Interest is the cost of using money, essentially the reward for depositing funds or penalty for borrowing. This monetary exchange stimulates both saving and lending in modern banking. One key concept is compound interest, which exponentially accelerates savings growth. Unlike simple interest calculated solely on the principal amount, compound interest includes both the principal and accumulated interest. This leads to increased savings as each period's earned interest becomes the next period's principal. Interest rates, usually given as an annual percentage rate (APR), significantly influence the growth of bank accounts. A higher rate boosts savings, while a lower rate may not offset inflation, thus eroding purchasing power. Therefore, understanding these elements - especially the difference between simple and compound interest and the role of interest rates - is essential in selecting the right savings vehicle and effective financial planning. The principal amount refers to the initial sum of money deposited into the bank account. It is the foundation upon which interest is calculated. As interest accrues over time, the principal amount remains constant unless additional deposits or withdrawals are made. Keeping track of the principal ensures accurate interest calculations. Interest rates are determined by the financial institution and are influenced by various factors, such as market conditions, central bank policies, and the account holder's creditworthiness. Interest rates may be fixed, remaining constant throughout the account's tenure, or variable, subject to change based on prevailing market rates. Being aware of how interest rates fluctuate and their impact on savings allows individuals to adapt their financial strategies accordingly. The frequency of interest compounding defines how often the interest is added to the account balance. Common compounding periods include daily, monthly, quarterly, semi-annually, and annually. More frequent compounding leads to faster growth, making daily or monthly compounding preferable for higher returns. Understanding the compounding frequency aids in comparing different accounts and assessing the impact on long-term savings. The formula for calculating interest on a bank account depends on whether the interest is simple or compound. For simple interest, the formula is straightforward: For compound interest, the formula is more complex due to multiple compounding periods within a year: Understanding these formulas empowers account holders to compute interest and plan for their financial future more effectively. Savings accounts are designed to encourage individuals to save money for the future. They offer a safe place to keep funds while earning a modest return. Savings accounts are suitable for regular deposits and withdrawals, ensuring liquidity when needed. They are particularly beneficial for people setting aside money for planned expenses or unforeseen emergencies. Interest rates on savings accounts vary depending on prevailing market conditions and the financial institution's policies. Generally, online banks and credit unions tend to offer higher interest rates compared to traditional brick-and-mortar banks. Shopping around for competitive interest rates is crucial for maximizing earnings on savings accounts. Checking accounts serve as a hub for handling daily financial activities, including bill payments, purchases, and direct deposits. They offer the convenience of immediate access to funds through various channels, such as ATMs and online banking. The accessibility of checking accounts makes them suitable for handling regular expenses and managing daily cash flow. In most cases, checking accounts offer nominal interest rates, if any. The focus of these accounts is on providing easy liquidity rather than generating significant interest income. Individuals looking to grow their savings should consider utilizing other account types with higher interest rates while using checking accounts for their transactional needs. Certificates of Deposit, commonly known as CDs, offer higher interest rates than traditional savings accounts. They are suitable for individuals who can afford to set aside their money for a specified period, known as the CD's term. CDs are a preferred option for individuals with a stable financial position and a willingness to lock in their funds for a higher return. CDs require the account holder to deposit a fixed sum of money for a predetermined term, which can range from a few months to several years. During this time, the money is locked, and early withdrawals may incur penalties. CDs are beneficial for individuals who have a specific savings goal in mind and can afford to set aside money without immediate access. CDs typically offer higher interest rates than regular savings accounts due to the longer lock-in period. The longer the term of the CD, the higher the interest rate tends to be. Individuals with surplus funds that they do not need in the short term can take advantage of CDs to maximize their interest earnings. Central banks play a vital role in influencing interest rates by setting the benchmark interest rate for the economy. This rate, often referred to as the "policy rate" or "prime rate," serves as a reference for financial institutions when setting their own interest rates. Changes in the central bank's policy rate can trigger corresponding adjustments in interest rates across various financial products. Interest rates on bank accounts are influenced by the prevailing economic conditions, including inflation, economic growth, and unemployment rates. In times of economic expansion, interest rates may rise to curb inflation, whereas during economic downturns, interest rates tend to decrease to stimulate borrowing and spending. Being mindful of the economic climate helps account holders anticipate potential changes in interest rates. For individuals seeking