Dedicated to military personnel, the Fannie Mae Military Housing Loan addresses the unique challenges this community faces. Be it frequent relocations or periods of active duty, the loan's structure seeks to provide relief. While it stems from Fannie Mae's overarching goal to support homeownership, this specific loan distinguishes itself by honing in on military needs. Navigating the housing market can be intricate, but this loan aims to simplify that journey for our servicemen and servicewomen. Distinguishing between this and VA loans is vital. Both cater to the same community but differ in their origination, benefits, and requirements. Recognizing these differences can assist potential borrowers in making informed choices tailored to their individual needs, ensuring they gain the most from their loans. The loan, in essence, seeks to serve those with ties to military service. Whether active duty or veterans, the intention is to recognize and assist these individuals. While each category might have nuanced criteria, the underpinning ethos remains constant: support and appreciation. It becomes a bridge connecting service to the country with tangible financial benefits. Service to the nation takes various forms. Accordingly, the loan has provisions that cater to varied durations and types of service. The eligibility criteria reflect a balance between broad inclusivity and maintaining the loan's unique focus. By ensuring benefits reach those genuinely dedicated to service, the loan maintains its integrity and purpose. Financial health remains a crucial evaluation criterion. While military ties are vital, the ability to repay the loan remains paramount. The evaluation might be lenient, considering the distinct financial journeys of military personnel, but it doesn't bypass standard checks. This ensures responsible lending while accommodating the financial realities of those in service. Meticulous documentation serves as a foundation for the application process. While verifying military service forms a cornerstone, other financial and personal documents play a crucial role. Ensuring accuracy and comprehensiveness can streamline the journey, bringing clarity and speed to the application process. Each document serves as a piece in the puzzle, constructing a comprehensive picture of the applicant's financial landscape. Every loan application undergoes a systematic journey. Beginning with preliminary assessments, it moves to more in-depth financial evaluations. Each step, though structured, has its nuances, influenced by individual circumstances. A transparent dialogue with the lender can illuminate this path, demystifying potential complexities. While a general timeframe exists, individual cases might experience variations. The pace often depends on the efficiency of document submission and the clarity of the provided information. A proactive approach, coupled with anticipation of potential queries, can aid in reducing wait times. Engaging in open dialogue with the lender can further ensure that the process is seamless and efficient. Synonymous with military housing loans, VA Loans have carved a unique space. Offering benefits like zero down payments and competitive rates, they remain a prime choice for many. However, their distinct requirements and potential limitations need careful consideration. A thorough analysis, weighing the advantages and potential challenges, can offer clarity. It's about finding the perfect fit, one that resonates with individual needs and aspirations. While not exclusively for military personnel, FHA loans can be an alternative path. Their flexibility in credit qualifications and reduced down payment requirements might appeal to many. But, the embedded mortgage insurance and its implications warrant scrutiny. A side-by-side evaluation with the Fannie Mae Military Housing Loan can help potential borrowers discern the nuances, guiding them towards a decision that aligns with their long-term vision. Venturing into conventional loans brings a broader playing field. These loans, while offering competitive rates and terms, might miss the specific advantages intrinsic to military-focused loans. An exhaustive comparison, diving deep into terms, potential future implications, and individual priorities, can be enlightening. It's about holistic understanding, ensuring every facet of the loan is assessed and understood. Beyond the numbers, the competitive interest rates offered by the Fannie Mae Military Housing Loan symbolize appreciation and recognition for the service of military personnel. In the vast landscape of mortgages, a favorable interest rate can be a beacon for many. Over time, even slight rate variations can amount to substantial differences in payments, underscoring the significance of this benefit. For those committed to long-term homeownership, this aspect can be pivotal. The financial journey of every individual varies. Recognizing this, the Fannie Mae Military Housing Loan extends flexibility in down payments. This nuance aids in minimizing the initial financial hurdles, ensuring that even those with limited savings can envision a future as homeowners. Such provisions are crafted, keeping in mind the unpredictability and financial challenges that come with military life. Beyond monetary incentives, the loan's design takes into account the realities of military life. For a serviceman or servicewoman, challenges like deployment or relocations are frequent. The loan seeks to cushion these aspects, ensuring that their commitment to the country doesn't adversely impact their path to homeownership. The adaptability and understanding embedded