1031 Exchanges in Syndication refers to a strategy utilized within real estate investment, combining the benefits of a 1031 exchange—a tax deferment tool—and real estate syndication—a method of pooling multiple investors' funds. In a 1031 exchange, investors can defer capital gains tax by reinvesting proceeds from a sold property into another "like-kind" property. When used in syndication, this strategy allows a group of investors to collectively reinvest gains from one property into another, potentially escalating their returns and investment portfolio's growth. The purpose of this approach is to leverage the power of collective investment while maximizing tax efficiency, thereby enhancing the profitability of the syndicate's real estate transactions. This method is particularly useful for expanding and diversifying a syndicate's real estate portfolio, enabling more flexible and strategic investment choices. 1031 exchanges, in essence, allow real estate investors to defer capital gains tax by reinvesting proceeds from a sold property into another “like-kind” property. When incorporated within real estate syndication—a method where multiple investors pool funds to invest in properties they may not afford individually—the process becomes even more dynamic. Syndicators can use 1031 exchanges to roll over gains from one syndicated property to another, offering increased flexibility and potential returns for the syndicate's investors. Syndications engaging in 1031 exchanges must adhere to strict IRS guidelines. The core requirement is that the exchanged properties are of "like-kind." This doesn't necessarily mean they are identical, but they must be of the same nature or character. In the context of syndication, an additional layer of complexity arises as the exchange must ensure proportional ownership interests for the syndicate's investors. Failure to comply can lead to hefty penalties and potential disqualification from tax deferral benefits. TIC allows individual investors in syndication to own a fractional deed in a property. It provides direct ownership, and each investor can use their share for a 1031 exchange independently. However, this structure requires unanimous decision-making, potentially slowing down syndication operations. In a DST, the property is held in a trust, and syndicate investors own beneficial interests in this trust. DSTs allow for more streamlined decision-making than TICs, offering syndications faster and more flexible operations. After the sale of an initial property, syndications have a 45-day window to identify potential replacement properties. It's a time-sensitive phase requiring swift yet careful decision-making to ensure the best choices for the syndicate. The entire exchange, from the sale of the relinquished property to the acquisition of the replacement property, must be completed within 180 days. Syndications must manage this timeline meticulously, accounting for potential delays in financing or closing. A Qualified Intermediary (QI) is pivotal in 1031 exchanges, acting as a neutral third party to handle funds and ensure the process adheres to IRS guidelines. For syndications, the QI's role is amplified due to the complexities of managing multiple investor interests. As emphasized earlier, properties in the exchange must be of "like-kind." For syndications, this can translate to exchanging an office building for another commercial property or a multi-family residential property for another similar asset. "Boot" refers to any additional value received in the exchange that isn't considered "like-kind," such as cash or debt reduction. This is taxable and can offset some of the benefits of the 1031 exchange. Syndications must be cautious to minimize boot to maintain the tax efficiency of the transaction. Arguably the most prominent advantage, 1031 exchanges allow syndications to defer capital gains tax, thereby preserving more capital for reinvestment. By repeatedly rolling over gains from one property to another, a syndicate can effectively defer taxes until an ultimate sale, often years or decades down the line. Syndications, after a successful investment, often find themselves holding properties with significant accrued equity. Through a 1031 exchange, this equity can be reinvested in more valuable properties, possibly promising higher returns. Over time, a syndicate can use 1031 exchanges to diversify its portfolio. Rather than being tied to a single property type or market, syndicates can strategically exchange properties, branching into different markets or property types and spreading the risk. Syndications, while choosing replacement properties, may face unpredictable market shifts. A property that seems promising during the identification period may lose value by the time of acquisition. The tight deadlines of the 1031 exchange process leave little room for error. Syndications must navigate potential challenges like financing delays, investor disagreements, or unexpected property issues, all within the stipulated timeframes. If a syndication relinquishes a property with associated debt, the new property must also have equal or greater debt to avoid tax penalties. This can complicate property choices, especially in volatile debt markets. TICs, while offering direct ownership, necessitate unanimous decision-making. This can be challenging for syndications, leading to potential disputes, decision-making delays, or even dissolution threats. Choose the Right Syndicator: A syndicator's expertise is vital. Prospective investors should look for a syndicator with a proven track record in managing 1031 exchanges, ensuring the complexities are well-navigated. Understand the Market: Syndicates should constantly monitor real estate trends. Identifying rising markets or foreseeing potential downturns can inform smarter decisions during the exchange process. Proper Due Diligence: From ensuring properties are "like-kind" to managing tight timelines, syndications must be meticulous. Proper due diligence can be the difference between a successful tax-deferred exchange and a costly mistake. 1031 Exchanges in Syndication offer a potent tool for real estate investors, blending tax deferral advantages with the power of a collective investment. By adhering to strict IRS guidelines and managing complex timelines, syndicates can leverage accrued equity to purchase higher-value properties, diversify their real estate portfolios, and enhance overall profitability. However, the process isn't without challenges. Unpredictable market risks, debt replacement rules, and potential disagreements within Tenant-In-Common structures can pose substantial hurdles. As the landscape continues to evolve, influenced by changing tax laws and emerging technologies, successful navigation of these complexities will require a combination of syndicator expertise, diligent market understanding, and careful due diligence. Ultimately, while 1031 exchanges in syndication present an attractive opportunity, they also underscore the importance of informed, strategic decision-making within the realm of real estate investment.1031 Exchanges in Syndication Overview

