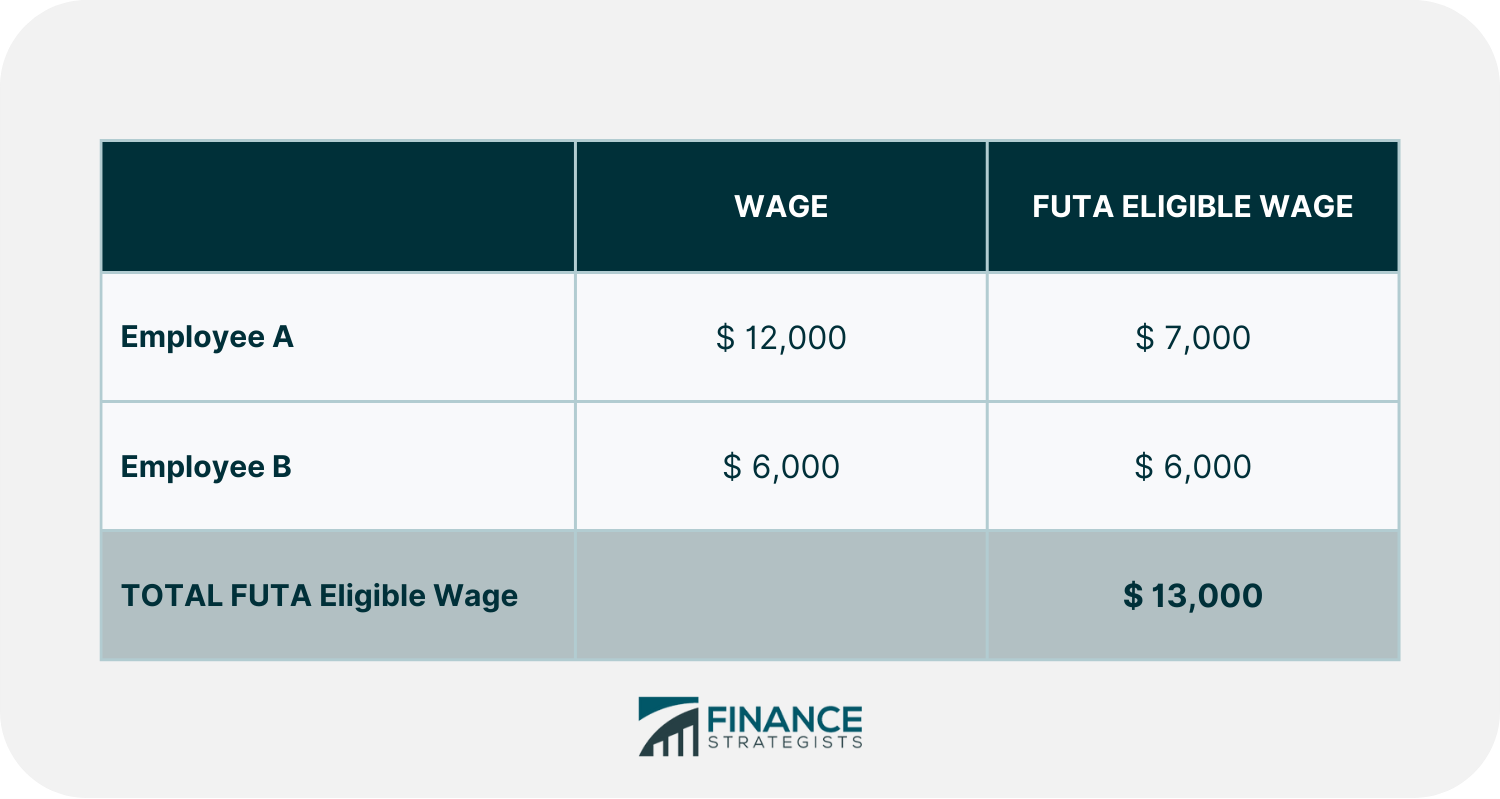

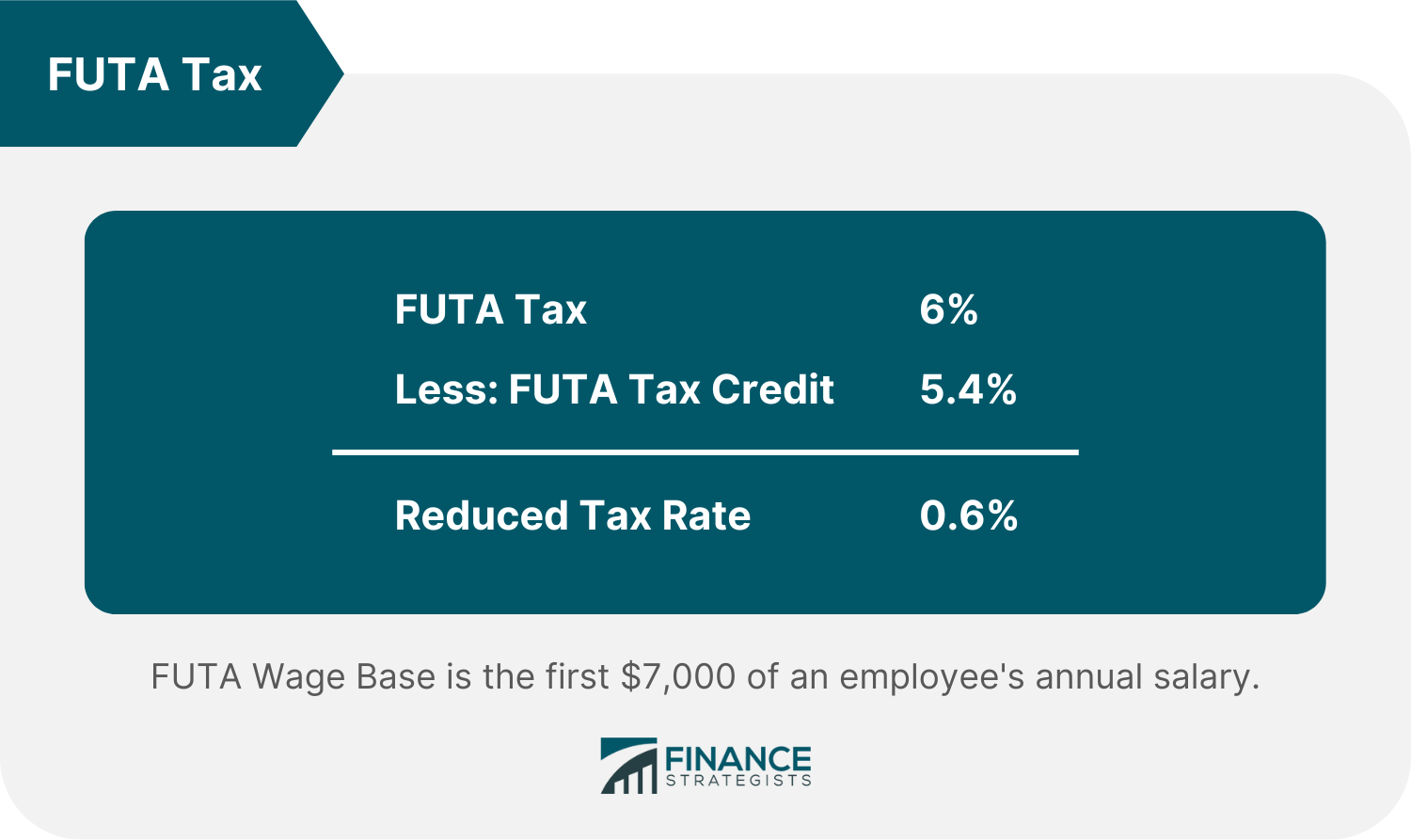

The Federal Unemployment Tax Act (FUTA) was the 1939 federal law that created a payroll tax to fund unemployment benefits. It mandates employers to pay unemployment FUTA tax to fund state unemployment programs. FUTA tax is unique from other types of payroll taxes, such as the Social Security tax, which is imposed on both employees and employers equally. The current FUTA tax rate is 6%. The first $7,000 in wages each employee receives during the course of the year is subject to tax. The laws of each state may cause your state wage base to differ. The requirements for filing FUTA reports differ depending on the underlying entity that is responsible for remitting taxes to the IRS. To find out if your business is required to pay FUTA, the IRS looks at two things: You might be categorized as a household employer if you give wages to employees who perform tasks in or close to your home. An individual working in a family may do so on a temporary or less-than-full-time basis. Household workers must pay FUTA under the following conditions: Household employers can file FUTA taxes on Form 1040's Schedule H instead of Form 940. Agricultural employers have different criteria. FUTA tax collection and reporting are required if the employer meets one of the following conditions: An organization that qualifies for section 501(c)(3) of the Internal Revenue Code exemption from income tax is likewise exempt from FUTA. This exception cannot be waived. Religious, educational, scientific, charitable, and other tax-exempt organizations are exempt from FUTA. Services provided by state or municipal governments are also exempt. Indian tribal governments are free from paying taxes as long as they adhere to all state unemployment insurance requirements. Any branch, subsidiary, or company that is completely owned by the tribe is exempt from this requirement. When figuring out your FUTA taxes, it is important to understand what types of income are taxable. The first $7,000 per employee per year is generally tax-free, but any amounts over that limit are taxable. This includes salaries and wages, commissions, bonuses, vacation allowances, sick pay, and contributions to retirement plans. Depending on the laws of that state, your state's wage base can change. Let us take, for example, Employee A was paid $12,000 in FUTA-taxable wages in Q1, and Employee B was paid $6,000 in FUTA-taxable wages in Q1. Only the first $7,000 of Employee A's wages per quarter is liable to tax. Hence, the tax liability equals: FUTA Liability = (Employee A's Eligible Wages + Employee B's Eligible Wages) x 6% = ($7,000 + $6,000) x 6% = $780 When