in this loan make it a suitable choice for many. Entering the world of home loans comes with its set of fees and charges. With the potential for fee reductions or waivers in the Fannie Mae Military Housing Loan, the financial load lightens. It's not just about easing the monetary strain but also about extending a gesture of gratitude. Every saved dollar can be channeled into making a house a home. Financial situations evolve. Recognizing this dynamic, the loan includes provisions for streamlined refinancing. This flexibility ensures that military personnel can adapt their mortgages to mirror changes in their financial or personal circumstances. With economic landscapes in constant flux, having the option to recalibrate loan terms can be a vital asset. The allure of a spacious home or a prime location can sometimes cloud judgment. While loans facilitate homeownership, it's imperative to match borrowing with repayment capacity. Striking a balance ensures sustainability, avoiding potential financial distress in the future. Having a clear financial blueprint can be instrumental in making decisions that resonate with both the heart and the wallet. The intricacies of loan terms can sometimes be overwhelming. But, neglecting or misinterpreting these can have repercussions. Every clause, no matter how trivial it seems, has implications. Investing time to dissect these, and seeking clarity where needed forms the bedrock of a well-informed decision. It's about proactive engagement, ensuring that the road to homeownership remains devoid of unpleasant surprises. The volatile nature of interest rates adds an element of unpredictability. While rates might seem favorable at the onset, delays or oversight can result in missed opportunities. Proactive communication with the lender, coupled with timely decision-making, can circumvent this pitfall. Being attuned to market movements and having a responsive strategy can yield dividends in the form of favorable rates. Every lender brings their flavor to the table. While the foundational benefits of the Fannie Mae Military Housing Loan remain, variations in terms might exist across lenders. Exploring multiple options, and delving into the fine print, can unearth the best deals. It's about diligence and patience, ensuring that the chosen loan resonates perfectly with individual aspirations. Beyond the principal and interest, several fees influence the total cost of a loan. From processing charges to potential penalties, a multitude of fees can come into play. A comprehensive understanding of these, paired with a quest for transparency, ensures clarity. Seeking detailed breakdowns from lenders can bring to light the true cost of the loan, enabling informed decision-making. A well-structured budget serves as a compass, guiding financial decisions. Before venturing into the loan application, gaining clarity on one's financial capacity and constraints can be empowering. This preparatory step can shape the borrowing decision, ensuring alignment with financial realities. It's about proactive planning and sculpting a path that resonates with both aspirations and capacities. The adage "the devil is in the details" holds particularly true for loan documents. Beyond the highlighted terms, the nuanced clauses carry weight. Meticulously navigating these, and seeking external expertise, if needed, can illuminate the true essence of the loan. Engaging deeply at this stage can prevent potential missteps, shaping a smooth homeownership journey. The world of mortgages can sometimes be labyrinthine. Having a financial advisor as a guide can simplify this journey. Their expertise, combined with an objective perspective, can bring clarity and direction. Whether it's understanding terms or charting a repayment strategy, their insights can be invaluable. Engaging with experts can bring the confidence and clarity needed to navigate the mortgage landscape. Knowledge remains a potent tool. In the context of home loans, this translates to exhaustive research and comparison. Beyond the apparent benefits, delving deep can unearth hidden gems or potential challenges. Investing time and effort in this phase ensures a decision that's both informed and aligned with long-term visions. Clarity on costs is pivotal. Beyond the principal and interest, understanding all associated fees brings transparency to the borrowing journey. By seeking detailed breakdowns and clarifications, borrowers can ensure there are no hidden surprises. Transparent dialogue with lenders at the outset sets the stage for a harmonious relationship, ensuring that the path to homeownership remains smooth and predictable. The Fannie Mae Military Housing Loan stands as a testament to our commitment to honor and support those who serve our country. It is a specialized mortgage solution designed specifically with the challenges and nuances of military life in mind. From its competitive interest rates to its tailored benefits, the loan aims to bridge the gap between service and homeownership. However, like any financial product, it's essential to approach it with knowledge and caution. By distinguishing it from other options like VA or FHA loans, potential borrowers can better identify what aligns with their needs. Key to this process is understanding its benefits, potential pitfalls, and strategies to navigate them. Ultimately, when pursued with a blend of aspiration and prudence, the Fannie Mae Military Housing Loan can become a powerful tool in the homeownership journey for our military personnel, echoing our gratitude for their dedication and service.Understanding the Fannie Mae Military Housing Loan

