A lump-sum distribution is a significant amount of money that is paid out all at once, typically from a retirement plan or pension fund. It can also refer to a large sum received from other sources, such as legal settlements or inheritances. Individuals who receive a lump-sum distribution should carefully evaluate their financial situation and consider the potential consequences. It is crucial to assess how the distribution fits into their overall financial goals and retirement plans. Some people may choose to use the lump-sum distribution to pay off debt, invest in other assets, or purchase an annuity to provide a guaranteed income stream in retirement. Understanding the tax implications, assessing one's financial goals, and seeking expert guidance can help individuals navigate lump-sum distributions effectively and ensure they are used wisely to secure their financial future. A key advantage of a lump-sum distribution is immediate access to funds, which can be helpful for addressing urgent financial needs or fulfilling short-term goals. When you receive a lump-sum distribution, you gain control over the investment of those funds, allowing you to make decisions that align with your risk tolerance and financial goals. With a lump-sum distribution, you can invest the entire amount at once, potentially leading to higher returns if well-managed. In certain cases, a lump-sum distribution may result in a lower overall tax burden, particularly if you can strategically manage your investments and tax liabilities. The risk of poor financial management is a significant downside of lump-sum distributions. If you are inexperienced or make poor investment choices, you could lose a significant portion of the funds. When you take a lump-sum distribution from an employer-sponsored retirement plan, you may lose certain long-term benefits, such as guaranteed income, that could have been available if you had remained in the plan. Lump-sum distributions can have significant tax implications and may result in penalties if not properly managed or if taken before a certain age. Receiving a lump-sum distribution may impact your overall retirement income, particularly if you do not invest the funds wisely or spend them too quickly. Understand the differences in tax treatment for qualified and non-qualified lump-sum distributions, which can significantly impact your overall tax liability. Learn about various rollover options, such as transferring the funds to an IRA or another qualified retirement plan, to minimize or avoid immediate tax consequences. Be aware of the tax implications and potential penalties associated with early withdrawal from retirement accounts before reaching a certain age. Explore strategies to minimize your tax burden when receiving a lump-sum distribution, including tax-efficient investing and strategic withdrawal timing. Before deciding to take a lump-sum distribution, consider factors such as your financial goals, current income needs, tax implications, and investment management skills. Learn various strategies to make the most of a lump-sum distribution, such as investing in a diversified portfolio, creating a budget, and establishing an emergency fund. Understand the rules and tax implications associated with inherited retirement accounts, including required minimum distributions and the various options available to beneficiaries. Learn about structured settlements as an alternative to lump-sum distributions in legal settlements and the pros and cons of each option. Explore the tax implications of receiving a lump-sum distribution from an inheritance or legal settlement, and consider various planning strategies to minimize tax liabilities. Discover the rules and processes for dividing retirement accounts during a divorce, including the potential tax implications and consequences. Understand the importance of Qualified Domestic Relations Orders (QDROs) in the context of divorce settlements and the division of retirement assets. Examine the tax implications and financial planning considerations when dealing with lump-sum distributions as part of a divorce settlement. When deciding between a lump-sum distribution and an annuity, it's essential to understand the key differences, such as the immediate access to funds with a lump sum or the guaranteed income stream an annuity provides. Consider factors such as your financial goals, risk tolerance, tax situation, and current financial needs when deciding between a lump-sum distribution and an annuity. Lump-sum distributions are an essential aspect of financial planning that can significantly affect one's financial future. It is crucial to weigh the advantages, such as immediate access to funds, control over investments, and potential for higher returns, against the disadvantages, which include the risk of poor financial management, loss of long-term benefits, and potential tax consequences. Additionally, considering the unique scenarios in which lump-sum distributions may apply, such as inheritances, legal settlements, and divorce settlements, can help optimize financial planning. By understanding and addressing these key points, individuals can navigate the complexities of lump-sum distributions and make well-informed decisions for their financial well-being.What Is a Lump-Sum Distribution?

