A Variable Benefit Plan (VBP) is a type of retirement savings plan that allows employees and employers to contribute to an individual account, with the employee's retirement income dependent on the performance of the investments in that account. Unlike traditional pension plans, which provide a predetermined and guaranteed income during retirement, the income generated by a VBP is based on the returns of the chosen investments. The main purpose of VBPs is to provide employees with a flexible and portable retirement savings option that can potentially offer higher returns than traditional pension plans. Advantages of VBPs include employee control over investments, tax advantages, and the ability to transfer retirement funds between employers. Traditional pension plans, also known as defined benefit plans, guarantee a specific retirement income based on an employee's years of service and salary. A 401(k) plan is a tax-advantaged, defined contribution retirement plan offered by many employers. Employees can choose to contribute a portion of their salary before taxes, and employers may also contribute to the employee's account. The funds in the account are invested in various options, such as stocks, bonds, or mutual funds. Similar to 401(k) plans, 403(b) plans are tax-advantaged retirement plans designed specifically for employees of tax-exempt organizations, such as schools, hospitals, and religious institutions. Like 401(k) plans, employees can contribute pre-tax income, and employers may also make contributions. A 457 plan is another type of tax-advantaged retirement plan primarily designed for state and local government employees. The main difference between a 457 plan and a 401(k) or 403(b) plan is that 457 plans do not have early withdrawal penalties, allowing employees to access their funds before retirement age without incurring additional taxes. IRAs are tax-advantaged retirement accounts that individuals can establish independently of their employer. There are two main types of IRAs: Traditional IRAs, where contributions may be tax-deductible, and Roth IRAs, where withdrawals are tax-free in retirement. Both types of IRAs have annual contribution limits and various investment options. Cash balance plans are a type of hybrid retirement plan that combines features of both defined benefit and defined contribution plans. Employees have individual accounts, but the employer guarantees a specific rate of return on the account balance. Upon retirement, employees can choose to receive their account balance as a lump sum or as an annuity. Target benefit plans are hybrid plans that set a specific retirement income target for each employee based on factors like age, salary, and years of service. Employees and employers contribute to the plan, and investments are made to achieve the targeted retirement income. However, unlike traditional pension plans, the actual retirement income is not guaranteed and depends on investment performance. Floor-offset plans combine a traditional pension plan with a defined contribution plan. The employer guarantees a minimum retirement income (the "floor") through the defined benefit plan, while employees and employers contribute to a separate defined contribution plan. If the defined contribution plan's investments perform well, the employee's retirement income will be higher than the guaranteed floor. Employers may choose to contribute to their employee's VBP in various ways, such as matching employee contributions up to a certain percentage, providing a set dollar amount, or using a profit-sharing formula. Employer contributions can help incentivize employees to participate in the plan and save more for retirement. Employees can contribute to their VBP through salary deferrals, typically on a pre-tax basis. This allows employees to reduce their current taxable income while saving for retirement. Some plans may also offer a Roth option, allowing employees to contribute after-tax dollars and enjoy tax-free withdrawals in retirement. Stocks represent ownership shares in a company, and their value may increase or decrease based on the company's financial performance. Investing in stocks can offer higher potential returns compared to other investment options but also carries a higher level of risk. Bonds are debt securities issued by governments or corporations. When an investor purchases a bond, they are essentially lending money to the issuer in exchange for periodic interest payments and the return of the principal at maturity. Bonds are generally considered less risky than stocks but offer lower potential returns. Mutual funds pool money from multiple investors to purchase a diversified portfolio of stocks, bonds, or other securities. This diversification helps to spread risk and can provide investors with exposure to various asset classes and investment styles. Mutual funds are managed by professional portfolio managers who make investment decisions on behalf of the fund's shareholders. ETFs are similar to mutual funds in that they provide diversification and professional management. However, unlike mutual funds, ETFs are traded on stock exchanges and can be bought and sold throughout the trading day. This provides additional flexibility for investors and can result in lower fees compared to mutual funds. Target-date funds are a type of mutual fund or ETF that automatically adjusts the asset allocation based on an investor's planned retirement date. As the target date approaches, the fund shifts its allocation from higher-risk investments like stocks to lower-risk investments like bonds. This helps to manage risk as the investor nears retirement. Vesting schedules determine when an employee has a non-forfeitable right to the employer's contributions in their VBP. Some plans offer immediate vesting, while others require the employee to work for a certain number of years before they are fully vested. Understanding the vesting schedule can be important when considering job changes or retirement planning. Withdrawals from a VBP are typically allowed upon reaching retirement age (usually 59½), although some plans may have additional provisions for early withdrawals under specific circumstances. Withdrawals from pre-tax accounts are generally taxed as ordinary income, while Roth account withdrawals are tax-free in retirement. Early withdrawals before retirement age may be subject to additional taxes and penalties, depending on the type of plan and the specific