A Certificate of Deposit (CD) ladder is an investment strategy involving the purchase of multiple CDs with varying maturity dates, providing a steady stream of income and minimizing the risk associated with fluctuating interest rates. This approach allows investors to stagger their investments, mitigating the risk of locking all their funds at a low-interest rate. CD ladders can be an effective retirement planning tool, providing a predictable and relatively low-risk source of income. They can be structured to match an investor's retirement timeline and adjusted as needed to reflect changes in financial goals or market conditions. CD ladders can be an excellent way to build an emergency fund, as they provide a degree of liquidity while still offering the potential for higher returns than traditional savings accounts. By staggering the maturity dates, investors can access funds at regular intervals without incurring early withdrawal penalties. CD ladders are a suitable investment strategy for long-term savings goals, such as college tuition or a down payment on a house. They offer a relatively safe and predictable return on investment while still providing the potential for higher returns than traditional savings accounts. A Certificate of Deposit (CD) is a time-bound savings product offered by banks and credit unions that typically pays a higher interest rate than traditional savings accounts. Investors commit to keeping their funds on deposit for a specified term in exchange for a higher return. Interest rates on CDs are generally higher than those on savings accounts, but they may vary based on factors such as the term length, the financial institution, and prevailing market rates. Rates may be fixed or variable, with fixed rates offering more predictability. CDs come with a variety of maturity terms, ranging from as short as one month to as long as ten years or more. Longer-term CDs generally offer higher interest rates, but they also require a longer commitment of funds, which may be a drawback for some investors. Withdrawing funds from a CD before its maturity date usually incurs a penalty, often in the form of lost interest. These penalties can be substantial, making it important for investors to consider their liquidity needs carefully before investing in a CD. The time horizon for a CD ladder refers to the overall length of the investment strategy, which is determined by the individual investor's financial goals and risk tolerance. A longer time horizon generally provides the opportunity for higher returns but may also involve greater risk. An even distribution strategy for a CD ladder involves investing equal amounts of money in CDs with varying maturity dates. This approach provides a consistent stream of income and allows for more predictable liquidity management. An uneven distribution strategy involves allocating different amounts of money to CDs with varying maturity dates. This approach may be tailored to an investor's specific financial goals, risk tolerance, or liquidity needs, providing greater flexibility in managing their investment portfolio. Before constructing a CD ladder, investors should identify their financial goals, risk tolerance, and liquidity needs. These factors will help guide the selection of maturity rungs, the distribution of funds, and the choice of financial institutions for their CD ladder. A short-term CD ladder consists of CDs with relatively short maturity dates, typically ranging from three months to one year. This type of ladder is suitable for investors who prioritize liquidity and flexibility, but may offer lower returns than longer-term ladders. An intermediate-term CD ladder includes CDs with maturity dates that typically range from one to five years. This type of ladder balances liquidity needs with the potential for higher returns, making it a popular choice for investors with moderate risk tolerance. A long-term CD ladder comprises CDs with five years or more maturity dates. This type of ladder is best suited for investors with a longer time horizon and a higher risk tolerance, as it offers the potential for higher returns but requires a longer commitment of funds. Investors should carefully consider the financial institutions they choose for their CD ladder, as factors such as interest rates, account features, and customer service can vary widely. Comparing offerings from multiple banks or credit unions can help investors find the best fit for their needs. Investing in CDs from multiple financial institutions can further diversify a CD ladder and minimize the risk associated with any single institution's performance. This approach can also provide additional FDIC or NCUA insurance coverage, protecting an investor's funds in the event of a bank failure. Brokered CDs are CDs offered by brokerage firms rather than banks or credit unions. These CDs can provide additional diversification and access to a wider range of interest rates and maturity terms. Still, they may also carry higher fees and different risks compared to traditional CDs. When a CD reaches its maturity date, investors can choose to roll over the funds into a new CD with a similar maturity term. This strategy maintains the structure of the CD ladder, providing a consistent stream of income and predictable liquidity management. As