A 457 plan is a type of non-qualified, tax-advantaged deferred compensation retirement plan available to certain state and local public employees and employees of some tax-exempt organizations. These plans allow participants to save money for retirement by deferring a portion of their salary and contributing it to the plan. The money in a 457 plan grows tax-deferred until it is withdrawn, typically after retirement. The creation of 457 plans dates back to 1978 when the Revenue Act was passed. It was initially designed for state and local government employees, but the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) expanded the eligibility to include certain non-governmental, non-profit organizations. The intention was to provide these groups with similar retirement savings opportunities that private sector employees have with 401(k) plans. The two primary entities offering 457 plans are government organizations and non-profit organizations. These include state, county, and municipal governments, public school systems, water and utility districts, and non-profit hospitals, charities, and unions. In the governmental sector and some non-profit organizations, employees are eligible to participate in 457(b) plans. Unlike other retirement plans, there are no income restrictions for participation in a 457(b) plan. As of 2026, the maximum contribution to a 457(b) plan is $24,500 ($23,500 for 2025) per year, with a catch-up contribution of an additional $8,000 allowed for those aged 50 and above. These limits are subject to annual adjustments for inflation. One of the significant benefits of the 457(b) plan is the absence of a 10% penalty for withdrawing funds before the age of 59½, unlike 401(k) and 403(b) plans. This makes it a flexible option for those considering early retirement. However, a potential drawback is the limited investment options compared to what might be available in a 401(k) or an IRA. The 457(f) plans are available for select groups of highly compensated employees and executives within non-governmental, tax-exempt organizations. Unlike 457(b) plans, these are typically not available to all employees. There are no specified IRS contribution limits for 457(f) plans, making them attractive for high earners. However, these plans are subject to a "risk of forfeiture," meaning the employee risks losing the deferred compensation if certain conditions aren't met. A significant benefit of 457(f) plans is the lack of contribution limits, potentially allowing for substantial tax-deferred earnings. However, the risk of forfeiture can be a significant drawback, tying the employee's deferred compensation to continued service with the organization or specific performance goals. Both 457 and 401(k) plans are types of tax-advantaged retirement plans that allow for pre-tax contributions. However, there are key differences. Most notably, 457 plans don't incur a 10% penalty for withdrawals made before age 59½, unlike 401(k) plans. Additionally, 457 plans often have fewer investment options than 401(k) plans. Like 457 plans, 403(b) plans are designed for public sector and non-profit employees. A significant difference is that early withdrawals before age 59½ from a 403(b) plan can incur a 10% penalty, whereas 457 plans do not have this penalty. However, 403(b) plans can offer a broader range of investment options compared to some 457 plans. Traditional and Roth IRAs are personal retirement accounts, not employer-sponsored. The main difference is the tax treatment: Traditional IRA contributions are tax-deductible, while Roth IRA contributions are made with post-tax dollars. In contrast, all contributions to a 457 plan are pre-tax. Additionally, 457 plans typically allow for higher annual contributions compared to IRAs. One of the primary benefits of a 457 plan is that contributions are made pre-tax, which lowers your taxable income for the year. This can be a substantial advantage for those in higher tax brackets. Another major benefit of 457 plans is the lack of a 10% early withdrawal penalty. This is a unique feature among most retirement