A spousal rollover is a process by which a surviving spouse can transfer the assets of their deceased spouse into their own accounts, ensuring that these assets can continue to grow tax-deferred and provide financial support. This process is particularly important when dealing with retirement accounts, as it can help to simplify estate planning and provide flexibility in withdrawal options. The main purpose of a spousal rollover are to enable a surviving spouse to assume control of the deceased spouse's assets while maintaining their tax-deferred status. This can help to minimize tax liability, simplify estate planning, and provide financial security for the surviving spouse. In order to be eligible for a spousal rollover, the surviving spouse must be the sole beneficiary of the deceased spouse's account. Additionally, the account must be a qualified retirement or non-retirement accounts, such as an IRA, 401(k), annuity, or life insurance policy. A surviving spouse can roll over assets from a deceased spouse's traditional IRA into their own traditional IRA, allowing for continued tax-deferred growth and potential tax savings. A Roth IRA spousal rollover involves transferring the assets of a deceased spouse's Roth IRA into the surviving spouse's Roth IRA. This allows for continued tax-free growth and qualified tax-free withdrawals. Spousal rollovers can also apply to 401(k) accounts, enabling the surviving spouse to transfer the assets into their own 401(k) account or into a traditional IRA. While not tax-deferred, a spousal rollover can occur for taxable investment accounts, resulting in the transfer of assets from the deceased spouse's account to the surviving spouse's account. Spousal rollovers for annuities allow the surviving spouse to assume ownership of the annuity contract and maintain the tax-deferred status of the assets. A spousal rollover for a life insurance policy enables the surviving spouse to take over the policy and receive the death benefit without incurring taxes. It is essential for the surviving spouse to initiate the spousal rollover process within the designated timeframe, which may vary depending on the type of account and financial institution involved. The first step in initiating a spousal rollover is to contact the financial institution holding the deceased spouse's account. The surviving spouse will need to provide the financial institution with the necessary documentation, including a death certificate and proof of beneficiary status. The surviving spouse will need to decide on the type of account for the rollover and designate new beneficiaries for the account. Spousal rollovers help maintain the tax-deferred status of the assets, potentially minimizing tax liability for the surviving spouse. For certain types of accounts, such as traditional IRAs and 401(k)s, the surviving spouse may be subject to Required Minimum Distributions (RMDs) once they reach a certain age. If the surviving spouse withdraws funds from the account before reaching the age of 59 ½, they may be subject to early withdrawal penalties, depending on the type of account. One of the main benefits of spousal rollovers is the ability to maintain the tax-deferred status of the assets, allowing for continued growth and potential tax savings. Spousal rollovers can help simplify estate planning by consolidating assets and reducing the complexity of managing multiple accounts. A spousal rollover can provide the surviving spouse with greater flexibility in withdrawal options, particularly when dealing with retirement accounts. While spousal rollovers can offer tax benefits, the surviving spouse may still face potential tax liability when withdrawing funds, depending on the type of account. In some cases, spousal rollovers may result in limited investment choices, particularly when transferring assets from a 401(k) to an IRA. Spousal rollovers may complicate matters for non-spouse beneficiaries, who may face additional tax implications or restrictions when inheriting assets. Instead of opting for a spousal rollover, the surviving spouse may choose to inherit the assets directly. This option may be more suitable in certain situations, particularly when dealing with non-retirement accounts. In some cases, the surviving spouse may choose to disclaim the inheritance, allowing the assets to pass to the next beneficiary in line. This option may be beneficial for estate planning purposes or in situations where the surviving spouse does not need the assets. Another alternative to spousal rollovers is establishing a trust, which can provide a more flexible and customizable solution for managing inherited assets. State laws regarding marital property can influence the spousal rollover process, as certain states may have specific rules or restrictions in place. The IRS provides guidelines and regulations surrounding spousal rollovers, which must be adhered to in order to maintain the tax-deferred status of the assets. FINRA also provides guidelines for spousal rollovers, particularly in relation to the transfer of assets and the designation of beneficiaries. Spousal rollovers play a critical role in estate planning, as they can help to simplify the process and ensure that assets are transferred efficiently and effectively to the surviving spouse. Each individual's circumstances will differ, and it is essential to carefully assess one's own financial situation and needs when deciding whether a spousal rollover is the best option. Due to the complexity of spousal rollovers and the various legal and regulatory considerations involved, it is highly recommended to consult with financial and legal professionals when navigating this process.Definition of Spousal Rollover

