1031 Exchange for Dummies is a simplified guide aimed at helping beginners understand the complexities of a 1031 exchange in real estate. A 1031 exchange, named after Section 1031 of the U.S. Internal Revenue Code, is an investment strategy that allows an investor to defer capital gains tax when selling an investment property, provided they reinvest the proceeds into a "like-kind" property. The purpose of a 1031 exchange is to encourage active reinvestment in the real estate market and to enable investors to leverage their capital more effectively by postponing tax liability. The 1031 exchange for dummies guide breaks down the involved processes, requirements, deadlines, and potential risks of such transactions, enabling investors to make more informed decisions and potentially enhance their long-term investment success. In order to qualify for a 1031 exchange, both the property sold and the property being acquired must be used for investment or business purposes. Properties held primarily for sale, personal residences, or vacation homes typically do not qualify. There are two key time constraints in a 1031 exchange. The investor has 45 days from the date of sale of the relinquished property to identify potential replacement properties. Following this, the investor has a total of 180 days from the sale of the relinquished property to close on the new property. In a 1031 exchange, a qualified intermediary (QI) plays a crucial role by holding the proceeds from the sale of the relinquished property and then using those funds to acquire the replacement property. The QI ensures the exchange process follows IRS guidelines, and the investor does not take constructive receipt of the funds, which could invalidate the exchange. To fully defer all taxes, the total purchase price of the replacement property must be equal to or greater than the total sale price of the relinquished property. Additionally, all the equity received from the sale must be used to acquire the replacement property. "Boot" is the term for any cash or relief from debt received in an exchange. If a property is sold and replaced with property of lesser value, the investor will receive boot and may have to pay capital gains tax on this amount. To avoid receiving boot, the investor should always try to exchange for a property of equal or greater value and reinvest all proceeds from the sale. First, the relinquished property is sold, and the process of a 1031 exchange begins. The sale proceeds go to the QI, which holds the funds until the replacement property is purchased. Within 45 days of the sale of the relinquished property, the investor must identify potential replacement properties. This is often the most challenging aspect of a 1031 exchange due to the strict timing and rules around property identification. The QI holds the funds from the sale and will use them to purchase the replacement property. This avoids the risk of the investor receiving the funds directly, which would disqualify the 1031 exchange. Once the replacement property is identified, the QI uses the proceeds from the original property's sale to purchase the replacement property. The QI then transfers the deed to the new property to the investor, thus completing the 1031 exchange. The investor must report the 1031 exchange to the IRS on Form 8824 for the tax year in which the exchange occurred. It is important to keep accurate records of the transaction, including identification notices and settlement statements. Failing to meet either of the two-time limits (45-day identification period and 180-day exchange period) will result in a disallowed exchange. This means the sale will be subject to tax as a regular sale. A mismanaged 1031 exchange could lead to significant tax implications. For instance, if an investor receives the funds directly or the QI is not properly qualified, the entire exchange could be disqualified, leading to immediate tax liabilities. As mentioned, receiving a "boot" could lead to a taxable event. If the replacement property is of lesser value, the difference could be considered boot, making it subject to tax. Deferred Exchanges: This is the most common form of 1031 exchange. In a deferred exchange, the sale of the old property and the purchase of the new one do not happen simultaneously. Simultaneous Exchanges: The relinquished and replacement properties are swapped simultaneously. This is less common due to the logistical complexities of timing two transactions to occur concurrently. Improvement / Construction Exchanges: In this scenario, the proceeds from the sale of the relinquished property are used to improve or construct the replacement property. The improved property must still meet the same requirements as a traditional 1031 exchange. Reverse Exchanges: This is a more complex variant where the replacement property is purchased before selling the current property. An "Exchange Accommodation Titleholder" is used to hold the title of the replacement property until the original property is sold. • Understanding Capital Gains Tax: Capital gains tax is a tax on the profit made from the sale of an investment. In the context of a 1031 exchange, this tax can be deferred as long as the proceeds are reinvested in like-kind property. • Tax Deferment vs Tax Exclusion: It's important to note that a 1031 exchange is a tax deferral strategy, not a tax exclusion strategy. This means that while the tax on the gain is deferred, it will eventually need to be paid when the new property is sold unless another 1031 exchange is performed. • Impact of 1031 Exchange on Tax Return: The 1031 exchange must be reported on the taxpayer’s IRS Form 8824 and included with the taxpayer's tax return for that year. Detailed records of the exchange, such as closing statements and identification letters, should be kept for tax purposes. In essence, a 1031 exchange is a powerful tool in real estate investing that allows deferral of capital gains tax when selling a property, provided a like-kind property is procured using the profits. This strategy motivates continual reinvestment in the real estate sector and optimizes investors' capital use by delaying tax obligations. The guidelines are stringent, necessitating awareness of the rules, deadlines, and potential risks associated with such transactions. A Qualified Intermediary plays an instrumental role in ensuring IRS compliance. Various forms of 1031 exchanges exist, each tailored to specific scenarios. Tax implications are pivotal, distinguishing deferral from exclusion and necessitating accurate record-keeping for IRS reporting. Ultimately, while complex, understanding and properly utilizing 1031 exchanges can significantly amplify long-term investment outcomes.Overview of 1031 Exchange for Dummies

