The 408(k) plan is a type of retirement savings plan available to small businesses with 100 or fewer employees, as well as self-employed individuals. It shares similarities with the more widely known 401(k) plan but has some distinct differences. The main difference lies in the eligibility requirements and target market. While 401(k) plans are available to larger businesses and have fewer restrictions on employee participation, 408(k) plans are specifically designed for smaller businesses. Additionally, 408(k) plans typically have more flexible contribution options, allowing employees to make adjustments to their contributions throughout the year. This makes it a suitable choice for businesses seeking to offer retirement benefits to their employees while accommodating varying financial circumstances. 408(k) plan is available to small businesses with 100 or fewer employees, as well as self-employed individuals. To be eligible, an employee must be at least 21 years old and have completed one year of service with the employer. Employers can also choose to set less restrictive eligibility requirements if they wish. Employees can make contributions to their 408(k) accounts through payroll deductions. The amount contributed can be a fixed dollar amount or a percentage of their salary. Employees can also adjust their contributions throughout the year, allowing for greater flexibility in their retirement savings strategy. Employers have the option to make contributions to their employees' 408(k) accounts. These contributions can be in the form of a matching contribution, where the employer matches a percentage of the employee's contribution, or a discretionary contribution, where the employer contributes a fixed amount regardless of employee contributions. The Internal Revenue Service (IRS) sets annual contribution limits for the 408(k) plan. For 2026, the maximum employee contribution is $24,500 ($23,500 for 2025), with an additional catch-up contribution of $8,000 ($7,500 for 2025) allowed for those aged 50 or older. Employer contributions are also subject to limits, with the combined total of employee and employer contributions not exceeding 100% of the employee's compensation or $72,000 ($70,000 for 2025), whichever is lower. Vesting refers to the percentage of employer contributions that employees are entitled to keep when they leave the company. 408(k) plan can have immediate vesting, meaning employees have full ownership of employer contributions as soon as they are made, or they can have a vesting schedule. The most common vesting schedule is a three-year cliff, where employees become 100% vested after three years of service. One of the main benefits of a 408(k) plan is the tax-deferred growth of investments. This means that earnings on investments within the plan are not subject to taxes until they are withdrawn, allowing for a potentially larger retirement nest egg. Employee contributions to a 408(k) plan are made on a pre-tax basis, reducing the employee's taxable income for the year. This can result in significant tax savings for employees, especially those in higher tax brackets. Employers can also benefit from tax deductions on their contributions to employees' 408(k) accounts. These contributions are considered business expenses and can be deducted from the employer's taxable income, reducing their overall tax liability. Employees who leave their job or retire can roll over their 408(k) account balance to another qualified retirement plan, such as an Individual Retirement Account (IRA) or another employer's plan, without incurring any taxes or penalties. This allows for continued tax-deferred growth of their retirement savings. Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. They offer a way for employees to access professionally managed, diversified investment options within their 408(k) plan. ETFs are similar to mutual funds in that they offer diversified investment portfolios. However, they trade like individual stocks on an exchange, allowing for more flexibility in buying and selling throughout the trading day. ETFs can be a cost-effective and tax-efficient investment option within a 408(k) plan. Some 408(k) plan may also allow employees to invest in individual stocks and bonds. This option provides greater control over the investment strategy but requires more knowledge and involvement in managing the portfolio. Active management involves a portfolio manager making investment decisions based on research and analysis of the market, with the goal of outperforming a specific benchmark index. While actively managed funds can potentially deliver higher returns, they often come with higher fees and greater risk. Passive management, or index investing, involves investing in a fund that tracks a specific market index, such as the S&P 500. These funds typically have lower fees and offer broad market exposure, making them a popular choice for retirement savings plans like the 408(k). When choosing investment options within a 408(k) plan, it is important for employees to consider their risk tolerance and investment horizon. Younger investors with a long time until retirement may be able to take on more risk, while those nearing retirement may want to focus on more conservative investments to preserve their savings. The plan administrator is responsible for managing the 408(k) plan, including ensuring compliance with regulations, maintaining accurate records, and providing required disclosures to employees. This role can be performed by the employer, an outside service provider, or a combination of both. 408(k) plan is subject to numerous regulations from the Department of Labor (DOL) and the IRS. These regulations govern areas such as plan eligibility, contribution limits, and reporting requirements. Failure to comply with these regulations can result in penalties and potential loss of the plan's tax-advantaged status. Plan administrators must maintain accurate records for each