Purpose and Benefits of Spousal Rollover

Eligibility for Spousal Rollover

Types of Spousal Rollover

Retirement Accounts

Traditional IRA

Roth IRA

401(k)

Non-retirement Accounts

Taxable Investment Accounts

Annuities

Life Insurance Policies

Spousal Rollover Process

Timeframe for Rollover

Steps to Initiate a Spousal Rollover

Contact Financial Institution

Provide Necessary Documentation

Select New Account Type and Beneficiaries

Tax Implications and Considerations

Tax-Deferred Status

Required Minimum Distributions (RMDs)

Early Withdrawal Penalties

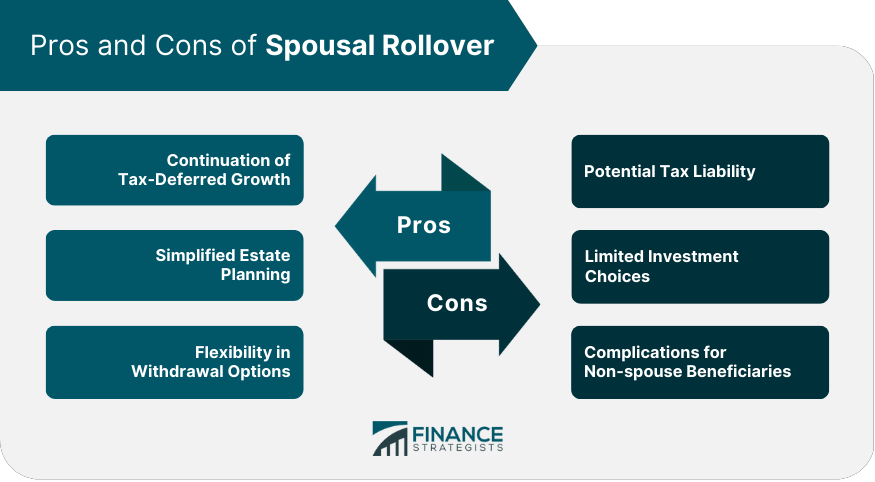

Pros and Cons of Spousal Rollover

Pros

Continuation of Tax-Deferred Growth

Simplified Estate Planning

Flexibility in Withdrawal Options

Cons

Potential Tax Liability

Limited Investment Choices

Complications for Non-spouse Beneficiaries

Alternative Strategies

Inheriting Assets Directly

Disclaiming the Inheritance

Establishing a Trust

Legal and Regulatory Considerations

State Laws and Marital Property

IRS Rules and Regulations

Financial Industry Regulatory Authority (FINRA) Guidelines

Conclusion

Spousal Rollover FAQs

Spousal rollovers offer several key benefits, including the continuation of tax-deferred growth, simplified estate planning, and flexibility in withdrawal options for retirement accounts.

Yes, there are a few potential disadvantages to spousal rollovers, such as potential tax liability upon withdrawal, limited investment choices in some cases, and complications for non-spouse beneficiaries.

Spousal rollovers can be applied to various types of retirement and non-retirement accounts, including traditional IRAs, Roth IRAs, 401(k)s, taxable investment accounts, annuities, and life insurance policies.

The spousal rollover process typically involves contacting the financial institution holding the deceased spouse's account, providing necessary documentation, and selecting a new account type and beneficiary. The timeframe for completing a spousal rollover may vary depending on the type of account and financial institution involved.

Yes, it is essential to be aware of state laws and marital property rules, IRS guidelines and regulations, and Financial Industry Regulatory Authority (FINRA) guidelines when dealing with spousal rollovers to ensure compliance and maintain the tax-deferred status of the assets.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.