An inherited 401(k) is a type of retirement savings plan that is passed down to a beneficiary upon the original account holder's death. It differs from a regular 401(k) plan in several ways. A regular 401(k) plan is an employer-sponsored retirement savings plan where the employee contributes a portion of their salary into the account and receives tax benefits. In contrast, an inherited 401(k) refers specifically to the 401(k) account that is inherited by a beneficiary. If the original 401(k) plan holder was married, their surviving spouse is typically the primary beneficiary of the inherited 401(k). However, this arrangement can be altered if the spouse signs a waiver relinquishing their right. In cases where the original account holder was unmarried, or the spouse has waived their right to inherit the 401(k), the account can be left to children, siblings, other relatives, or even a trust or charity. Beneficiaries of an inherited 401(k) have several options for receiving the funds in the account. These options depend on various factors, including their relationship to the account owner, the account owner's age at death, and the beneficiaries' age upon inheritance.

If a 401(k) owner dies without paying taxes on their retirement savings, the account's beneficiary is responsible for paying instead. However, the beneficiary has some degree of control over the amount owed since this is partly influenced by the withdrawal option they select. For instance, depending on their chosen option, the beneficiary may be required to take minimum distributions each year based on their life expectancy. If the beneficiary fails to do so, they may be subject to tax penalties on the amount that should have been withdrawn. Distributions are taxed as ordinary income, and the beneficiary is responsible for the taxes owed on these distributions. Depending on the method, the beneficiary may be required to pay taxes on the entire distribution, or they may be able to spread the taxes owed over several years. Since inherited 401(k) funds are generally considered taxable income, they must be reported on the beneficiary's tax return. The value of tax owed will depend on the beneficiary's tax bracket and the total value of the inherited 401(k) account. In some cases, the value of an inherited 401(k) may also be subject to estate tax if it exceeds the estate tax exclusion limit. The estate tax rate and exclusion limit are subject to change. It can be helpful to avail tax services for those who wish to avoid any potential tax liabilities. Spousal beneficiaries of an inherited 401(k) have several options when managing their inherited funds. These options include: This option allows the spouse to take a lump-sum distribution of the entire inherited 401(k) balance without triggering an early withdrawal penalty. This may provide the beneficiary with immediate access to the funds but can also result in a significant tax liability in a single year. If the amount contained in the inherited 401(k) is substantial, then a lump-sum distribution could push the spousal beneficiary into a higher tax bracket, increasing the overall amount of taxes owed for the year. A spousal beneficiary can choose to keep the funds in the inherited 401(k) and take distributions based on their life expectancy or their spouse's. The age of both spouses also affects when minimum distributions are required. If the surviving spouse is over 59 ½ and the deceased spouse took the required minimum distributions (RMDs) before death, withdrawals can be continued as scheduled or delayed until the remaining spouse turns 73. For surviving spouses aged 73 and above, taking RMDs is already required. Meanwhile, spousal beneficiaries between 59 ½ and 73 whose deceased spouse was not yet 73 upon death can choose to take RMDs based on the year when their spouse would have turned 73. The spousal beneficiary can ask their custodian to directly transfer the inherited 401(k) to an inherited individual retirement account (IRA) in their name. Withdrawals from this type of account will not be subject to the 