employee's 408(k) account, including contributions, earnings, and distributions. They are also responsible for filing annual reports with the IRS and providing employees with statements detailing their account activity. In some cases, the 408(k) plan may be subject to an audit by the DOL or the IRS. The purpose of these audits is to ensure compliance with regulations and to protect the interests of plan participants. Employers should work closely with their plan administrator to ensure all necessary documentation is in place in case of an audit. Withdrawals from a 408(k) plan before the age of 59 ½ are generally subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income. There are some exceptions to this rule, such as for qualified higher education expenses or the purchase of a first home. Starting at age 73, plan participants must begin taking required minimum distributions (RMDs) from their 408(k) accounts. The RMD amount is calculated based on the account balance and the participant's life expectancy, as determined by IRS tables. In certain cases, employees may be eligible for a hardship withdrawal from their 408(k) account to cover immediate and heavy financial needs. These withdrawals are still subject to taxes and may also incur a 10% early withdrawal penalty. Some 408(k) plan may allow employees to take loans from their account balance. These loans must be repaid within five years, with interest, and are subject to certain restrictions. While loans can provide employees with access to their retirement savings in times of need, they can also reduce the long-term growth potential of the account. When leaving a job or retiring, employees can choose to roll over their 408(k) account balance to an Individual Retirement Account. This rollover allows for continued tax-deferred growth of retirement savings and provides greater flexibility in investment options. Employees can also choose to roll over their 408(k) balance to a new employer's retirement plan, such as a 401(k) or another 408(k) plan. This option allows for continued tax-deferred growth and may provide access to additional employer-sponsored benefits. Direct transfers, also known as trustee-to-trustee transfers, involve moving the 408(k) account balance directly from the current plan administrator to the new plan or IRA without the employee ever taking possession of the funds. This method ensures that the rollover is tax-free and avoids potential penalties. Indirect transfers involve the employee receiving a distribution from their 408(k) account and then depositing the funds into a new retirement plan or IRA within 60 days. However, this method can be subject to taxes and penalties if the funds are not deposited within the required timeframe. When conducted properly, rollovers and transfers of 408(k) plan assets are generally tax-free. However, failure to complete the rollover or transfer within the required timeframe or not following the proper procedures can result in taxes and penalties. There are several reasons an employer may choose to terminate a 408(k) plan, such as business closure, financial hardship, or a change in the company's retirement benefit offerings. When a 408(k) plan is terminated, employees will typically receive their account balance as a lump-sum distribution or as an annuity, depending on the plan provisions. These distributions are subject to taxes and may also be subject to penalties if taken before age 59 ½. The tax implications of a 408(k) plan termination will depend on the circumstances and the method of distribution chosen by the employer and employee. It is essential for employees to consult with a tax advisor to understand the potential tax consequences and explore options for rollovers or transfers to minimize their tax liability. 401(k) plan is the most common employer-sponsored retirement plan and shares many features with the 408(k) plan. However, 401(k) plans are typically available to larger employers and may offer a more extensive range of investment options and plan features. 403(b) plan is similar to the 401(k) plan but is available to employees of public schools, non-profit organizations, and certain religious institutions. While the 403(b) plan also offers tax-deferred growth and employer contributions, they may have different investment options and plan provisions. SEP plans are another retirement savings option for small businesses and self-employed individuals. They allow employers to make tax-deductible contributions to employees' IRAs, providing flexibility in contribution amounts and a simplified administrative process. However, unlike the 408(k) plan, SEP plans do not allow for employee contributions. SIMPLE IRAs are designed for small businesses with 100 or fewer employees and offer a simpler alternative to the 408(k) plan. Both employees and employers can contribute to SIMPLE IRAs, but the contribution limits are generally lower than those for the 408(k) plan. Additionally, SIMPLE IRAs may have fewer investment options and plan features compared to the 408(k) plan. The 408(k) plan is a retirement savings option specifically designed for small businesses and self-employed individuals. It offers flexibility in employee contributions, allowing adjustments throughout the year. Employers have the option to make matching or discretionary contributions. The plan provides tax benefits, including tax-deferred growth, pre-tax employee contributions, and employer tax deductions. There are various investment options available, including mutual funds, ETFs, and individual stocks and bonds. Rollover options include transferring funds to an IRA or another employer's plan. However, early withdrawals and failure to meet distribution requirements may result in penalties and taxes. Compared with other retirement plans, the 408(k) plan caters to a specific market segment and offers unique features tailored to the needs of small businesses and self-employed individuals.Definition of 408(k) Plan