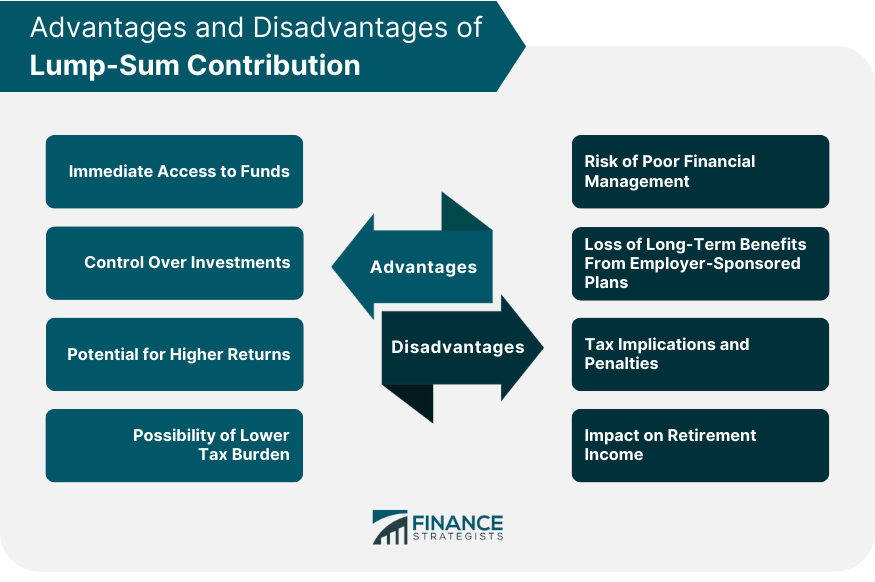

Advantages of Lump-Sum Distributions

Immediate Access to Funds

Control Over Investments

Potential for Higher Returns

Possibility of Lower Tax Burden

Disadvantages of Lump-Sum Distributions

Risk of Poor Financial Management

Loss of Long-Term Benefits From Employer-Sponsored Plans

Tax Implications and Penalties

Impact on Retirement Income

Tax Considerations for Lump-Sum Distributions

Tax Treatment of Qualified and Non-Qualified Distributions

Rollover Options to Avoid Taxes

Tax Consequences of Early Withdrawal

Strategies to Minimize Tax Burden

Lump-Sum Distribution in the Context of Retirement Planning

Factors to Consider When Deciding to Take a Lump-Sum Distribution

Strategies to Make the Most of a Lump-Sum Distribution

Lump-Sum Distribution for Inheritances and Legal Settlements

Inherited Retirement Accounts

Structured Settlements

Tax Implications and Planning Considerations

Lump-Sum Distribution in the Context of Divorce Settlements

Dividing Retirement Accounts

Qualified Domestic Relations Orders (QDROs)

Tax Implications and Financial Planning Considerations

Lump-Sum Distribution vs. Annuities

Comparison of Key Features

Factors to Consider When Choosing Between the Two Options

Conclusion

Lump-Sum Distribution FAQs

A lump-sum distribution refers to a one-time payment made from a retirement plan or a pension fund to an employee or a retiree. The payment is usually made in a single sum and is taxable in most cases.

Yes, you can roll over a lump-sum distribution into an Individual Retirement Account (IRA) or another qualified retirement plan within 60 days of receiving the distribution. By doing so, you can avoid paying taxes on the distribution and continue to save for retirement.

A lump-sum distribution is typically taxable as ordinary income in the year it is received. However, there are some exceptions, such as if the distribution is from a Roth IRA or if it is used for qualified higher education expenses.

If you have a defined benefit pension plan, you may be eligible for a lump-sum distribution if your plan offers this option. The eligibility requirements can vary depending on the plan, so it's best to check with your plan administrator to see if you qualify.

One advantage of taking a lump-sum distribution is that you have access to a large amount of money upfront that you can use for various purposes. However, weighing the pros and cons of a lump-sum distribution versus other options, such as rolling the distribution over into an IRA or taking regular payments over time, is important.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.