Since the income in these accounts grows tax-deferred, capital gains realized within the account do not contribute to the current year's income, thus not affecting the AMT computation. Lastly, taxpayers who pay AMT in one year may be eligible for a credit in a subsequent year under certain circumstances. If a taxpayer pays AMT due to "deferral" preference items, like exercising incentive stock options, they may be able to claim the AMT credit in a later year. This process can reduce future tax liability. Given the complexity of the AMT rules and their interaction with capital gains, personalized advice from a tax professional can be extremely beneficial. Each taxpayer's situation is unique, and what works best for one person might not work for another. A tax professional can analyze your specific circumstances and provide tailored strategies to minimize your tax liability. Tax planning involves making strategic decisions to minimize tax liability, and understanding the interplay between capital gains and AMT is a key part of this process. With proper planning, a taxpayer can time the realization of capital gains and losses, utilize tax-advantaged accounts effectively, and take advantage of any available AMT credits. In this way, a knowledgeable tax professional can help taxpayers navigate the complexities of capital gains and AMT. Understanding the complex relationship between capital gains and the Alternative Minimum Tax is crucial for effective tax planning. Both long-term and short-term capital gains can increase a taxpayer's overall income, potentially pushing them into the AMT zone. Unique AMT rules, exemptions, and adjustments related to capital gains further complicate the tax landscape. However, strategies like timing capital gains and losses, utilizing tax-deferred retirement accounts and considering AMT credits can potentially minimize AMT liability. Despite these strategies, the complexity of AMT rules necessitates the assistance of a tax professional for personalized advice and effective planning. Their expertise can provide tailored solutions to navigate the intricacies of capital gains and AMT, underscoring the value of strategic tax planning in managing one's overall tax liability.Direct Influence of Capital Gains on Alternative Minimum Tax (AMT)

Capital Gains in AMT Computation

Illustrating Capital Gains Affecting AMT

Unique Rules and Exemptions Related to Capital Gains and AMT

Understanding AMT Adjustments That Relate to Capital Gains

Rules and Exemptions in Practice

Strategies to Minimize AMT Liability Due to Capital Gains

Timing of Capital Gains and Losses

Use of Tax-Deferred Retirement Accounts

Consideration of AMT Credits

Role of a Tax Professional in Capital Gains and AMT Planning

Need for Personalized Advice

Benefits of Tax Planning

Bottom Line

How Capital Gains Affect AMT FAQs

Capital gains can indirectly influence AMT liability. Both long-term and short-term capital gains increase the taxpayer's total income. If this income exceeds the AMT exemption amount, the taxpayer may become liable for AMT. Although capital gains are taxed at the same rate under both the regular tax system and AMT, they can impact the taxpayer's overall tax liability under AMT.

Yes, capital losses can affect your AMT liability. If you incur capital losses, they can offset your capital gains, potentially reducing your total income and, thus, your AMT exposure.

Timing the realization of capital gains and losses can strategically minimize AMT liability. Avoiding large capital gains in years when you're close to the AMT zone may be beneficial. Conversely, realizing capital losses in such years can reduce your total income, thus potentially decreasing your AMT exposure.

Yes, using tax-deferred retirement accounts like a 401(k) or an IRA can help. Since the income in these accounts grows tax-deferred, capital gains realized within the account do not contribute to your current year's income and hence do not affect the AMT computation.

Given the complexity of the AMT rules and their interaction with capital gains, a tax professional can provide personalized advice, analyze your specific circumstances, and provide tailored strategies to minimize your tax liability. They can guide you in timing the realization of capital gains and losses, using tax-advantaged accounts effectively, and taking advantage of any available AMT credits.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.