10% early withdrawal penalty. This option allows the beneficiary to keep the funds invested while also giving them more control over when they take distributions and how they manage their taxes on those distributions. The spousal beneficiary can also choose to transfer the inherited 401(k) funds to their own retirement plan, such as an IRA or pre-existing 401(k). This option does not come with a tax penalty and is only available for spousal beneficiaries. Once the funds have been transferred, they will be treated with the same tax rules as the other funds in the account. That is, withdrawals are subject to the 10% early withdrawal penalty if taken before 59 ½. Then, RMDs will be required when the surviving spouse turns 73. When a non-spouse beneficiary inherits an account such as a 401(k), there are specific rules and options that must be considered regarding the distribution of funds: Lump-sum distributions allow the beneficiary to receive the funds in a single payment and provide quick access to the funds in the account. However, this option will likely result in a significant tax liability and should be carefully considered. An individual inheriting a 401(k) plan will have to pay taxes on the amount they receive if it is pre-tax. A lump-sum distribution could push beneficiaries into a higher income tax bracket leading to more taxes. Non-spousal beneficiaries who inherited 401(k)s from account owners who passed away before 2019 had the option to withdraw all funds by the conclusion of the fifth year following the account owner's passing. In 2020, this guideline was replaced with the 10-year rule, indicating that non-spousal beneficiaries must completely withdraw funds from their inherited 401(k) account over a period of ten years. This option allows the beneficiary to have access to the funds in a more gradual manner and potentially minimize tax implications. However, failure to withdraw inherited funds within ten years of the account owner's passing may result in a 50% penalty. The option of transferring the funds from an inherited 401(k) to an inherited IRA provides the non-spousal beneficiary with greater control over the investment of the funds. The transferred funds can be invested according to the beneficiary's preference. However, it is important to note that the entire balance of the inherited IRA must be withdrawn within ten years. For pre-tax 401(k)s that are transferred to a pre-tax inherited IRA, the beneficiary has to pay ordinary income tax on the withdrawals made from the account. An inherited 401(k) is a type of retirement savings plan that is passed down from the original account holder to a beneficiary upon their death. Inheriting a 401(k) can be a complex process, and it is essential to understand the rules and regulations surrounding it. If a 401(k) plan owner dies without paying taxes on their retirement savings, the account's beneficiary is responsible for paying instead. However, the beneficiary has some degree of control over the amount owed since this is partly influenced by the withdrawal option they select. Spousal beneficiaries have more options when taking distributions from the account. They can take a lump-sum distribution, keep the money in the plan and take distributions, and transfer the funds to either an inherited IRA or their personal retirement plans. Non-spousal beneficiaries of an inherited 401(k) have fewer options due to the Secure Act of 2019, which requires them to entirely withdraw all funds within ten years of the account owner's passing. They can take a lump-sum distribution, keep the money in the plan, or transfer the funds to an inherited IRA. If they choose not to take a lump-sum distribution, they must withdraw the total within ten years. Exceptions to this rule are minors, chronically ill, and disabled individuals. Understanding the various options available and taking the right steps in managing an inherited 401(k) can help in retirement planning and ensure the funds are used in the most effective manner while taxes and penalties are minimized.What Is an Inherited 401(k)?