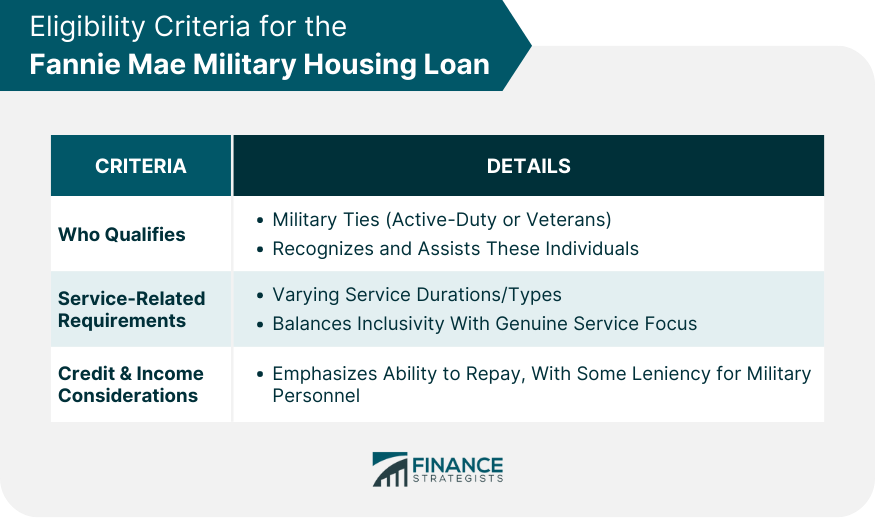

Eligibility Criteria for the Fannie Mae Military Housing Loan

Who Qualifies for the Loan

Service-Related Requirements

Credit and Income Considerations

Application Process for the Fannie Mae Military Housing Loan

Required Documentation and What to Expect

Steps Involved in the Application Process

Estimated Timeline and Tips for Expediting Approval

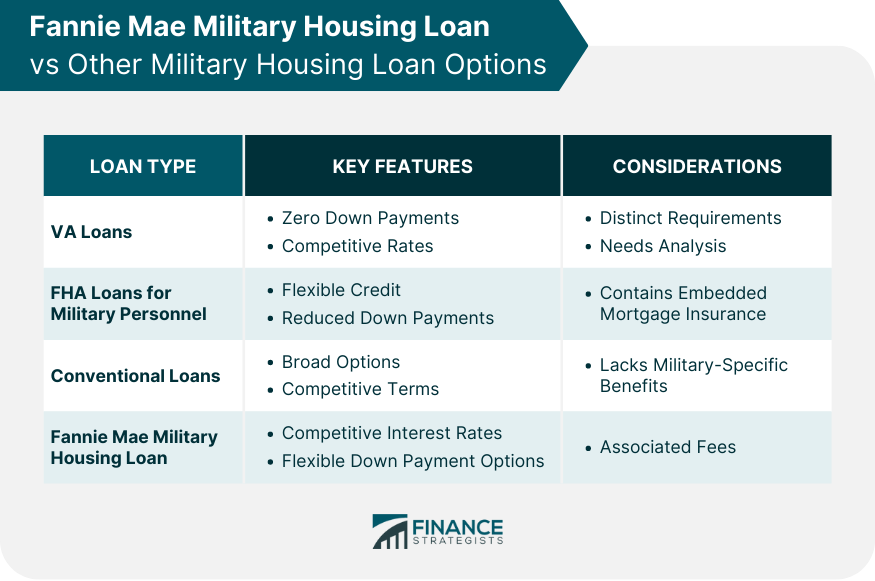

Fannie Mae Military Housing Loan Comparison With Other Military Housing Loan Options