to open a bank account, their credit score can significantly impact the interest rates offered. A higher credit score reflects a stronger credit history and financial responsibility, resulting in more favorable interest rates on loans and potentially higher interest rates on savings accounts. Maintaining a good credit score is advantageous for obtaining better interest rates on all types of financial products. In some cases, the interest rate offered on a bank account may be tiered, meaning that higher account balances qualify for more favorable interest rates. This encourages savers to maintain larger deposits, rewarding them with increased interest earnings. Account holders with substantial savings should explore accounts with tiered interest rates to maximize their earnings. High-interest accounts offer the potential for faster savings growth, allowing individuals to reach their financial goals more quickly. The compounding effect can be particularly beneficial over longer periods. However, high-interest accounts may come with certain restrictions, such as minimum balance requirements or limited access to funds. Balancing the higher returns against any associated limitations is crucial when choosing high-interest accounts. While low-interest accounts may not offer significant returns, they provide greater liquidity and flexibility. They are well-suited for individuals who require constant access to their funds without the constraints of lock-in periods. Low-interest accounts are suitable for short-term savings or for holding funds that may be needed for immediate expenses. Choosing the right bank account involves striking a balance between risk and reward. Individuals with specific financial goals and timelines should carefully consider the interest rates, fees, and account features before making a decision. Assessing one's risk tolerance and financial objectives can help determine the most suitable account type. To maximize interest earnings on a bank account, individuals can adopt various saving strategies. Consistently contributing to the account, taking advantage of automated savings, and redirecting windfalls into savings are some effective approaches. Setting a regular savings routine ensures consistent growth in the account balance. Aside from traditional savings accounts, alternative options like money market accounts, high-yield savings accounts, and online savings accounts may offer more competitive interest rates. These alternatives can provide better returns for savers willing to explore beyond conventional brick-and-mortar banks. Exploring different account options can lead to better interest rates and improved savings outcomes. Negotiating interest rates with your bank may be possible, especially if you have a strong banking relationship or a high credit score. Being a loyal customer and comparing rates from different banks can also give you leverage in negotiating a better deal. Demonstrating a history of responsible financial behavior can potentially lead to more favorable terms. Interest income earned on bank accounts is subject to taxation. Account holders must report interest earnings on their annual tax returns, even if the bank does not issue a Form 1099-INT. Accurate reporting of interest income ensures compliance with tax laws. While most interest income is taxable, some types of interest, such as municipal bond interest or certain savings bonds, may be exempt from federal income tax. Understanding the tax implications of interest income is essential for accurate tax reporting. Leveraging tax-exempt or tax-deferred accounts can enhance overall tax efficiency. The interest earned on a bank account adds to an individual's total taxable income. Depending on their tax bracket, this additional income may result in higher tax liability. Proper tax planning can help individuals optimize their savings while managing their tax obligations. Being mindful of tax brackets can guide decisions on withdrawing or reinvesting interest income. Inflation refers to the gradual increase in the price level of goods and services in an economy. It erodes the purchasing power of money over time. Account holders must be aware of inflation's effects to preserve the real value of their savings. Inflation impacts the real value of interest earned on a bank account. If the interest rate on the account does not keep pace with inflation, the purchasing power of the savings may decline. Account holders should aim for interest rates that exceed or match the inflation rate to maintain the value of their savings. To safeguard savings from the erosive effects of inflation, individuals can adopt investment strategies that outpace inflation, such as investing in assets with historically higher returns, such as stocks or real estate. Diversifying investment portfolios can help mitigate the impact of inflation and enhance long-term wealth preservation. The workings of interest on a bank account depend on various factors, including the understanding of simple and compound interest, interest rates, and their calculation. This information allows individuals to make informed decisions that can significantly influence their savings and overall financial planning. It's important to comprehend the different types of bank accounts, their respective interest rates, and how these can best serve your financial needs. Moreover, the impact of central bank policies, market conditions, credit scores, and account balances on interest rates cannot be understated. Opting for high or low-interest accounts involves balancing the associated benefits and risks. To make the most of your interest earnings, consistent saving strategies, exploring alternative high-yield options, and effectively negotiating rates are pivotal. Lastly, seeking professional banking services can provide further guidance on these matters and support your financial planning journey.Basics of Interest

