Fannie Mae, formally known as the Federal National Mortgage Association, plays a pivotal role in the US housing finance system. This government-sponsored enterprise works to provide liquidity, stability, and affordability to the housing market, primarily through buying mortgages from lenders. Its history and impact are deeply intertwined with American housing policies and aspirations. Moreover, its constant evolution means it remains pertinent, even in the face of an ever-shifting housing landscape. In addition to supporting homeownership, Fannie Mae also extends its influence to student housing. Recognizing the unique challenges and needs of student housing investments, Fannie Mae offers tailored financing solutions. These solutions are crucial as they address the burgeoning demand for off-campus student accommodations. As college enrollments soar and the need for quality housing intensifies, Fannie Mae stands at the forefront, offering viable, sustainable solutions. The primary objective of the Fannie Mae Student Housing Loan is to support investors and property owners in acquiring, refinancing, or improving student housing properties. These specialized loans acknowledge the specific nuances and demands of the student housing market. They serve as an important financing vehicle, making quality student housing projects more feasible and financially viable. Student housing loans from Fannie Mae stand out for their customized terms, competitive rates, and flexible options. Tailored specifically for properties that primarily serve student populations, these loans can be instrumental in ensuring that quality student housing is both available and affordable. Their adaptability and borrower-centric features make them one of the top choices for real estate professionals in the sector. While there are similarities between student housing loans and traditional multifamily financing, the differences are notable. The former often offers more flexibility in terms of loan terms and conditions. Moreover, the underwriting process for student housing often considers unique factors like per-bedroom leasing. This distinction can lead to better financial outcomes for borrowers, given the specific dynamics of student housing operations. To qualify for a Fannie Mae student housing loan, borrowers typically need to be a Single Purpose Entity (SPE). However, other entities, including corporations, trusts, or even individuals, may be considered under specific conditions. This versatility in borrower eligibility ensures that a broader spectrum of investors can tap into this financing tool, fostering more diverse investments in student housing. Eligibility is also determined by the nature and operations of the student housing property. Proximity to educational institutions, minimum leasing requirements, and operational durations are some of the critical criteria that properties need to fulfill. These stipulations maintain the quality and purpose of student accommodations, ensuring they genuinely cater to student needs. With Fannie Mae's student housing loan, borrowers have a variety of choices, ranging from short-term five-year loans to long-term loans extending up to 30 years. This flexibility allows investors to choose a loan term that aligns with their financial strategies and objectives. It also provides avenues for diverse investment strategies, be it a short-term flip or a long-term hold. These specialized loans can be utilized for multiple purposes, be it the acquisition of a new student housing property, refinancing an existing loan, or even making significant property improvements. The versatility in the loan's use means that borrowers can leverage it in various stages of their investment cycle, maximizing financial benefits. Loans can be amortized for up to 30 years, ensuring manageable monthly payments for borrowers. This extended amortization period can significantly improve the loan's affordability. It also provides a cushion, especially for new investors, allowing them to stabilize their operations before they contend with larger principal payments. The loan-to-value ratio, commonly known as LTV, indicates the percentage of the property's value that can be financed through the loan. With Fannie Mae's student housing loans, up to 75% LTV is possible, ensuring substantial financial support. A higher LTV can be especially beneficial in areas with rising property values, allowing borrowers to capitalize on market upswings. The Debt Service Coverage Ratio (DSCR) is another vital metric. With a required DSCR of 1.30x for fixed-rate loans and 1.05x for variable-rate loans, Fannie Mae ensures that borrowers have a comfortable margin to service their debt. It acts as a safeguard, ensuring that properties generate enough income to comfortably cover loan repayments. A standout feature of these loans is their non-recourse nature. This means that the borrower's liability is limited, offering added protection and peace of mind. Non-recourse loans can be especially attractive for investors, as they limit personal liability in the event of loan defaults. Loans may be repaid early, subject to a yield maintenance charge for fixed-rate loans and a declining prepayment premium for variable-rate loans. Prepayment terms are crucial in offering borrowers the freedom to navigate their investment journey without being unduly penalized. Fannie Mae offers some of the most competitive interest rates in the market, ensuring affordable financing for investors. This means that over the life of the loan, borrowers can realize significant savings, enhancing the profitability of their investments. A