Small business retirement plans are financial savings and investment programs specifically designed to help employees and owners of small businesses prepare for their retirement. These plans offer tax advantages, encourage long-term savings, and promote financial security for the future. Common types of small business retirement plans include Simplified Employee Pension (SEP) IRAs, Savings Incentive Match Plan for Employees (SIMPLE) IRAs, and 401(k) plans tailored for small businesses. Each plan has unique features, contribution limits, and eligibility requirements to accommodate the diverse needs of small business owners and their employees. A SEP IRA is an individual retirement account designed for small businesses and self-employed individuals. It allows employers to make tax-deductible contributions to their employees' retirement accounts. SEP IRAs are easy to set up and have low administrative costs. However, the employer is responsible for all contributions, which may not be ideal for businesses with tight budgets. To be eligible for a SEP IRA, the business must have fewer than 100 employees, and the employer must make contributions on behalf of all eligible employees. A SIMPLE IRA is a retirement plan designed for small businesses with 100 or fewer employees. It allows both employers and employees to make tax-deductible contributions. SIMPLE IRAs offer higher contribution limits than traditional IRAs and are easy to set up. However, employers are required to match employee contributions, which can be costly. To establish a SIMPLE IRA, the business must have 100 or fewer employees and cannot maintain any other retirement plans. A traditional 401(k) is a retirement plan that allows employees to contribute pre-tax dollars, with employers having the option to match contributions. Traditional 401(k) plans offer higher contribution limits than IRAs and provide flexibility for employers in terms of matching contributions. However, they come with higher administrative costs and responsibilities. There are no specific eligibility requirements for businesses to establish a traditional 401(k) plan. A Safe Harbor 401(k) is similar to a traditional 401(k), but it requires employers to make mandatory contributions to employees' accounts to avoid annual nondiscrimination testing. Safe Harbor 401(k) plans simplify administration by eliminating certain tests but require employers to make mandatory contributions. Any business can establish a Safe Harbor 401(k) plan, but it must meet specific contribution requirements. A Solo 401(k) is a retirement plan designed for self-employed individuals and business owners with no employees other than their spouses. Solo 401(k) plans offer high contribution limits and flexibility in terms of contributions. However, they are limited to businesses without employees. To establish a Solo 401(k), the business owner must have no employees other than their spouse. A profit-sharing plan is a type of defined contribution plan where employers make discretionary contributions to employees' retirement accounts based on the company's profits. Profit-sharing plans can help motivate employees and align their interests with the company's success. However, they may not be suitable for businesses with unpredictable profits. There are no specific eligibility requirements for businesses to establish a profit-sharing plan. A defined benefit plan is a traditional pension plan that promises employees a specific monthly benefit upon retirement, based on factors like salary and years of service. Defined benefit plans can provide employees with a stable and predictable source of retirement income. However, they come with higher administrative costs and funding requirements, making them less attractive for small businesses. There are no specific eligibility requirements for businesses to establish a defined benefit plan. However, these plans are more common among larger companies due to their complexity and cost. The size of your business can influence the type of retirement plan that best suits your needs. For example, smaller businesses may prefer SEP or SIMPLE IRAs, while larger companies might consider traditional 401(k) plans. Understanding the needs and preferences of your employees can help you choose the right retirement plan. For instance, younger employees may prefer plans with higher contribution limits and flexibility, while older employees might prioritize stability. Consider the costs associated with setting up and administering the retirement plan, such as fees, contribution requirements, and potential tax implications. Some retirement plans require more administrative effort than others. Ensure you have the resources to manage the chosen plan effectively. Different retirement plans offer various tax advantages for both employers and employees. Consult with a tax professional to understand the tax implications of each plan. Consider how the retirement plan will adapt as your business grows and evolves. Choose a plan that can accommodate changes in your workforce or financial situation. Research and compare various plan providers to find one that offers the right services, fees, and investment options for your business. Work with the chosen provider to set up the retirement plan, ensuring it meets legal and regulatory requirements. Educate employees about the benefits and features of the retirement plan, as well as their responsibilities and contribution options. Regularly review the performance of the retirement plan and make adjustments as necessary to ensure it continues to meet the needs of your business and employees. Small business retirement plans are crucial for both employers and employees, providing long-term financial security and contributing to a loyal workforce. Small businesses have a range of retirement plan options to choose from, including SEP IRAs, SIMPLE IRAs, 401(k) plans, profit-sharing plans, and defined benefit plans. When selecting a plan, it's essential to consider factors such as business size, employee demographics, cost considerations, administrative responsibilities, tax implications, and flexibility for future growth. Effective implementation of the chosen plan involves selecting a suitable plan provider, establishing the plan, communicating it to employees, and regularly monitoring and maintaining it. Overall, choosing the right retirement plan can help small businesses and their employees achieve their long-term financial goals.Definition of Small Business Retirement Plans