How Interest is Calculated

Principal Amount

Interest Rate

Frequency of Interest Compounding

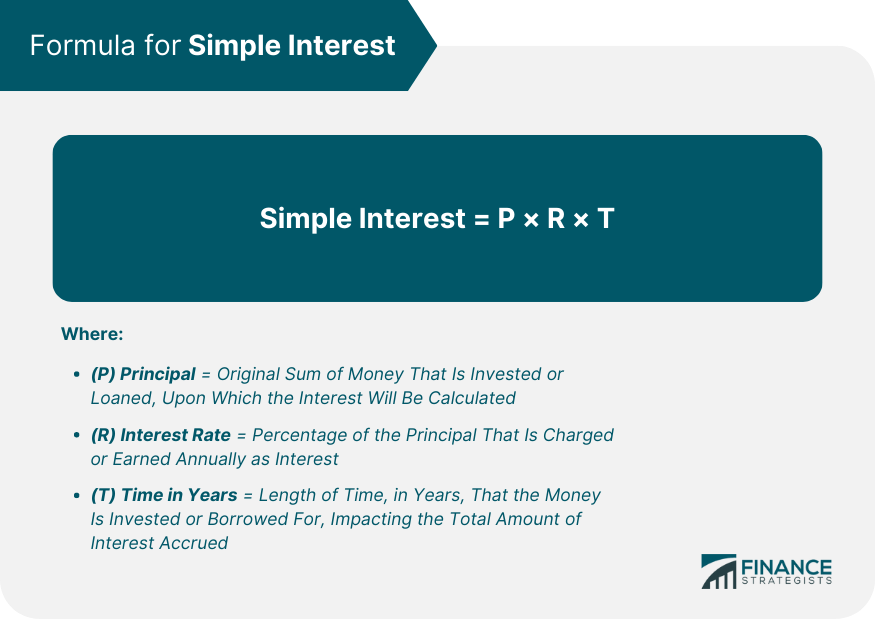

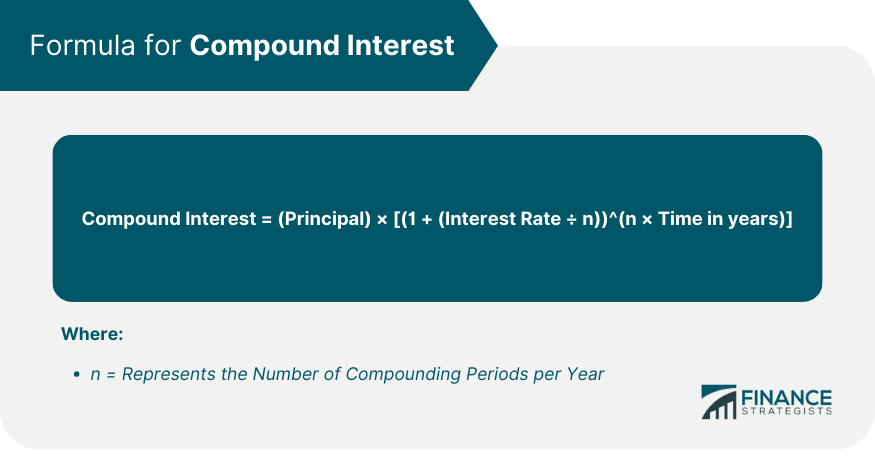

Formula for Calculating Interest on a Bank Account

Types of Bank Accounts and Interest Rates

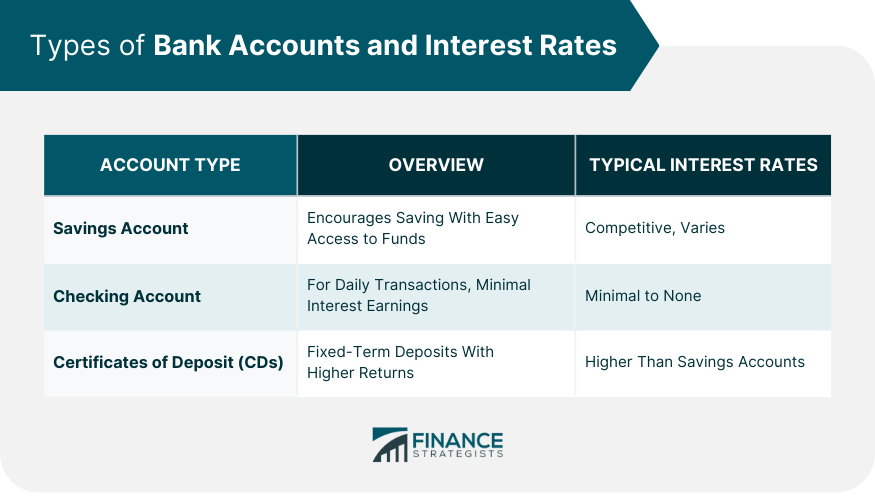

Savings Accounts

Overview of Savings Accounts

Typical Interest Rates for Savings Accounts

Checking Accounts

Overview of Checking Accounts

Do Checking Accounts Earn Interest?