CDs mature, investors may choose to adjust the rungs of their CD ladder to better align with their financial goals, risk tolerance, or market conditions. This may involve shortening or lengthening the maturity terms, or reallocating funds among CDs with different maturities. Investors should monitor interest rate trends and be prepared to adjust their CD ladder strategy accordingly. This may involve shifting funds to CDs with different maturity terms or reallocating investments to take advantage of higher interest rates or minimize the impact of rate fluctuations. Regularly reviewing the performance of a CD ladder helps investors ensure they are on track to achieve their financial goals. Monitoring factors such as interest income, maturity dates, and changes in interest rates can provide valuable insights and inform any necessary adjustments to the ladder strategy. CD ladders can be an important component of a diversified investment portfolio. Investors should consider how their CD ladder fits within their overall investment strategy and assess the balance between CDs and other asset classes, such as stocks, bonds, and real estate. CD ladders provide diversification by spreading investments across a range of maturity dates, helping to reduce risk and ensure a more stable return. This strategy helps to balance the potential for higher returns on longer-term CDs with the flexibility of shorter-term CDs. CD ladders help investors manage interest rate risk by staggering the maturity dates of their CDs. This reduces the impact of interest rate fluctuations on their entire portfolio, as only a portion of their investments will be affected at any given time. By structuring a CD ladder with varying maturity dates, investors can ensure they can access funds regularly. This provides a measure of liquidity, allowing them to access their cash when needed without incurring early withdrawal penalties. CD ladders, particularly those with longer maturity terms, can be exposed to inflation risk. If inflation outpaces the interest rates earned on the CDs, the purchasing power of the invested funds may decrease over time, reducing the real return on investment. Withdrawing funds from a CD before its maturity date typically incurs a penalty, which can be significant. Investors should carefully consider their liquidity needs and plan their CD ladder strategy accordingly to minimize the potential impact of early withdrawal penalties. Although CDs are generally considered a low-risk investment, there is a small chance that a bank or credit union could default, putting investors' funds at risk. Diversifying investments across multiple financial institutions and ensuring adequate FDIC or NCUA insurance coverage can help mitigate this risk. A bond ladder is an investment strategy similar to a CD ladder, but it involves purchasing bonds with staggered maturity dates instead of CDs. Bond ladders can offer greater diversification and potentially higher returns but may also carry increased risk and complexity. Money market accounts are a type of savings account that typically offer higher interest rates than traditional savings accounts. They can provide a more liquid alternative to CDs but may have lower returns and be subject to account fees or restrictions. High-yield savings accounts are another alternative to CDs, offering competitive interest rates with greater liquidity. However, the interest rates on these accounts can be variable and may be subject to change, which can impact the predictability of returns. Short-term bond funds invest in a diversified portfolio of bonds with short maturity terms, offering the potential for higher returns than CDs while still providing a relatively low-risk investment. However, these funds may have higher fees and be subject to market fluctuations. CD ladders are a versatile investment strategy that provide a balance of risk management, liquidity, and returns. By investing in CDs with staggered maturity dates, investors can achieve a more predictable stream of income while minimizing the impact of interest rate fluctuations. Before implementing a CD ladder strategy, investors should carefully evaluate their financial objectives, risk tolerance, and liquidity requirements. Understanding individual needs and goals allows for customizing a CD ladder that aligns with an investor's unique financial situation, helping optimize their investment strategy. Maintaining a strong understanding of CD ladders and other investment options is crucial for informed decision-making and long-term financial success. Investors should stay informed about market trends, interest rate changes, and new investment opportunities to make the most of their CD ladder strategy and adapt it to changing conditions as needed. For investors looking to optimize their CD ladder strategy and overall investment portfolio, engaging the expertise of professional wealth management services can be a valuable step. Wealth managers can provide personalized guidance, tailored investment strategies, and ongoing support to help investors achieve their financial goals. Don't hesitate to reach out to a wealth management professional to explore how their services can enhance your investment journey and secure your financial future.What Are Certificate of Deposit (CD) Ladders?