408(k) Plan Features

Eligibility for a 408(k) Plan

Contributions to a 408(k) Plan

Employee Contributions

Employer Contributions

Contribution Limits

Vesting Schedules

Tax Benefits of a 408(k) Plan

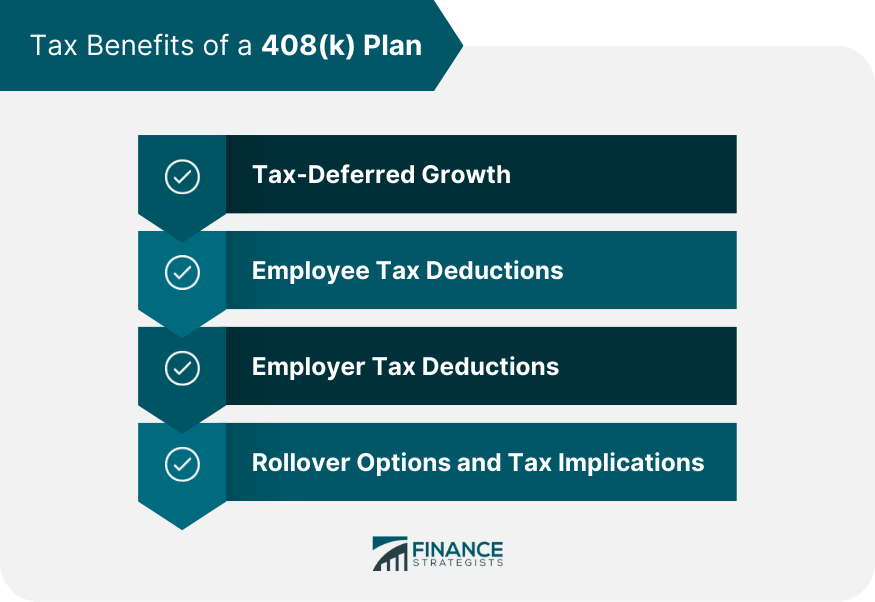

Tax-Deferred Growth

Employee Tax Deductions

Employer Tax Deductions

Rollover Options and Tax Implications

Investment Options in a 408(k) Plan

Types of Investments

Mutual Funds

Exchange-Traded Funds (ETFs)

