A Certificate of Insurance is a document issued by an insurance company or broker that verifies the existence of an active insurance policy for a policyholder. It summarizes the insurance coverage, outlining essential details such as coverage limits, policy type, and effective dates. The primary purpose of a COI is to provide proof of insurance to third parties, such as clients, vendors, or landlords. These parties often require proof of insurance to ensure that they are not exposed to unnecessary financial risk in the event of a claim. A COI also helps to build trust between parties, demonstrating that the insured party has taken the necessary steps to protect their business and the interests of others. Three primary parties are involved in a COI: the policyholder, the insurer, and the certificate holder. The policyholder is the insured party, while the insurer is the insurance company providing the coverage. The certificate holder is the third party requesting proof of insurance from the policyholder. The policyholder's information section of a COI includes the insured party's name, address, and contact information. This information is essential for identifying the party responsible for the insurance coverage. The insurer's information section lists the insurance company providing the coverage and their contact information. This section helps the certificate holder identify and verify the insurance provider. The policy number is a unique identifier assigned to the insurance policy. The policy type refers to the specific coverage provided, such as general liability or professional liability. These details help certificate holders understand the scope of the policy and assist in verifying its authenticity. The policy is effective, and expiration dates indicate when the insurance coverage is active. Certificate holders use these dates to ensure that the policy is current and valid. Coverage limits represent the maximum amount that the insurance company will pay for a covered claim. Deductibles are the amounts that the policyholder must pay out of pocket before the insurance company covers the remaining costs. These details give the certificate holder an understanding of the policy's financial parameters and potential exposures. An additional insured is a person or organization that is covered under the policyholder's insurance policy. This section lists any additional insured parties, providing certificate holders with information about who else may be protected by the policy. Endorsements are amendments or additions to the insurance policy that modify the coverage somehow. Special conditions refer to any unique requirements or provisions that apply to the policy. This section outlines any endorsements or special conditions that affect the policy's coverage. The certificate holder's information section includes the name, address, and contact information of the party requesting the COI. This information helps the insurer and policyholder identify the recipient of the certificate and any associated requirements or obligations. The policyholder must contact their insurance provider or broker to obtain a COI and request the document. The insurer will typically require the policyholder to provide specific details about the certificate holder, such as their name, address, and any additional insured or endorsement requirements. Once the insurer has this information, they will generate and issue the COI. The timeline for receiving a COI varies depending on the insurer and the complexity of the policy. In most cases, policyholders can expect to receive their COI within a few business days. However, it's essential to plan ahead and request the document well before it's needed to avoid delays. Typically, there is no direct cost associated with obtaining a COI, as it is a standard service provided by insurance companies. However, if the policyholder requires additional insured endorsements or other policy modifications, there may be fees associated with these changes. Once the policyholder receives the COI, they should provide a copy to the certificate holder, either electronically or in hard copy. In some cases, the insurer may send the COI directly to the certificate holder on behalf of the policyholder. You need to ensure that the COI details are consistent with what you require. If there's a minimum coverage limit that you need, check to see if it's met by the policy. Moreover, ensure that the policy is current and will be active for the duration you need coverage. Different types of insurance may also be relevant, such as general liability, workers' compensation, and auto insurance. Make sure the COI carries the correct type for the intended purpose. The insurer's details are generally specified on the COI. Research the insurer online to see if they're licensed and recognized by visiting the official website of your state's insurance commissioner or department. This step is important because even if a COI looks genuine, it could potentially be fraudulent or the insurance company could be unlicensed or insolvent. Be proactive and ask them to confirm the details of the policy, such as who the insured is, the type of coverage they have, their coverage limits, and the policy's effective dates. By doing this, you are ensuring that the information on the COI matches what the insurance company has on file. This also provides an opportunity to ask any questions you may have about the coverage. Insurance coverage can be cancelled or lapse without the certificate holder's knowledge, leaving them unaware that they are no longer covered. It is a good practice to confirm with the insurance company that the policy is active and will remain so for the duration you need coverage. For businesses seeking an additional layer of protection, you can request to be added to the policy as an "additional insured" or "loss payee". This means you have a certain level of rights under the policy. For example, as an additional insured, you may be covered for claims arising out of the named insured's activities. As a loss payee, you have the right to receive policy benefits directly from the insurer in the event of a loss. Implementing an efficient COI tracking system is essential for managing multiple certificates and ensuring compliance with contractual and regulatory requirements. A tracking system can be as simple as a spreadsheet or as advanced as specialized software designed for COI management. Key features of a COI tracking system include: Centralized storage for all COI documents Easy access for authorized personnel Alerts and notifications for upcoming expiration dates or policy changes Customizable reporting capabilities Regularly monitoring expiration dates is crucial for maintaining continuous insurance coverage and avoiding potential gaps in protection. Policyholders and certificate holders should establish a process for reviewing COIs and requesting updates or renewals as needed. As business needs and risks evolve, updating coverage limits or endorsements on an insurance policy may be necessary. Policyholders should review their policies periodically to ensure they provide adequate protection and make any necessary changes. Similarly, certificate holders should monitor COI updates and verify that any changes meet their requirements. Maintaining open communication with insurance providers and certificate holders is essential for effective COI management. Policyholders should promptly notify their insurer of any changes in their business or risk profile, while certificate holders should clearly communicate their insurance requirements and expectations. While a COI provides evidence of an active insurance policy, it is not legally binding. It does not guarantee that the policy will remain in effect for the duration of the project or contract. Certificate holders should always verify the policy's validity and details with the insurer. Certificate holders must carefully review the policy's details and consult with the insurer or an insurance expert to ensure they understand the coverage. Verify COIs to avoid exposing certificate holders to significant financial and legal risks. It is essential to thoroughly review and confirm the authenticity and accuracy of each COI to protect against potential losses and liabilities. Management of COIs can result in gaps in coverage, compliance with contractual or regulatory requirements, and increased risk exposure. Policyholders and certificate holders must implement efficient tracking systems and processes to ensure their COIs are current, accurate, and meet their needs. A Certificate of Insurance serves as proof of an active insurance policy and plays a vital role in establishing trust and mitigating financial risks for all parties involved. It verifies the existence of insurance coverage and provides essential details such as policyholder and insurer information, policy specifics, coverage limits, and additional insured parties. Obtaining a COI requires contacting the insurance provider or broker, allowing sufficient time for processing, and ensuring the accuracy of the document. To ensure the authenticity and reliability of a COI, verification is crucial. This involves carefully reviewing the COI details, conducting research on the insurance company's credibility, and directly contacting the insurer to confirm policy information. It is essential to be aware of common pitfalls and misconceptions surrounding COIs, such as understanding that a COI is not legally binding and the importance of reviewing coverage limits and exclusions. Effective management of COIs involves establishing a tracking system, monitoring expiration dates and renewals, updating coverage limits and endorsements, and maintaining open communication with insurance providers and certificate holders. What Is a Certificate of Insurance (COI)?