Primary Uses of CD Ladders

Retirement Planning

Emergency Fund Building

Long-Term Savings

Components of CD Ladders

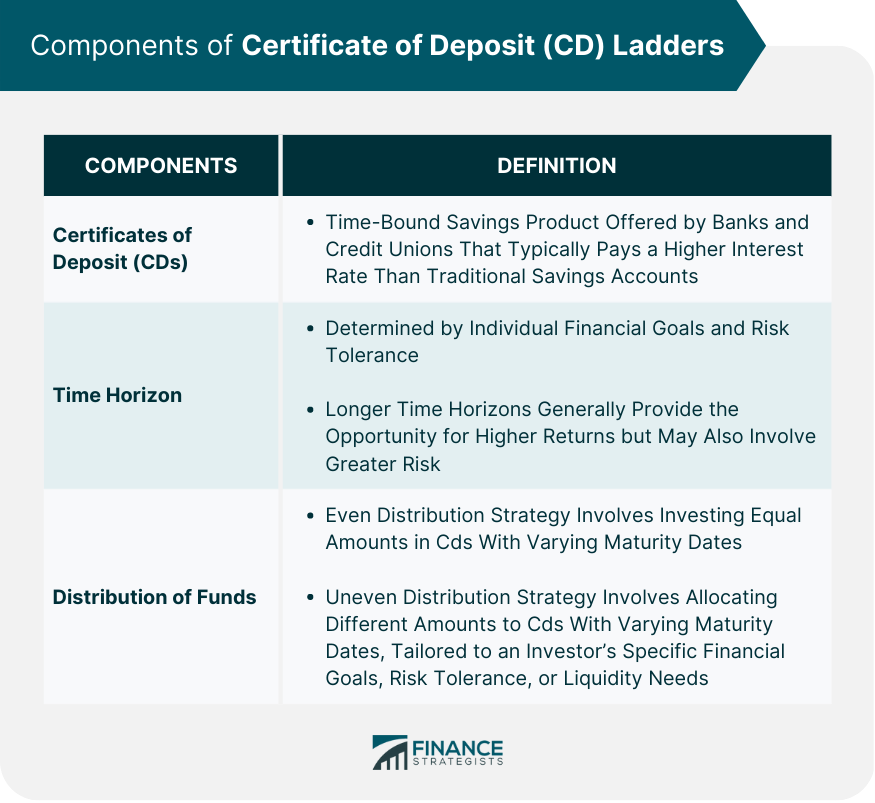

Certificates of Deposit (CDs)

Time Horizon

Distribution of Funds

Even Distribution

Uneven Distribution

Constructing a CD Ladder

Determining Investment Goals

Selecting Maturity Rungs

Short-term CD Ladder

Intermediate-term CD Ladder

Long-term CD Ladder

Choosing Financial Institutions

Diversification Strategies

Multiple Banks or Credit Unions

Brokered CDs

Managing a CD Ladder

Reinvesting Maturing CDs

Rolling Over into New CDs

Adjusting Ladder Rungs

Adapting to Changing Interest Rates

Monitoring CD Ladder Performance

Integrating CD Ladders with Other Investments

Benefits of CD Ladders

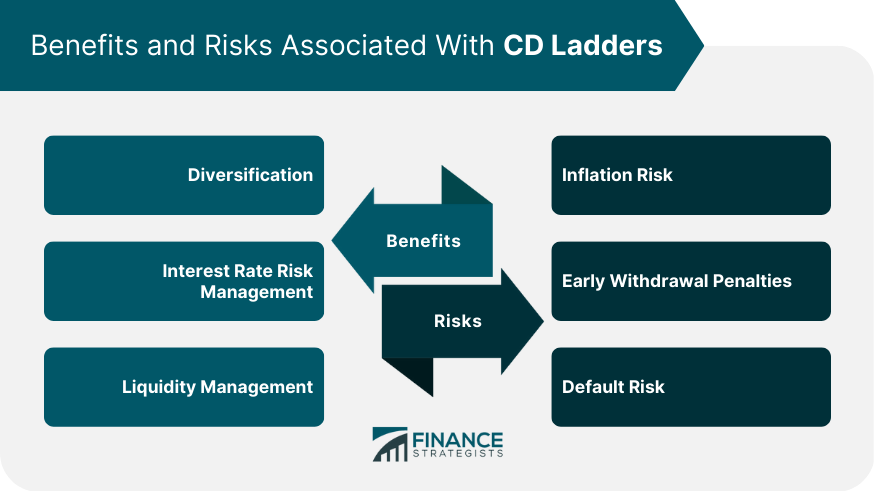

Diversification

Interest Rate Risk Management

Liquidity Management

Risks Associated with CD Ladders

Inflation Risk

Early Withdrawal Penalties

Default Risk

Alternatives to CD Ladders

Bond Ladders

Money Market Accounts

High-Yield Savings Accounts

Short-term Bond Funds

Final Thoughts

Certificate of Deposit (CD) Ladders FAQs

A CD ladder is an investment strategy that involves investing in multiple CDs with varying maturity dates. This approach provides a steady stream of income, diversifies risk, and minimizes the impact of interest rate fluctuations on the investor's portfolio. CD ladders work by staggering investments in CDs with different maturity dates, creating a predictable schedule of maturity dates and allowing investors to reinvest funds as they become available.

CD ladders provide several benefits, including diversification of investments, management of interest rate risk, and liquidity management. They can be used for a variety of financial goals, including retirement planning, emergency fund building, and long-term savings.

Although CD ladders are generally considered a low-risk investment strategy, they are not without risks. Some of the risks include inflation risk, early withdrawal penalties, and default risk. Investors should carefully evaluate these risks and plan their CD ladder strategy accordingly.

To construct a CD ladder, investors must first identify their financial goals, risk tolerance, and liquidity requirements. They must then select the appropriate maturity rungs, choose the right financial institutions, and diversify their investments. Regular monitoring and adjustment of the ladder are also essential to ensuring that it aligns with their investment goals.

Yes, there are several alternatives to CD ladders, including bond ladders, money market accounts, high-yield savings accounts, and short-term bond funds. Each of these options has its own benefits and drawbacks, and investors should evaluate each one carefully before making an investment decision.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.