circumstances. Variable Benefit Plans offer flexibility for both employers and employees in terms of contribution amounts, investment choices, and plan design. Employers can tailor their contributions to fit their budget, while employees can adjust their investment strategies based on their risk tolerance, financial goals, and time horizon. Unlike traditional pension plans, VBPs are portable, meaning employees can transfer their retirement savings to a new employer's plan or an IRA when they change jobs. This portability allows employees to maintain a continuous retirement savings strategy throughout their career. VBPs offer the potential for higher returns compared to traditional pension plans, as employees can invest in a wide range of asset classes, including stocks, bonds, and alternative investments. These higher returns can lead to a larger retirement nest egg for employees who effectively manage their investments. With VBPs, employees have greater control over their investments, allowing them to select investment options that align with their individual risk tolerance and retirement goals. This level of control can be empowering and motivating for employees as they take charge of their financial future. VBPs often provide tax advantages for both employers and employees. Employer contributions are generally tax-deductible, while employee contributions can reduce taxable income. Additionally, investment earnings in the plan grow tax-deferred, potentially increasing the overall value of the retirement account. One of the main disadvantages of VBPs is the investment risk that employees assume. Unlike traditional pension plans that guarantee a specific retirement income, the income generated from a VBP depends on the performance of the investments. This means employees may experience lower-than-expected returns or even losses in their retirement accounts. VBPs can be more complex than traditional pension plans, as employees are responsible for choosing their investment options and managing their portfolios. This added complexity may be overwhelming for some employees, particularly those without financial expertise or experience. While VBPs have the potential for higher returns, they also carry the risk of lower retirement income if investments underperform. Employees who do not effectively manage their investments or experience a market downturn close to retirement may find their retirement income significantly reduced. VBPs rely on employee participation to be effective. If employees do not contribute sufficiently to their retirement accounts or make poor investment choices, it may negatively impact the overall success of the plan. ERISA is a federal law that sets minimum standards for retirement plans in the private sector. It provides protections for plan participants, including requirements for reporting, disclosure, and fiduciary responsibilities. Employers offering VBPs must ensure compliance with ERISA regulations. VBPs must also comply with IRS regulations governing tax-advantaged retirement plans, including contribution limits, taxation of withdrawals, and required minimum distributions. Employers and plan administrators should be familiar with these regulations to avoid potential tax penalties and ensure the plan remains compliant. The DOL is responsible for overseeing retirement plan compliance with ERISA and other federal laws. Employers offering VBPs must maintain accurate records and be prepared for potential audits or investigations by the DOL. The PBGC is a federal agency that insures certain private-sector pension plans, including some hybrid plans with defined benefit components. VBPs that include a defined benefit component may be subject to PBGC insurance premiums and reporting requirements. Employers should provide clear and concise communication to employees about the plan's features, benefits, and risks. This includes explaining the investment options, contribution limits, vesting schedules, and withdrawal rules. Providing easy-to-understand materials, such as summary plan descriptions, can help employees make informed decisions about their retirement savings. To help employees manage investment risk and achieve their retirement goals, employers should offer a diverse range of investment options within their VBP. This may include a mix of stocks, bonds, mutual funds, ETFs, and target-date funds that cover various risk levels, industries, and geographic regions. Financial education resources, such as workshops, seminars, or online tools, can help employees better understand their VBP and make informed investment decisions. Employers should consider offering these resources to support employee engagement and promote responsible retirement planning. Employers should regularly review their VBP offerings to ensure they remain competitive, cost-effective, and aligned with the needs of their workforce. This may involve updating investment options, adjusting employer contributions, or modifying plan features to better support employees' retirement goals. Variable Benefit Plans (VBPs) are retirement savings plans that allow both employers and employees to contribute to individual accounts, with retirement income dependent on the performance of the investments in the account. There are various types of VBPs, including defined contribution plans like 401(k)s, 403(b)s, and IRAs, as well as hybrid plans such as cash balance, target benefit, and floor-offset plans. These plans consist of components such as employer and employee contributions, investment options, vesting schedules, and withdrawal options. VBPs offer several advantages, including flexibility, portability, the potential for higher returns, employee control over investments, and tax advantages. However, they also have some disadvantages, such as investment risk, complexity, potential for lower retirement income, and employer reliance on employee participation. As VBPs become increasingly important in the retirement planning landscape, it is essential to understand their features, benefits, and risks. To make the most of a Variable Benefit Plan, employees should consider seeking professional retirement planning services to help them navigate the complexities of VBPs and develop a strategy that aligns with their financial goals and risk tolerance. With the right guidance, employees can maximize the potential benefits of their VBP and secure a comfortable retirement.What Is a Variable Benefit Plan (VBP)?