businesses submit their Form 940, Employer's Annual Federal Unemployment Tax Return, they are typically eligible for a credit of 5.4%, resulting in a net FUTA tax rate of 0.6% (6.0% - 5.4% = 0.6%). Using the same example above, the FUTA liability net of the tax credit will be: FUTA Liability (net of the tax credit) = $13,000 x 0.006 =$78 FUTA tax liability for the company is only $78 after the tax credit. States that have to borrow money from the federal government to pay unemployment benefits are known as credit reduction states. They take out a loan from the Federal Unemployment Trust Fund of the government if they cannot pay unemployment insurance benefits for their residents. State reduction states are not eligible to claim the maximum credit reduction available and will have to pay more tax since the standard credit against the full FUTA tax rate has been reduced. The FUTA credit rate will reduce until the loan is repaid for states with an outstanding balance for two consecutive years and cannot pay in full in the second year. The reduction schedule for FUTA taxes is 0.3% for the first year and 0.3% for each following year until the loan is repaid in full. If a state has not fully paid these loans, it will be ineligible for the maximum credit reduction of 5.4% and is subject to higher FUTA taxes than other states. However, if a state has fully paid off these loans, it can claim the maximum credit reduction of 5.4% and will only pay 0.6% in FUTA taxes. If a loan debt is still outstanding and specific criteria are not met, additional offset credit reductions may apply to a state beginning with the third and fifth taxable years. The Department of Labor (DOL) manages the loan program and will make any necessary credit reduction announcements following the November 10 deadline each year. The FUTA tax does not apply to the following types of payments and some other conditions: It is important to understand how to report your FUTA tax return correctly to avoid any penalties. Employers must submit Form 940, Employer's Annual Federal Unemployment Tax Return, to the IRS each year to report any FUTA tax payments they have made throughout the year, including any FUTA payments that are still due. Information about your business must be provided, including your trade name, address, and employer identification number (EIN). You must also give the entire amount of wages paid to employees, the total amount of wages exempt from the FUTA tax, and the total FUTA tax liability. The filing deadline for Form 940 is January 31. You have until February 10 to file your FUTA tax return, but only if you deposited the full amount when it was due. If the deadline for filing a return falls on