Individual Stocks and Bonds

Investment Strategies

Active Management

Passive Management

Risk Tolerance and Investment Horizons

408(k) Plan Administration

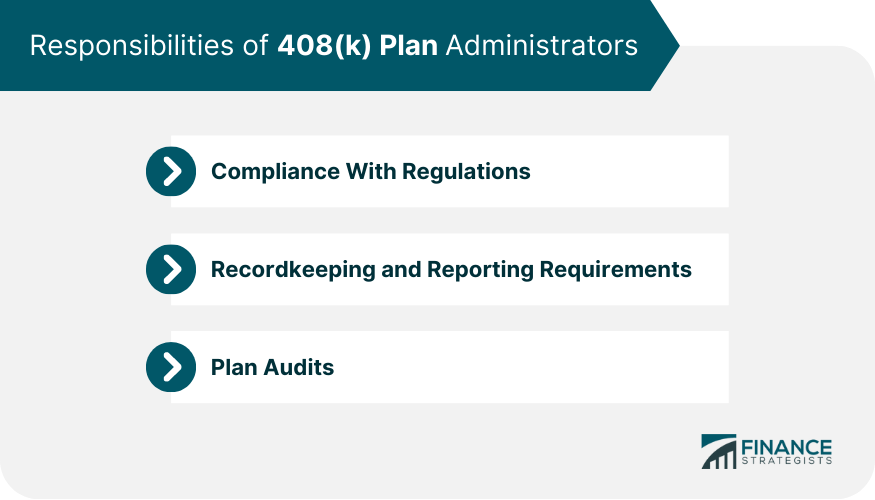

Responsibilities of Plan Administrators

Compliance With Regulations

Recordkeeping and Reporting Requirements

Plan Audits

408(k) Plan Distributions

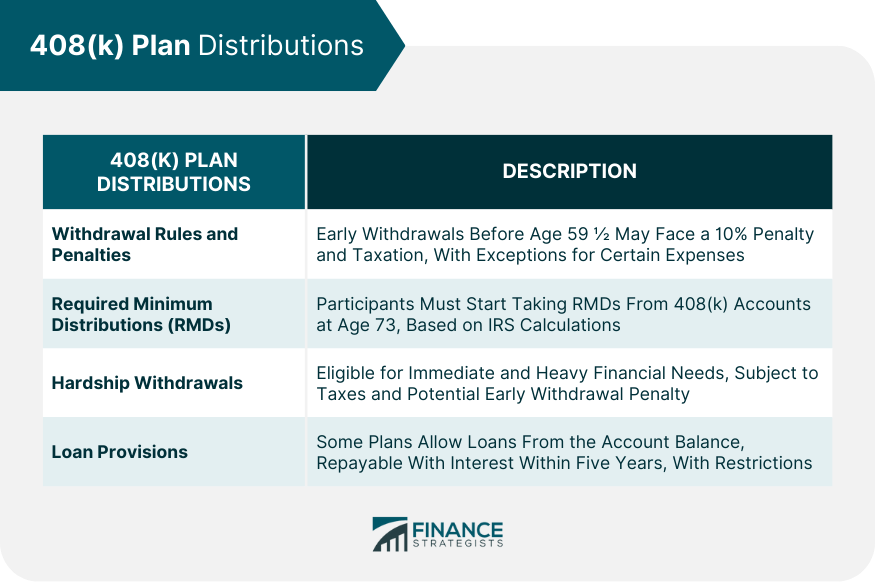

Withdrawal Rules and Penalties

Required Minimum Distributions (RMDs)