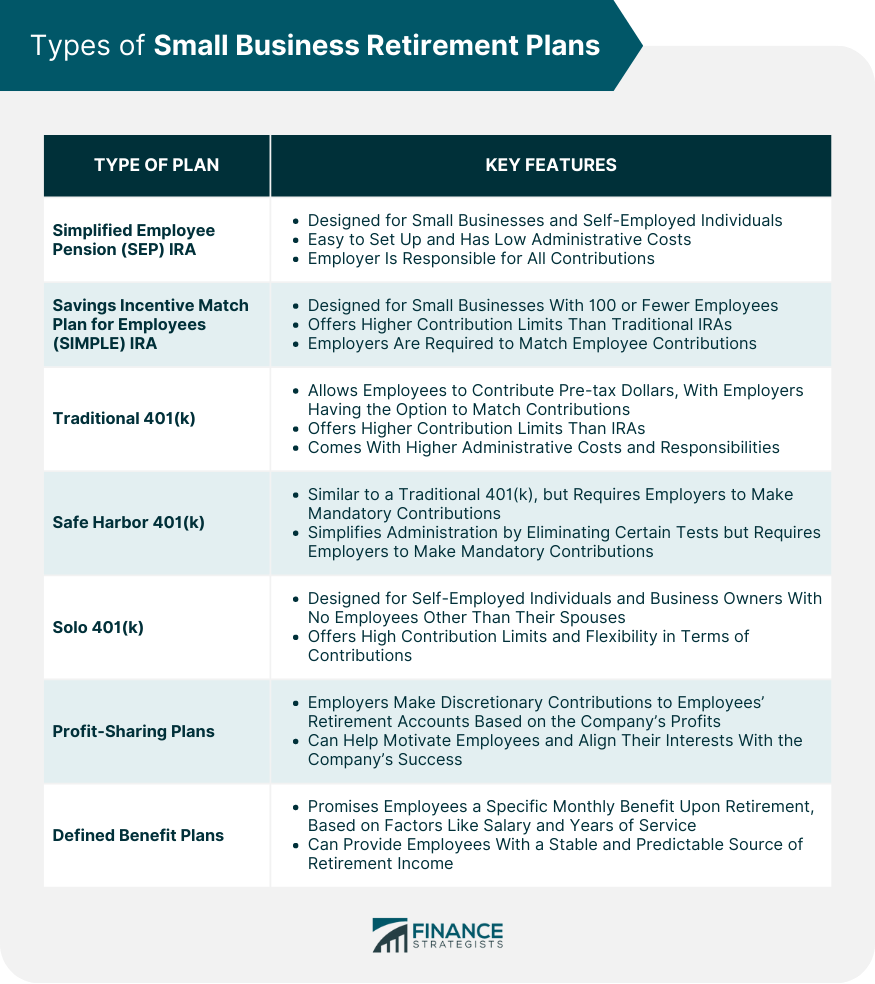

Types of Small Business Retirement Plans

Simplified Employee Pension (SEP) IRA

Savings Incentive Match Plan for Employees (SIMPLE) IRA

401(k) Plans

Traditional 401(k)

Safe Harbor 401(k)

Solo 401(k)

Profit-Sharing Plans

Defined Benefit Plans

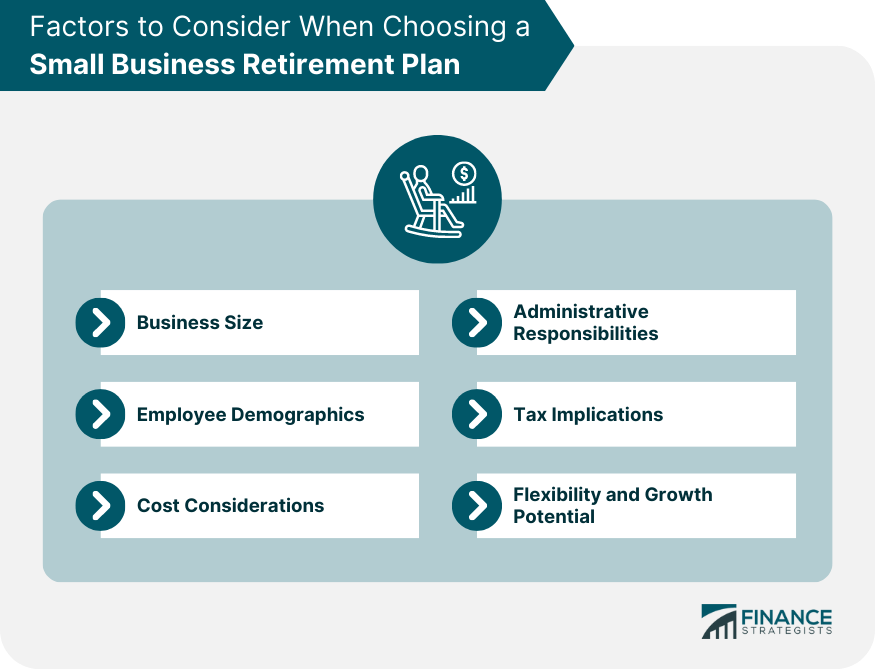

Factors to Consider When Choosing a Small Business Retirement Plan

Business Size

Employee Demographics

Cost Considerations

Administrative Responsibilities

Tax Implications

Flexibility and Growth Potential

Implementing a Retirement Plan for Small Business

Selecting a Plan Provider

Establishing the Plan

Communicating the Plan to Employees

Monitoring and Maintaining the Plan

Bottom Line

Small Business Retirement Plans FAQs

Some common small business retirement plans include Simplified Employee Pension (SEP) IRAs, Savings Incentive Match Plan for Employees (SIMPLE) IRAs, 401(k) plans (Traditional, Safe Harbor, and Solo), profit-sharing plans, and defined benefit plans.

Small business retirement plans provide financial security for employees in their retirement years while offering tax advantages for both employers and employees. Additionally, offering a retirement plan can help attract and retain top talent, contributing to a more stable and loyal workforce.

When choosing a small business retirement plan, consider factors such as business size, employee demographics, cost considerations, administrative responsibilities, tax implications, and flexibility for future growth.

To implement a small business retirement plan effectively, start by selecting a suitable plan provider, establishing the plan according to legal and regulatory requirements, communicating the plan to employees, and monitoring and maintaining the plan regularly to ensure it meets the needs of your business and employees.

Eligibility requirements for small business retirement plans vary depending on the plan type. For example, SEP and SIMPLE IRAs require businesses to have fewer than 100 employees, while Solo 401(k) plans are limited to self-employed individuals and business owners with no employees other than their spouses.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.