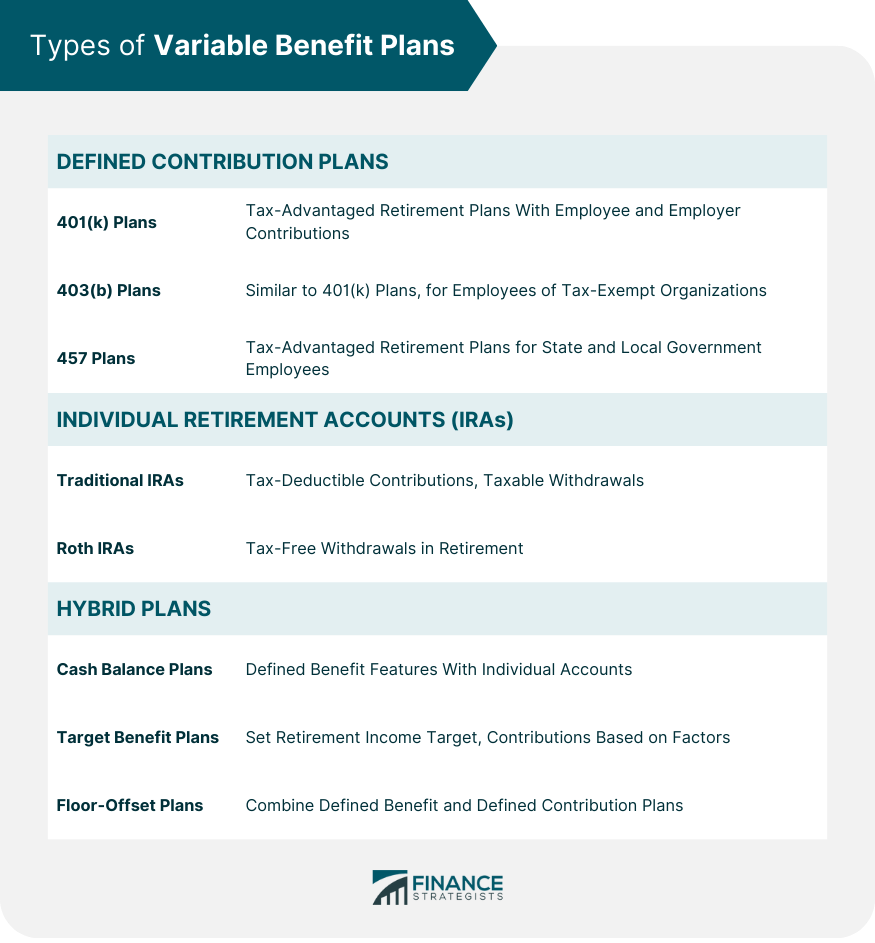

Types of Variable Benefit Plans

Defined Contribution Plans

401(k) Plans

403(b) Plans

457 Plans

Individual Retirement Accounts (IRAs)