Hardship Withdrawals

Loan Provisions

408(k) Plan Rollovers and Transfers

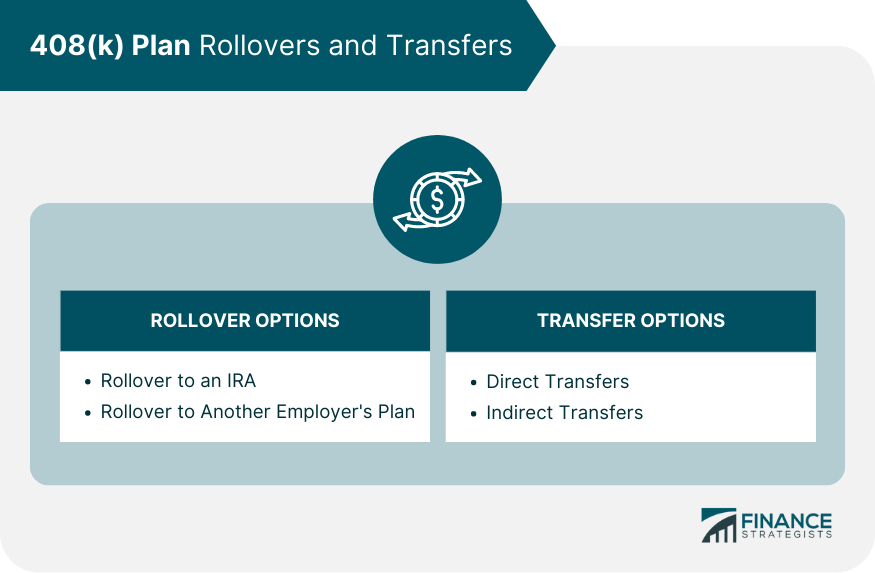

Rollover Options

Rollover to an IRA

Rollover to Another Employer's Plan

Transfer Options

Direct Transfers

Indirect Transfers

Tax Implications of Rollovers and Transfers

408(k) Plan Termination

Reasons for Plan Termination

Distribution of Assets Upon Plan Termination

Tax Implications of Plan Termination

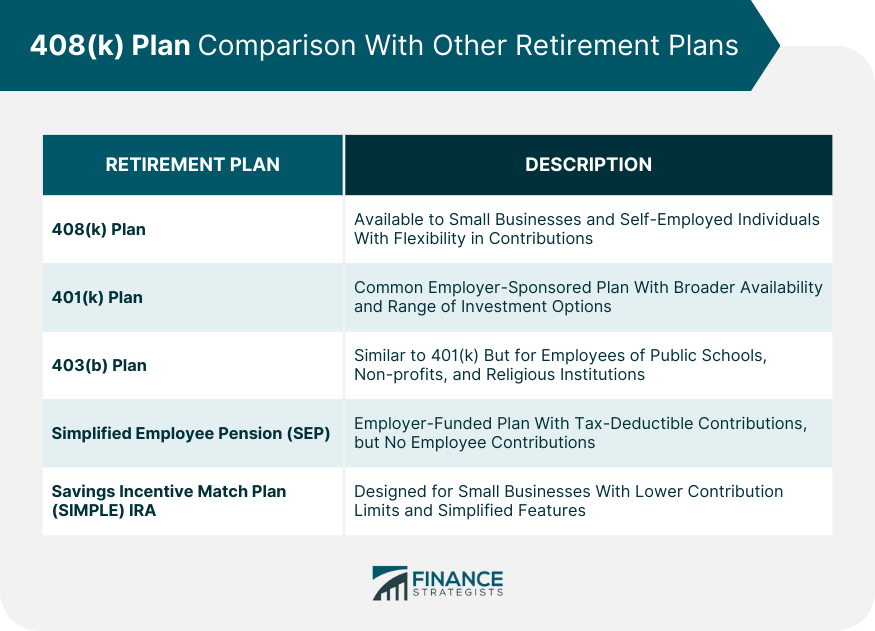

Comparing 408(k) Plan With Other Retirement Plans

401(k) Plan

403(b) Plan

Simplified Employee Pension (SEP) Plans

Savings Incentive Match Plan for Employees (SIMPLE) IRAs

Conclusion

408(k) Plan FAQs

A 408(k) Plan is a retirement savings plan designed for small businesses with 100 or fewer employees and self-employed individuals. To be eligible, an employee must be at least 21 years old and have completed one year of service with the employer. Employers can choose to set less restrictive eligibility requirements if they wish.

Employees can make pre-tax contributions to their 408(k) accounts through payroll deductions, while employers have the option to make matching or discretionary contributions. The IRS sets annual contribution limits for both employee and employer contributions to a 408(k) Plan.

A 408(k) Plan offers tax-deferred growth on investments, allowing for potentially larger retirement savings. Employee contributions are made on a pre-tax basis, reducing their taxable income, while employer contributions are tax-deductible as a business expense.

A 408(k) Plan offers a variety of investment options, including mutual funds, exchange-traded funds (ETFs), and individual stocks and bonds. Employees can choose between active and passive investment strategies based on their risk tolerance and investment horizon.

Yes, you can roll over your 408(k) Plan balance to another qualified retirement plan, such as an Individual Retirement Account (IRA) or another employer's plan, without incurring any taxes or penalties. Rollovers can be done through direct transfers (trustee-to-trustee) or indirect transfers, with the latter subject to specific time constraints and potential tax implications.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.