VA Loans

FHA Loans for Military Personnel

Conventional Loans

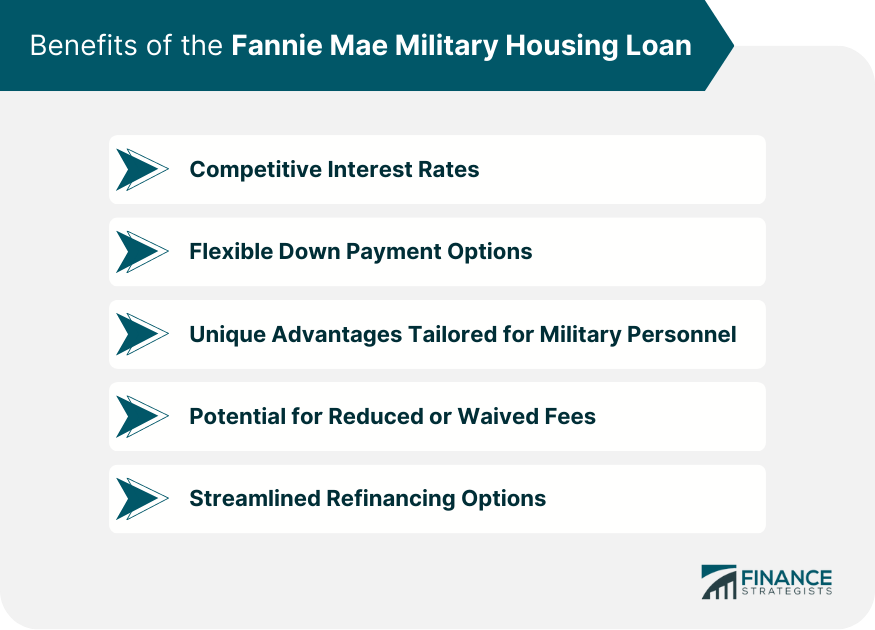

Benefits of the Fannie Mae Military Housing Loan

Competitive Interest Rates

Flexible Down Payment Options

Unique Advantages Tailored for Military Personnel

Potential for Reduced or Waived Fees

Streamlined Refinancing Options

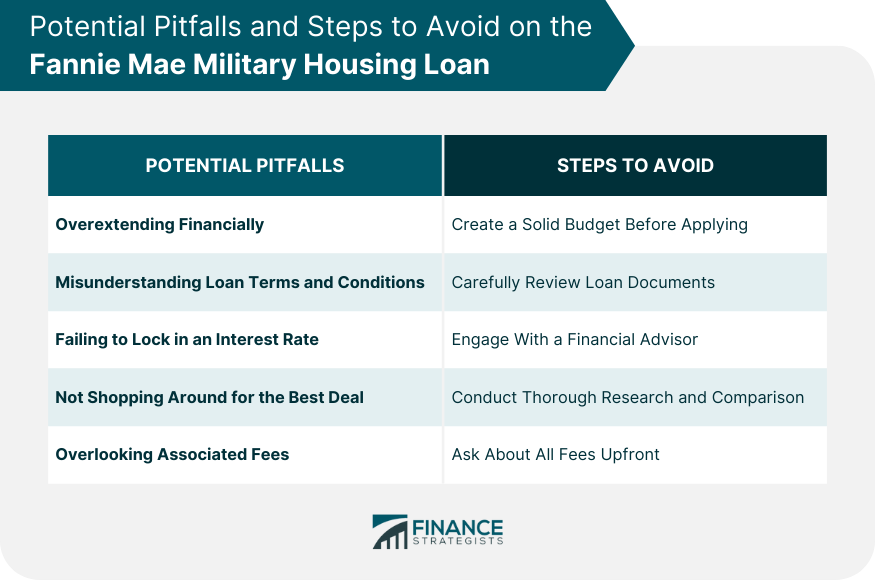

Potential Pitfalls on the Fannie Mae Military Housing Loan

Overextending Financially

Misunderstanding Loan Terms and Conditions

Failing to Lock in an Interest Rate

Not Shopping Around for the Best Deal

Overlooking Associated Fees

Steps to Avoid Pitfalls on the Fannie Mae Military Housing Loan

Create a Solid Budget Before Applying

Carefully Review Loan Documents

Engage With a Financial Advisor

Conduct Thorough Research and Comparison

Ask About All Fees Upfront

Bottom Line

Fannie Mae Military Housing Loan FAQs

It's a mortgage tailored for military personnel, offering benefits like competitive interest rates, flexible down payments, and other unique advantages.

Both cater to military personnel but differ in origination, benefits, and requirements. Fannie Mae's loan offers distinct advantages, but individual needs dictate the best choice.

Active-duty military members, veterans, and certain reservists may qualify, subject to service-related, credit, and income considerations.

Yes, like overextending financially, misunderstanding loan terms, or failing to lock in an interest rate. It's essential to be informed and cautious.

Ensuring accurate and comprehensive documentation, maintaining transparent dialogue with the lender, and proactive decision-making can expedite approval.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.