Certificates of Deposit (CDs)

Explanation of CDs and Their Features

How CD Interest Rates Differ From Regular Savings Accounts

Factors Affecting Interest Rates

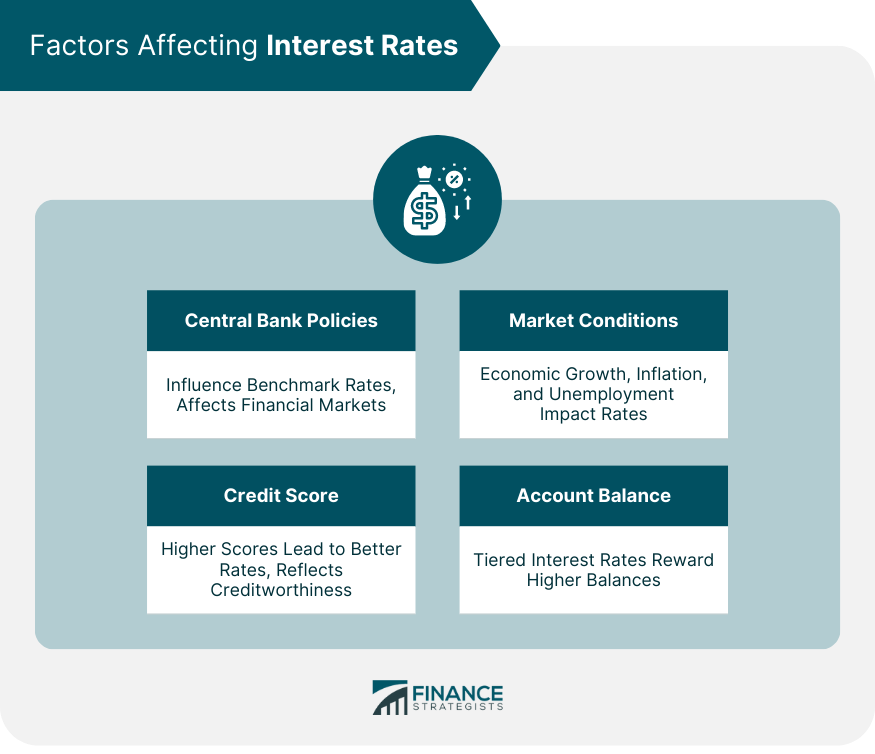

Central Bank Policies

Market Conditions

Credit Score

Account Balance

Risks and Benefits of High vs Low-Interest Accounts

Pros and Cons of High-Interest Accounts

Pros and Cons of Low-Interest Accounts

Balancing Risk and Reward When Choosing a Bank Account

How to Maximize Interest Earnings

Apply Saving Strategies

Explore Alternative High-Yield Savings Options

Negotiate Better Interest Rates

Tax Implications of Interest Income

Reporting Interest Income on Tax Returns

Understanding Taxable vs Tax-Free Interest Income

How Interest Income Affects Overall Tax Liability

Inflation and Its Impact on Interest

Definition of Inflation

Relationship Between Inflation and Interest Rates

Strategies for Mitigating Inflation's Impact on Savings

Bottom Line

How Interest Works on a Bank Account FAQs

Compound interest considers both the principal and earned interest, leading to faster growth, while simple interest is calculated solely on the initial amount deposited.

Compare savings, checking, and CDs. Consider factors like compounding frequency, account balance, and the impact of inflation to optimize your earnings.

A higher credit score can qualify you for better interest rates on both loans and savings accounts, allowing you to earn more on your deposited funds.

Consistent saving, automated deposits, and exploring high-yield savings options can help you earn more interest on your bank account balance.

To mitigate inflation's erosion, consider investments that outpace inflation, like stocks or real estate, to preserve the value of your savings.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.