Hybrid Plans

Cash Balance Plans

Target Benefit Plans

Floor-Offset Plans

Components of Variable Benefit Plans

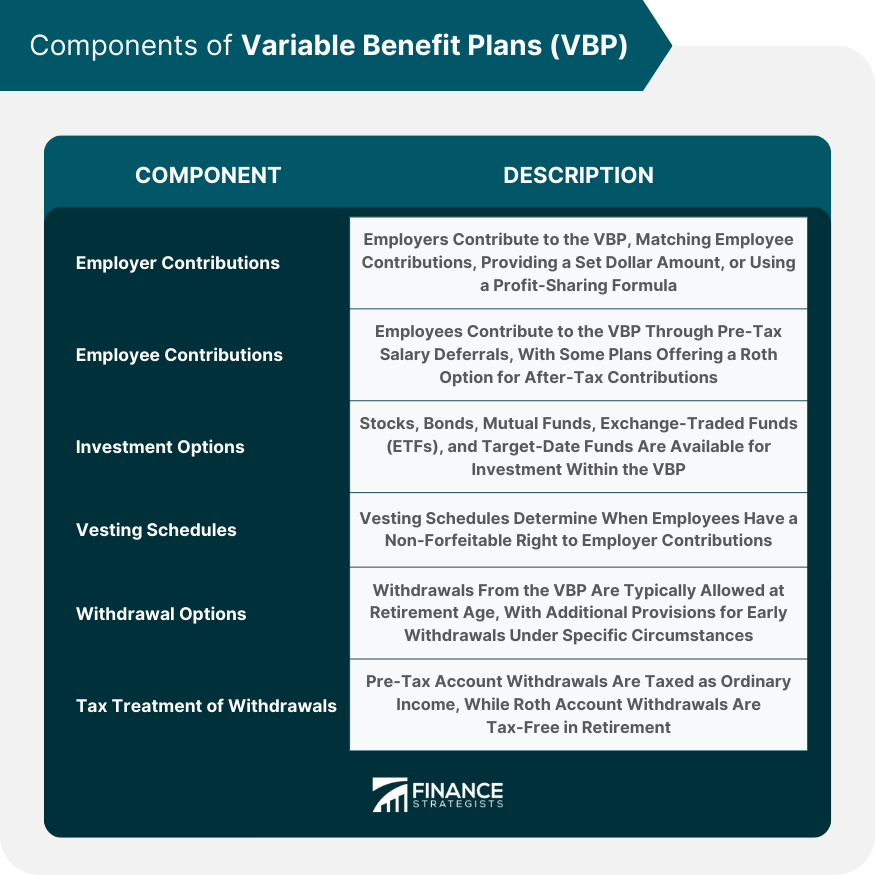

Employer Contributions

Employee Contributions

Investment Options

Stocks

Bonds

Mutual Funds

Exchange-Traded Funds (ETFs)