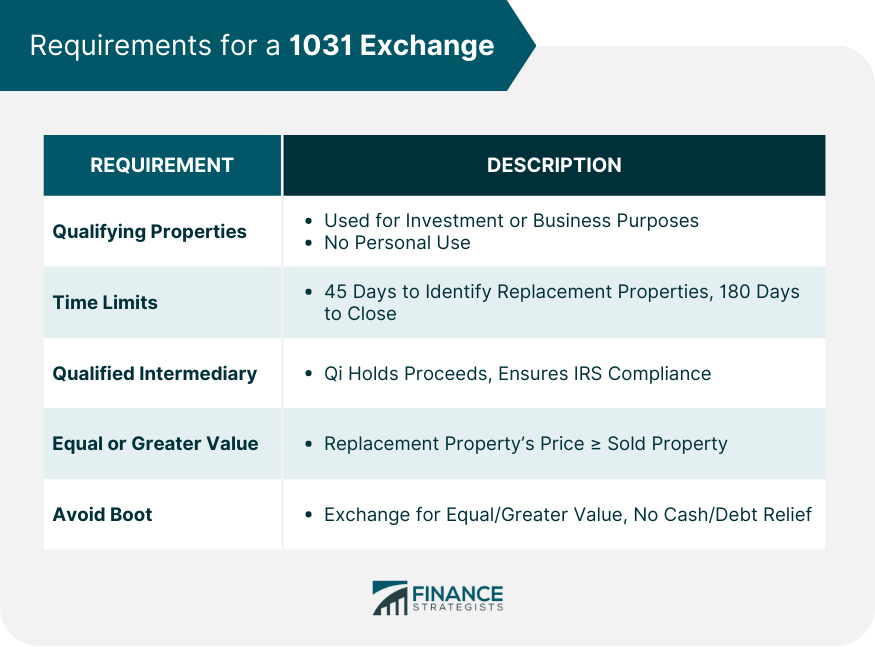

Requirements for a 1031 Exchange

Qualifying Properties for 1031 Exchange

Time Limits in 1031 Exchange

Role of a Qualified Intermediary

Equal or Greater Value Rule

Understand Boot and How to Avoid It

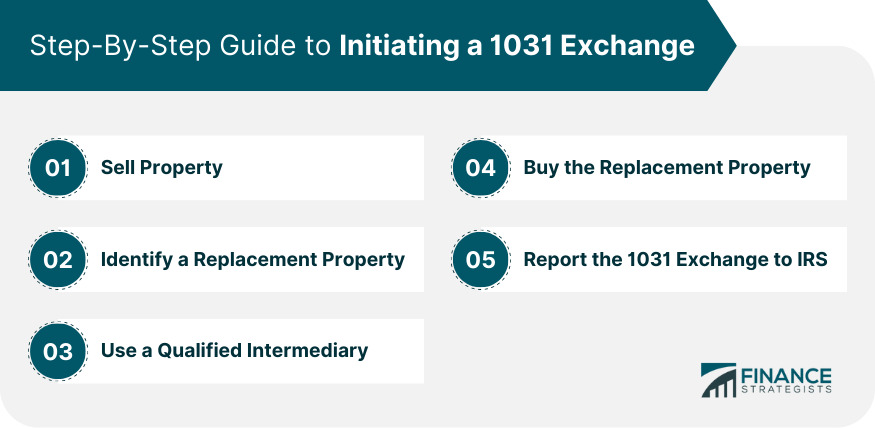

Step-By-Step Guide to Initiating a 1031 Exchange

Sell Property

Identify a Replacement Property

Use a Qualified Intermediary

Buy the Replacement Property

Report the 1031 Exchange to IRS

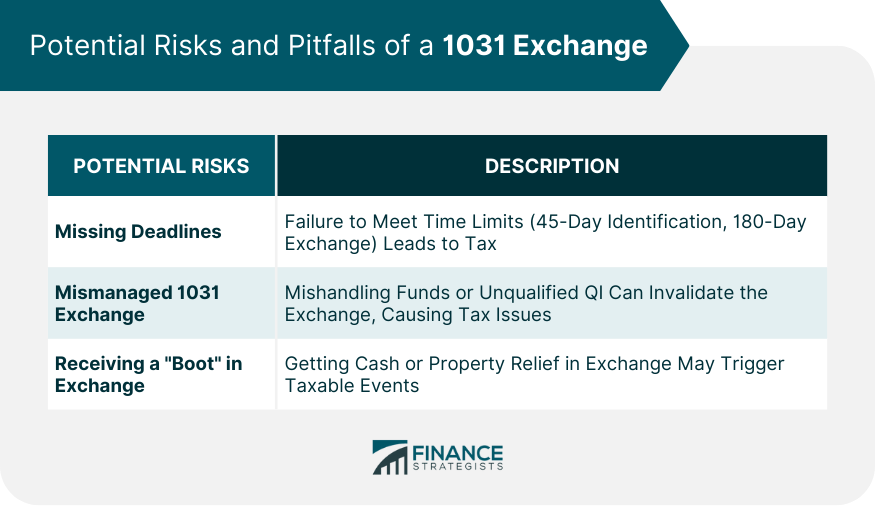

Potential Risks and Pitfalls of a 1031 Exchange

Risks Associated With Missing 1031 Exchange Deadlines

Potential Tax Implications of Mismanaging a 1031 Exchange

Impact of Receiving a "Boot" in an Exchange

1031 Exchange Variations

How 1031 Exchange Affects Taxes

Conclusion

1031 Exchange for Dummies FAQs

A 1031 exchange is a strategy in real estate investing where an investor can defer paying capital gains taxes on an investment property when it is sold as long as another "like-kind property" is purchased with the profit gained by the sale of the first property. The term "like-kind" refers to properties being similar in nature or character, not their grade or quality.

The investor has 45 days from the date of the sale of the relinquished property to identify potential replacement properties and a total of 180 days from the sale of the relinquished property to close on the new property.

A Qualified Intermediary (QI) is an individual or company that agrees to facilitate the 1031 exchange by holding the funds from the sale of the relinquished property until the replacement property is purchased. They ensure that the investor doesn't receive the funds directly, which would disqualify the 1031 exchange according to IRS guidelines.

"Boot" is the term for any cash or relief from debt received in an exchange. If a property is sold and replaced with property of lesser value, the investor will receive boot and may have to pay capital gains tax on this amount. To avoid receiving boot, the investor should always try to exchange for a property of equal or greater value and reinvest all proceeds from the sale.

Variations of 1031 exchanges include deferred exchanges (most common), simultaneous exchanges, improvement/construction exchanges, and reverse exchanges. Each variation suits different situations and has its own requirements and guidelines, according to the IRS.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.