Inherited 401(k) Tax Rules

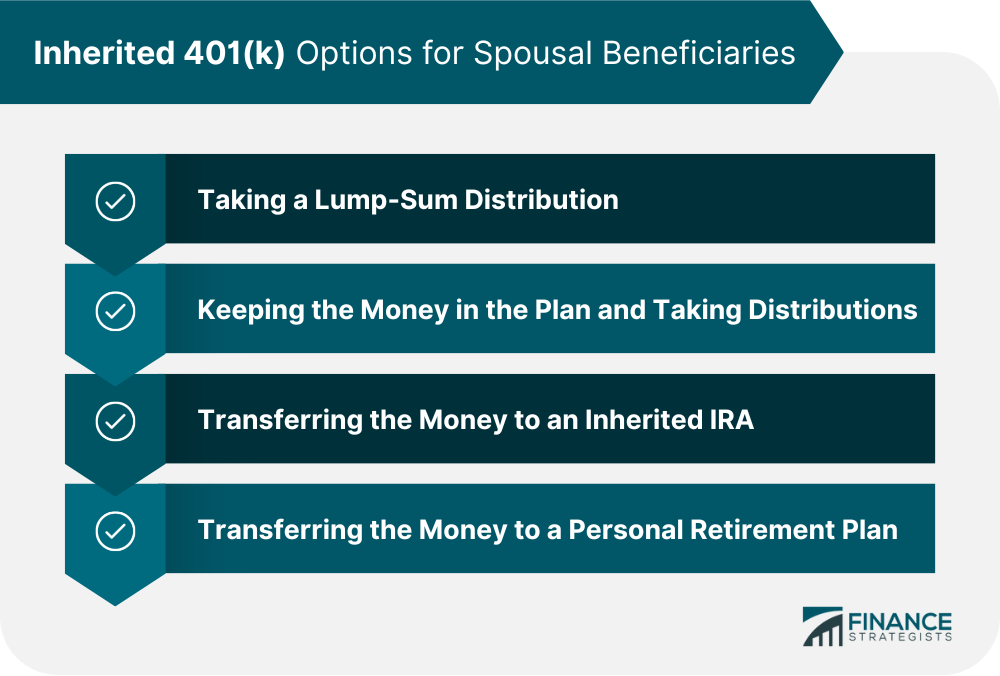

Inherited 401(k) Options for Spousal Beneficiaries

Taking a Lump-Sum Distribution

Keeping the Money in the Plan and Taking Distributions

Transferring the Money to an Inherited IRA

Transferring the Money to a Personal Retirement Plan

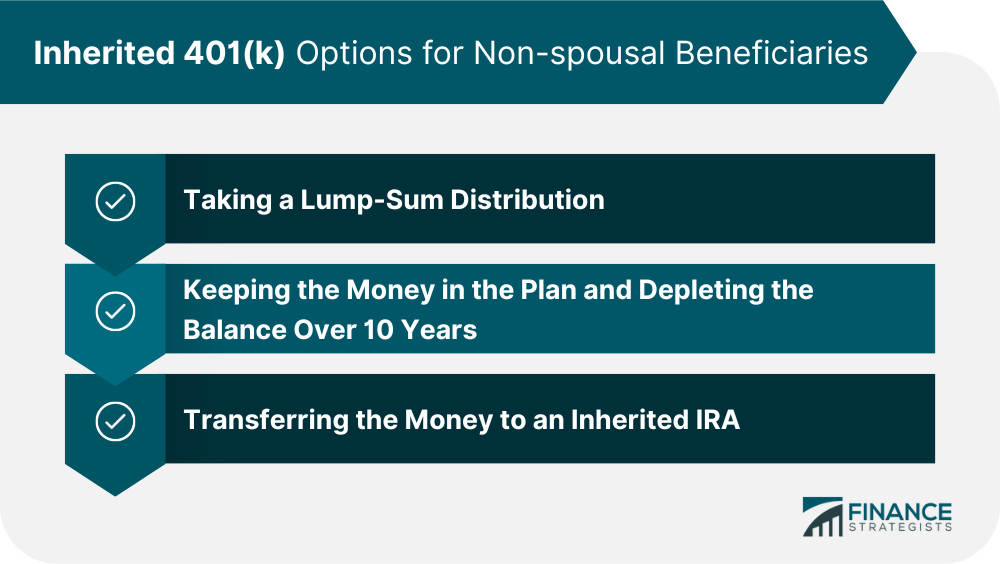

Inherited 401(k) Options for Non-Spousal Beneficiaries

Taking a Lump-Sum Distribution

Keeping the Money in the Plan and Depleting the Balance Over 10 Years

Transferring the Money to an Inherited IRA

Final Thoughts

Inherited 401(k) FAQs

The beneficiary of an inherited 401(k) is responsible for paying taxes on the distributions taken from the account. The tax rate will be based on the income of the beneficiary.

Yes, as a beneficiary of an inherited 401(k), you can withdraw money from the account. The specific tax rules for withdrawing funds may vary depending on whether you are a spousal or non-spousal beneficiary and the age of the original 401(k) account owner at the time of their passing.

The best way to handle an inherited 401(k) will depend on individual circumstances, such as the age of the beneficiary and their retirement goals. Generally speaking, it is advisable to consult a financial advisor to determine the most effective strategy for managing the funds.

If the account owner of a 401(k) passed away in 2019 or earlier, the funds can either be fully withdrawn by their beneficiaries at the end of the 5th year or spread out over the beneficiary's lifetime. For those who died in 2020 onwards, non-spousal beneficiaries must deplete the account's balance at most ten years after the account owner's death.

For those who inherited 401(k)s from account owners who passed away before 2019, beneficiaries were given the option to entirely withdraw all funds by the conclusion of the fifth year following the account owner's passing. In 2020, this guideline was replaced with the 10-year rule, indicating that non-spousal beneficiaries must completely withdraw their inheritance at most ten years after the account owner's death.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.