Target-Date Funds

Vesting Schedules

Withdrawal Options and Restrictions

Advantages of Variable Benefit Plans

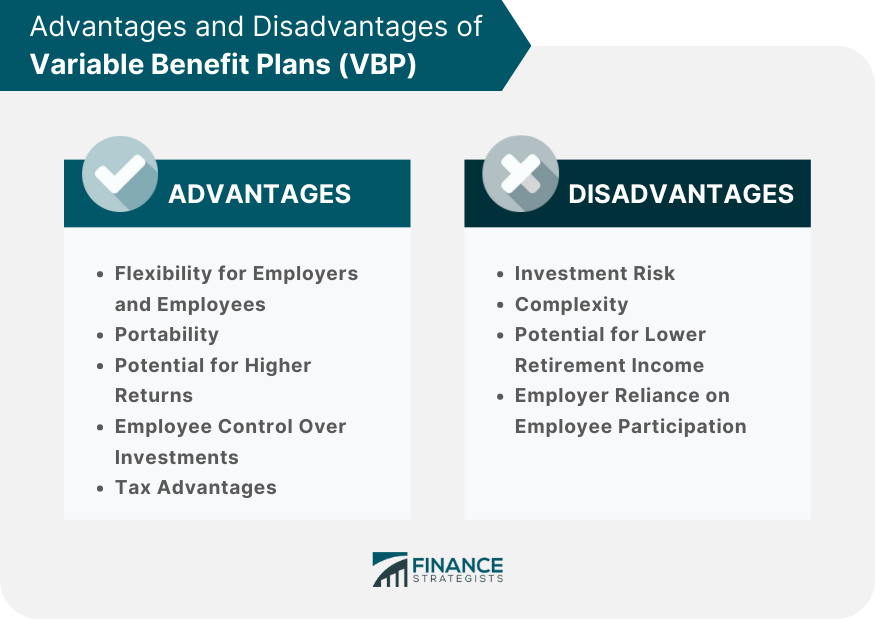

Flexibility for Employers and Employees

Portability

Potential for Higher Returns

Employee Control Over Investments

Tax Advantages

Disadvantages of Variable Benefit Plans

Investment Risk

Complexity

Potential for Lower Retirement Income

Employer Reliance on Employee Participation

Regulatory Framework and Compliance

Employee Retirement Income Security Act (ERISA)

Internal Revenue Service (IRS) Regulations

Department of Labor (DOL) Oversight

Pension Benefit Guaranty Corporation (PBGC) Role

Best Practices for Implementing a Variable Benefit Plan

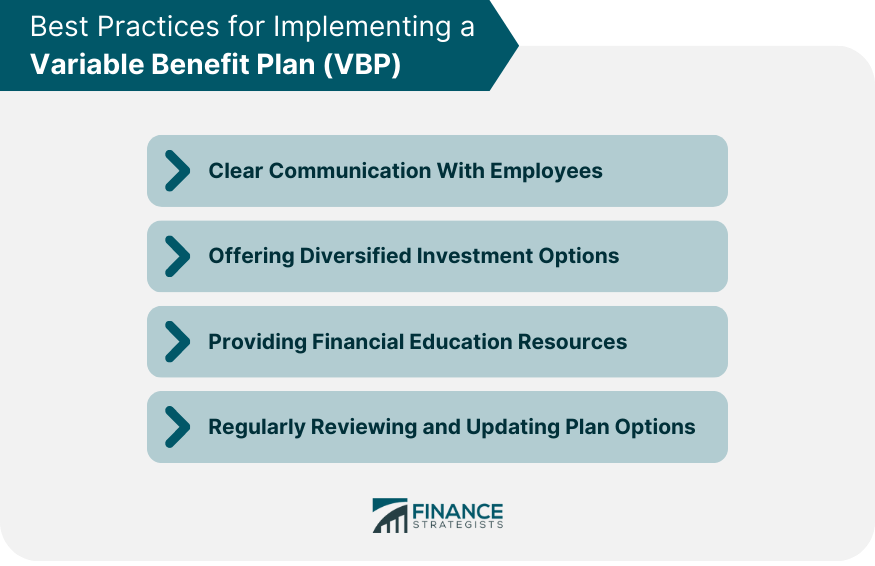

Clear Communication With Employees

Offering Diversified Investment Options

Providing Financial Education Resources

Regularly Reviewing and Updating Plan Options

Final Thoughts

Variable Benefit Plan FAQs

Variable Benefit Plans (VBPs) are retirement savings plans that offer flexibility in contributions and investment choices for both employers and employees. In these plans, retirement income depends on the performance of the investments in the individual's account, making the benefits "variable" based on investment returns.

There are two main types of Variable Benefit Plans: defined contribution plans and hybrid plans. Defined contribution plans include 401(k), 403(b), 457, and Individual Retirement Accounts (IRAs). Hybrid plans combine features of both defined benefit and defined contribution plans and include cash balance plans, target benefit plans, and floor-offset plans.

Variable Benefit Plans offer several advantages, such as flexibility for employers and employees, portability between jobs, the potential for higher returns, employee control over investments, and tax advantages for contributions and investment earnings.

Some risks and disadvantages of Variable Benefit Plans include investment risk, complexity, potential for lower retirement income and reliance on employee participation to achieve desired retirement outcomes. These factors can make VBPs more challenging to navigate compared to traditional pension plans, which typically guarantee a specific retirement income.

To maximize the benefits of Variable Benefit Plans, employees should consider seeking professional retirement planning services, diversifying their investments, contributing consistently, and taking advantage of employer-matching contributions when available. Additionally, employees should stay informed about their plan's features, benefits, and risks to make informed decisions about their retirement savings strategy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.