How 1031 Exchanges Work in Real Estate Syndication

Legal and Tax Implications of 1031 Exchanges in Syndication

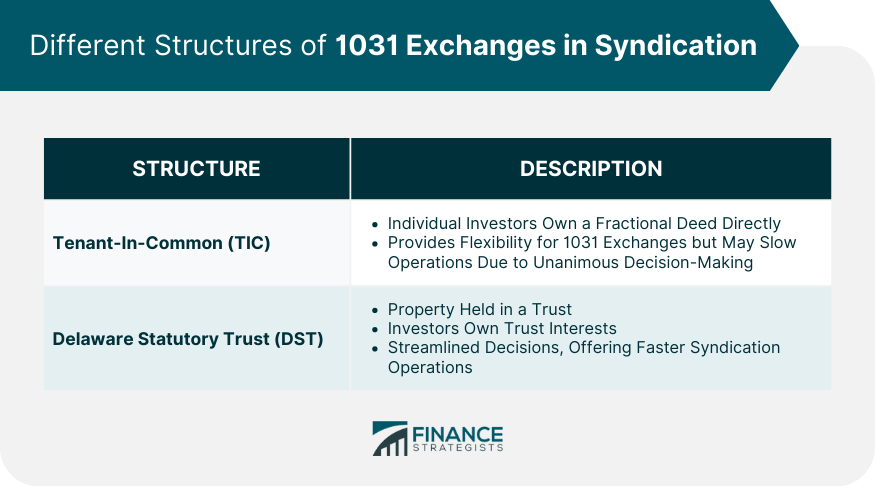

Different Structures of 1031 Exchanges in Syndication

Tenant-In-Common (TIC) Structure

Delaware Statutory Trust (DST) Structure

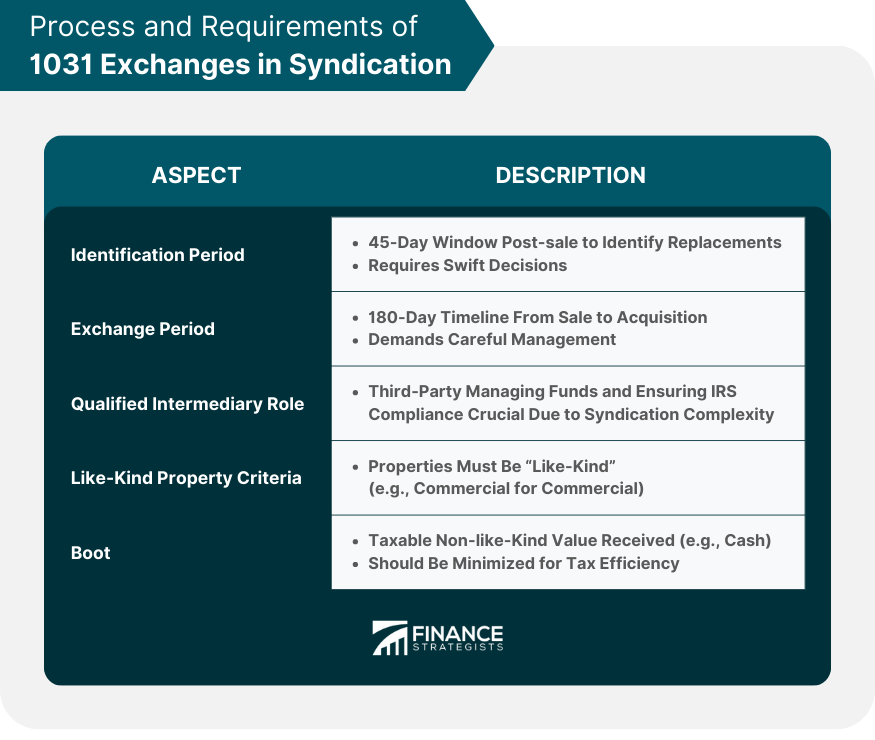

Process and Requirements of 1031 Exchanges in Syndication

Identification Period

Exchange Period

Qualified Intermediary Role

Like-Kind Property Criteria

Boot

Advantages of 1031 Exchanges in Syndication

Deferment of Capital Gains Tax

Leveraging Equity to Purchase Higher-Value Properties

Diversification of Real Estate Portfolio

Potential Risks and Challenges of 1031 Exchanges in Syndication

Market Risks

Timing Risks

Debt Replacement Rules

Risks Associated With Co-ownership in TIC Structure

Expert Tips for Successful 1031 Exchanges in Syndication

Conclusion

1031 Exchanges in Syndication FAQs

A 1031 exchange allows real estate investors to defer capital gains tax by reinvesting proceeds from a sold property into another “like-kind” property. Within real estate syndication, this process enables multiple investors who've pooled funds to roll over gains from one syndicated property to another, enhancing flexibility and potential returns.

TIC allows individual investors in syndication to own a direct, fractional deed in a property. Each investor can use their share for a 1031 exchange individually. DST, on the other hand, holds the property in a trust, with investors owning beneficial interests in this trust. DSTs typically allow for more streamlined decision-making compared to TICs.

A Qualified Intermediary (QI) acts as a neutral third party in the 1031 exchange process, handling funds and ensuring that the transaction complies with IRS guidelines. In the context of real estate syndication, the QI's role is especially crucial due to the complexities of managing multiple investor interests, making sure the exchange remains beneficial and compliant for all involved parties.

There are several risks, including market risks where property values can unexpectedly drop, timing risks due to strict deadlines of the exchange process, complications arising from debt replacement rules, and challenges related to unanimous decision-making in the TIC structure.

Changing tax laws can affect the feasibility or benefits of 1031 exchanges, requiring syndicates to adapt to maintain their advantages. Technological advancements, like blockchain, can revolutionize property transactions, potentially making 1031 exchanges more transparent and efficient for syndicates.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.