plans and provides additional flexibility, especially for those considering early retirement. For those nearing retirement, the 457 plan allows for catch-up contributions, which can significantly increase the amount of money you're able to set aside for retirement. One potential drawback of 457 plans is that they often have more limited investment options compared to 401(k) plans or IRAs. This can restrict your ability to diversify your investments within the plan. In non-governmental 457 plans, the deferred compensation remains the property of the employer until the employee receives the distribution. This means that in the event of the employer's bankruptcy, the funds could be subject to the employer's creditors. In 457(f) plans, the 'risk of forfeiture' clause may result in a loss of deferred compensation if the employee doesn't meet certain requirements, such as staying with the employer for a specified period. The Internal Revenue Service (IRS) provides guidelines for contribution limits, catch-up contributions, and withdrawals for 457 plans. It's crucial to understand these rules to avoid any tax penalties or unforeseen tax liabilities. Each employer can set specific rules and restrictions for their 457 plan, including eligibility, matching contributions, and investment options. Employees should thoroughly understand these details before participating in the plan. 457 plans can be rolled over into other retirement plans, like a 401(k) or an IRA, or into another 457 plan. However, the rollover rules can be complex, and it's important to understand them to avoid any unintended tax consequences. Contributions to a 457 plan are tax-deferred, meaning you don't pay taxes on the money until you withdraw it in retirement. This can be a significant benefit, especially if you're in a lower tax bracket in retirement than when you were working. While 457 plans don't have a 10% early withdrawal penalty, they are subject to regular income tax upon withdrawal. Additionally, non-governmental 457(f) plans are taxed when the risk of forfeiture lapses, not when the funds are withdrawn. One of the most effective strategies to maximize the benefits of a 457 plan is to make regular contributions. Over time, these contributions, combined with the power of compound interest, can result in significant retirement savings. Despite the potentially limited investment options in some 457 plans, it's still crucial to diversify investments within the plan to balance risk and return. This can involve spreading investments across different asset classes, sectors, and geographical locations. If you have access to other retirement accounts like a 401(k), 403(b), or an IRA, it's beneficial to balance contributions among these plans. Each plan has its own advantages, and a well-balanced retirement strategy can help maximize the benefits of each. A 457 plan is a type of tax-advantaged, deferred compensation retirement plan available for specific employees of government and non-profit organizations. There are two types: 457(b) plans, which are available to all eligible employees and have defined contribution limits, and 457(f) plans, designed for select groups of highly compensated employees and executives, with no defined contribution limits but with risks of forfeiture. The benefits of these plans include pre-tax contributions, the absence of a 10% early withdrawal penalty, and the potential for catch-up contributions. However, potential drawbacks include limited investment options, employer control over assets in certain situations, and the risk of forfeiture associated with 457(f) plans. Maximizing the benefits of a 457 plan involves strategies such as making regular contributions, diversifying investments, and balancing contributions with other retirement accounts if available. The unique characteristics of 457 plans make them an essential consideration in a comprehensive retirement strategy. However, navigating the complexities of retirement planning can be challenging. It's crucial to seek advice from financial advisors or retirement specialists. What Is the 457 Plan?