Key Components of a Certificate of Insurance

Policyholder's Information

Insurer's Information

Policy Number and Type

Policy Effective and Expiration Dates

Coverage Limits and Deductibles

Additional Insured Parties

Endorsements and Special Conditions

Certificate Holder's Information

Obtaining a Certificate of Insurance

Requesting a COI From Provider or Broker

Timeline for Receiving a COI

Cost Considerations

Distribution to Relevant Parties

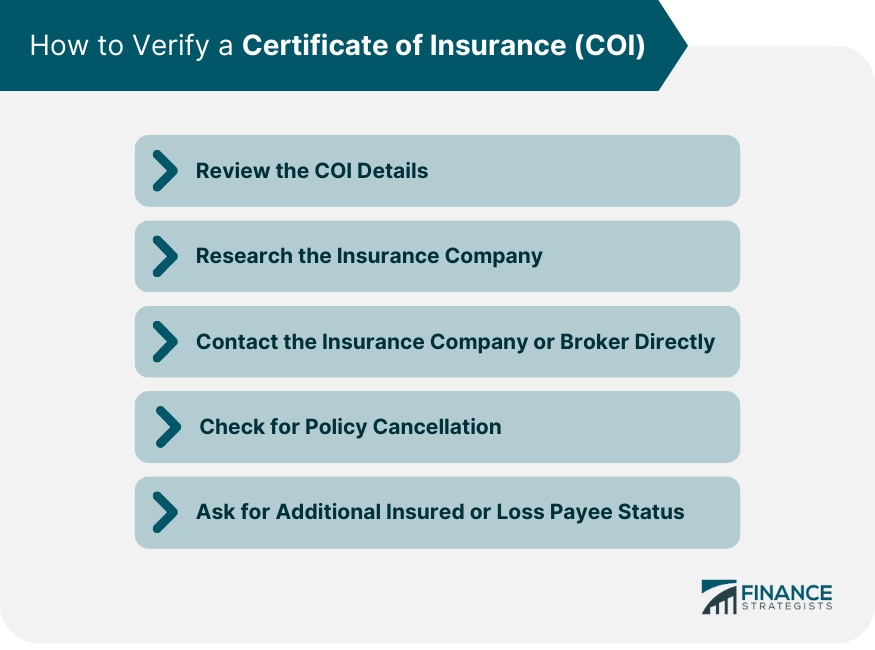

Verifying a Certificate of Insurance

Review the COI Details

Research the Insurance Company

Contact the Insurance Company or Broker Directly

Check for Policy Cancellation

Ask for Additional Insured or Loss Payee Status

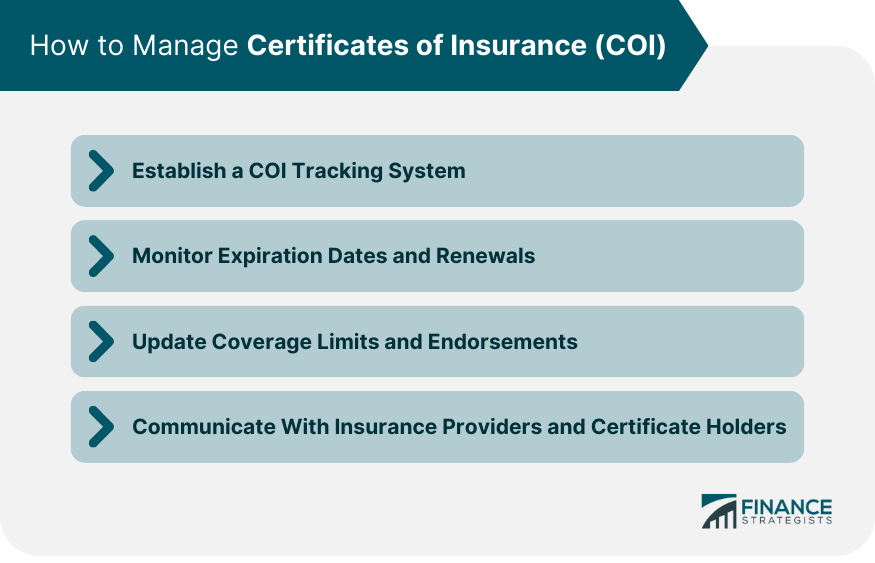

Managing Certificates of Insurance

Establishing a COI Tracking System

Monitoring Expiration Dates and Renewals

Updating Coverage Limits and Endorsements

Communicating With Insurance Providers and Certificate Holders

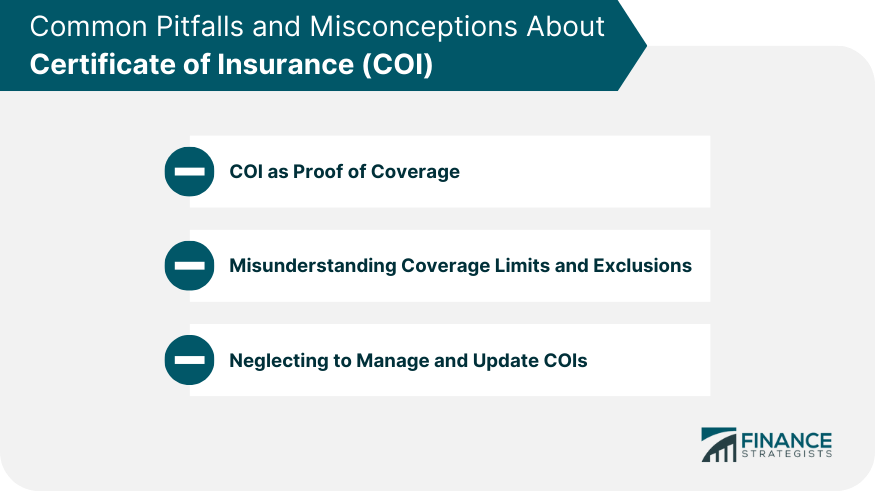

Common Pitfalls and Misconceptions About COI

COI as Proof of Coverage

Misunderstanding Coverage Limits and Exclusions

Neglecting to Manage and Update COIs

Conclusion

Certificate of Insurance (COI) FAQs

A Certificate of Insurance (COI) is a document issued by an insurance company or broker that verifies the existence of an insurance policy. It details the types and limits of coverage, the issuing insurance company, the policy number, the named insured, and the policy's effective periods.

A COI is often required when liability and significant losses are a concern. For example, if you're a contractor, clients might require a COI to prove you have adequate insurance coverage in case of damage or injury during the project. It provides reassurance that there's an insurance policy in place to cover potential risks.

Your insurance company or broker typically provides a COI. After purchasing an insurance policy, you can request a COI from them. In some cases, you can request and receive your COI online through your insurer's website or portal.

Generally, a COI itself does not cost anything. It's a document that your insurance company provides as a part of your insurance policy. However, the cost of the insurance policy itself can vary widely based on the type of coverage, the amount of coverage, your industry, and other factors.

Unfortunately, a COI can be faked, so it's important to verify the information on the certificate. If you're the party requesting the COI, you can contact the insurance company listed on the certificate directly to confirm the policy's validity. Ensuring that the insurance coverage is legitimate and adequate for your needs is crucial.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.