higher Loan-to-Value ratio, like the 75% offered by Fannie Mae, enables borrowers to finance a substantial portion of their property's value. This reduces the upfront capital required, making property acquisition or refinancing more accessible. The non-recourse nature of these loans provides a safety net for borrowers. It ensures that they are not personally liable beyond the collateralized property, a provision that's instrumental in attracting a diverse range of investors. In certain situations, interest-only terms might be available. This option can provide borrowers with lower initial payments, offering financial flexibility, especially during the early phases of property ownership when other costs might be more pressing. Once the primary loan has been in place for a year, Fannie Mae offers the possibility of supplemental loans. This feature can be instrumental in aiding property improvements or expansions, enhancing the property's value and potential income. One distinct advantage is the potential for underwriting based on a per-bedroom rate. Given the nature of student housing, this can often result in a more favorable loan amount compared to traditional multifamily properties. With options for 30-90 day rate locks after commitment and even extended rate locks before closing, borrowers are provided with protection against potential interest rate hikes. This predictability is essential for sound financial planning. Loans being fully assumable means that in the event of a property sale, the new buyer might be able to take on the existing loan, subject to lender approval. This can be an attractive selling point for properties, potentially facilitating quicker sales. The streamlined financing processes, especially when leveraging platforms like Janover, make the borrowing experience efficient and hassle-free. The ease of loan application and approval can often be a deciding factor for many investors. To ensure the viability of the loan, Fannie Mae often requires third-party reports. While these assessments guarantee a thorough evaluation of the property, they can also mean additional costs and extended timelines for borrowers. Typically, lender closing costs can amount to around $12,500, inclusive of third-party reports. These upfront costs need to be factored into the overall financial calculations when considering a Fannie Mae student housing loan. Legal costs associated with these loans can range from $7,500 to $12,500. This is over and above other expenses and can be a significant consideration for borrowers, especially those new to the student housing market. Borrowers need to maintain a replacement reserve of around $250 per unit per year. This fund ensures property upkeep but also means an ongoing financial commitment from the borrower's side. Properties need to adhere to stringent occupancy guidelines, ensuring they cater primarily to students. These requirements, although ensuring the property's student-centric nature, might pose challenges in terms of leasing flexibility. Fannie Mae mandates certain criteria for potential owner/operators. These often include requirements like US citizenship, ample liquid assets, and industry experience. While these guidelines maintain the quality of operations, they can also limit the pool of potential borrowers. Certain stipulations govern lease terms for student tenants. These can include requirements like 12-month leases guaranteed by parents or evidence of employment. While these terms ensure stability, they might limit leasing flexibility, especially in markets with diverse student populations. A 2% rate lock deposit is usually required at the onset. While this deposit is refunded once Fannie Mae purchases the loan, it's an upfront cost that borrowers need to consider. From the initial application to final loan closure, the process spans typically between 45 to 60 days. This window ensures a thorough evaluation while still being timely enough to meet investor needs. The structured process ensures both the lender's and borrower's interests are safeguarded. Every step of the application process, from the initial submission to final loan approval, is meticulously crafted to ensure clarity and transparency. Borrowers are guided through each phase, ensuring they are well informed and prepared for subsequent steps. Janover offers an integrated platform, simplifying and streamlining the loan application process. With tools that enable borrowers to compare loan products, receive multiple quotes, and swiftly navigate through the application phases, Janover proves invaluable. Their platform not only saves time but also ensures borrowers are well-positioned to secure the best financing deals. In today's evolving housing landscape, the significance of Fannie Mae's commitment to student housing cannot be overstated. With rising college enrollments and increasing demand for off-campus accommodations, Fannie Mae's tailored financing solutions emerge as a beacon of support for investors and property owners. By offering competitive terms, flexible options, and a balance of advantages, Fannie Mae addresses the unique challenges of the student housing market. While there are associated costs and stipulations, the overarching benefits provide a compelling case for investors. Leveraging these specialized loans, combined with platforms like Janover, can significantly enhance the feasibility and profitability of student housing projects. As the demand for quality student housing continues to grow, Fannie Mae's role in shaping the future of student accommodations becomes even more pronounced.Overview of Fannie Mae