Types of 457 Plans

457(b) Plan: Government and Non-Profit

Eligibility

Contribution Limits

Benefits and Potential Drawbacks

457(f) Plan: Non-Governmental Tax-Exempt Organizations

Eligibility

Contribution Limits

Benefits and Potential Drawbacks

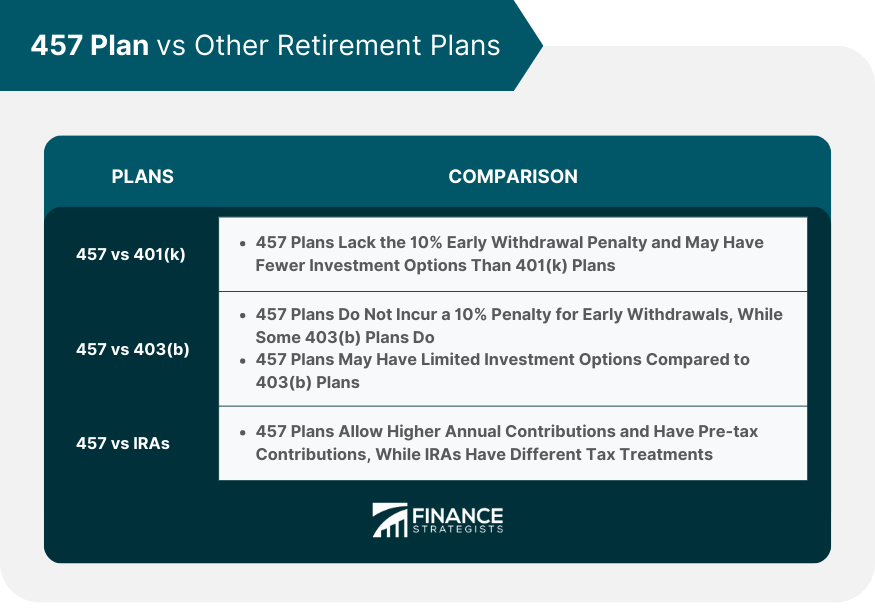

Comparisons With Other Retirement Plans

457 Plan vs 401(k) Plan

457 Plan vs 403(b) Plan

457 Plan vs Traditional and Roth IRAs

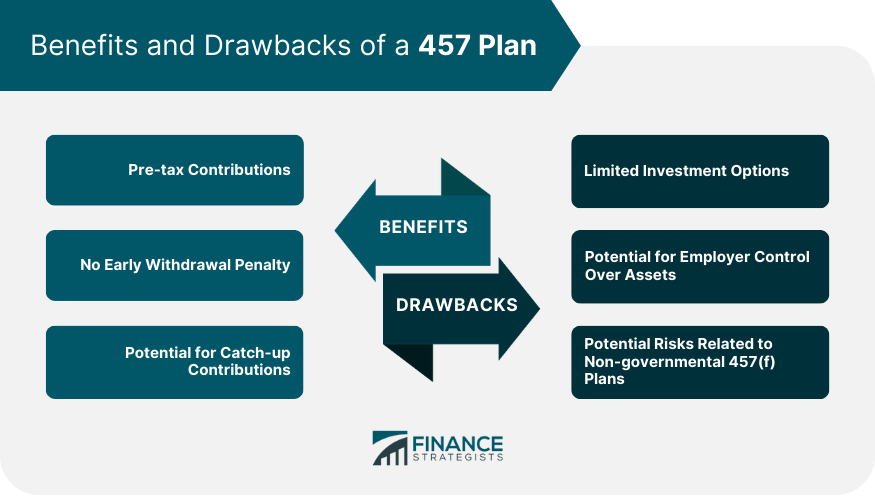

Benefits of a 457 Plan

Pre-tax Contributions

No Early Withdrawal Penalty

Potential for Catch-up Contributions

Drawbacks of a 457 Plan

Limited Investment Options

Potential for Employer Control Over Assets

Potential Risks Related to Non-governmental 457(f) Plans

Rules and Regulations Governing 457 Plans

IRS Rules and Regulations

Employer Rules and Restrictions

Rollover Rules

457 Plan and Tax Implications

Tax Benefits of a 457 Plan

Tax Penalties and Considerations

Strategies for Maximizing 457 Plan Benefits

Regular Contributions

Diversification of Investments

Balancing With Other Retirement Accounts

Final Thoughts

457 Plan FAQs

A 457 plan is a type of tax-advantaged retirement plan offered primarily to state and local public employees and to some non-profit employees. It allows participants to defer a portion of their salaries into the plan for future use, typically retirement.

A primary difference between a 457 plan and a 401(k) or 403(b) plan is the lack of a 10% penalty for early withdrawals before the age of 59½ in a 457 plan. However, 457 plans often have fewer investment options compared to 401(k) and 403(b) plans.

Generally, any employee of a state or local government or a non-profit organization that offers a 457 plan is eligible to participate. For 457(f) plans, typically offered by non-governmental, non-profit organizations, eligibility is often limited to highly compensated employees or executives.

In 2025, the maximum annual contribution to a 457(b) plan is $24,500 ($23,500 in 2025), with an additional catch-up contribution of $8,000 allowed for those aged 50 and above. There are no specified IRS contribution limits for 457(f) plans.

Contributions to a 457 plan are made pre-tax, reducing your taxable income for the year. The funds grow tax-deferred until withdrawal, at which point they are subject to regular income tax. However, unlike many other retirement plans, there's no 10% penalty for early withdrawals made before age 59½.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.