Understanding Fannie Mae Student Housing Loan

Purpose

Key Features

Comparison to Multifamily Financing

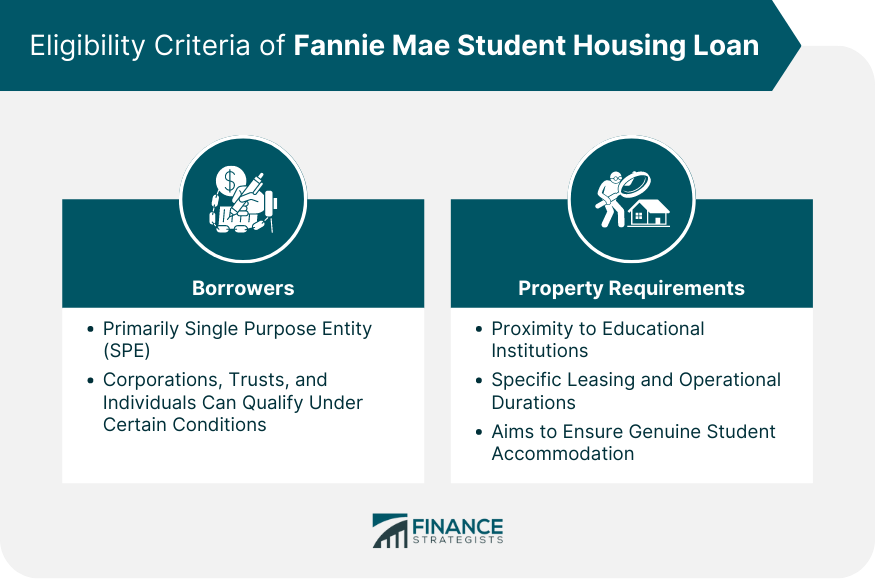

Eligibility Criteria of Fannie Mae Student Housing Loan

Borrowers

Property Requirements

Loan Specifications of Fannie Mae Student Housing Loan

Term Range

Use

Amortization

Max Loan-to-Value (LTV) Ratio

Debt Service Coverage Ratio (DSCR) Criteria

Recourse Conditions

Prepayment Options

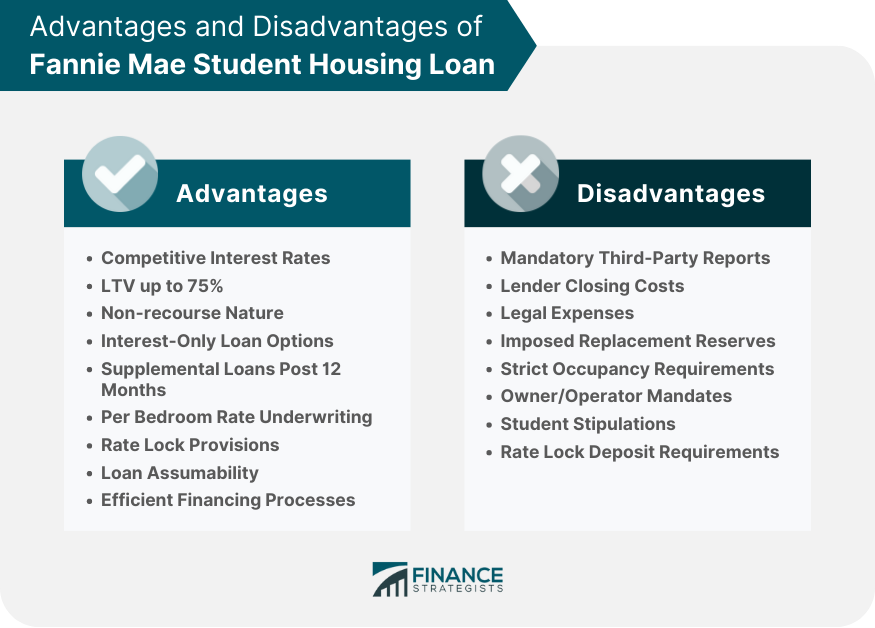

Advantages of Fannie Mae Student Housing Loan

Competitive Interest Rates

LTV up to 75%

Non-Recourse Nature

Interest-Only Loan Options

Supplemental Loans Post 12 Months

Per Bedroom Rate Underwriting

Rate Lock Provisions

Loan Assumability

Efficient Financing Processes

Disadvantages of Fannie Mae Student Housing Loan

Mandatory Third-Party Reports

Lender Closing Costs

Legal Expenses

Imposed Replacement Reserves

Strict Occupancy Requirements

Owner/Operator Mandates

Student Stipulations

Rate Lock Deposit Requirements

Application Process of Fannie Mae Student Housing Loan

Closing Timeline

Application Steps

Janover Platform Benefits

Bottom Line

Fannie Mae Student Housing Loan FAQs

To support investors and property owners in acquiring, refinancing, or improving student housing properties.

They offer more flexibility in loan terms and consider unique factors like per-bedroom leasing.

Competitive interest rates, high LTV, non-recourse nature, interest-only options, and efficient financing processes.

Yes, including mandatory third-party reports, lender closing costs, strict occupancy requirements, and rate lock deposit requirements.

The process spans between 45 to 60 days from initial application to final loan closure.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.