a Saturday, Sunday, or a holiday that is recognized by law, you have until the first business day after the holiday to submit the return. You can submit Form 940 to the IRS electronically or by mail. Choosing the e-filing option will help you save time, guarantee security and accuracy, and will allow you to receive an acknowledgment within 24 hours. If you want to e-file your tax return, you have two choices: you can do it yourself, or you may hire a tax expert to do it for you. You will need to buy IRS-approved software if you decide to submit it yourself. If you hire a tax professional, you can refer to the Authorized IRS e-file Provider Locator Service. For the mailing option, you can choose the address based on your location and whether you are mailing your return with or without payment. For further reference, you may check the Instructions for Form 940 provided by the IRS. Although Form 940 is for a calendar year, you must deposit your FUTA tax before submitting your return. You can make electronic fund transfers using the Electronic Federal Tax Payment System (EFTPS). The following table will guide you on when to make deposits according to your FUTA tax liability. Liabilities owed for credit reduction must be included with your fourth quarter deposit in years where credit reduction states apply. When you submit your Form 940, you can include payment by completing Form 940-V, known as a Payment Voucher. FUTA, SUTA (State Unemployment Tax Act), and FICA (Federal Insurance Contributions Act) are federal and state laws that provide funds for basic government programs. FUTA and SUTA are taxes imposed on employers to provide unemployment compensation to laid-off workers. For SUTA, some states require both the employer and employee to pay, but this is only limited to Alaska, New Jersey, and Pennsylvania. States may exempt companies from the SUTA tax. For instance, a state may exempt nonprofit organizations and businesses with fewer workers. The exemptions differ by state, so verify your state's legislation. FICA requires employees and employers to pay to help fund Social Security and Medicare. Employers deduct social security taxes from their employee's paychecks and pay an equal amount. The majority of salaries have FICA taxes deducted. The Federal Unemployment Tax Act (FUTA) is a federal law requiring employers to pay a tax to fund unemployment benefits to laid-off workers. Employers who also pay state unemployment insurance may be eligible for a federal tax credit of up to 5.4%, resulting in a 0.6% effective FUTA tax rate. FUTA and SUTA are the same taxes imposed on different levels of government intended to fund unemployment compensation. In comparison, the FICA tax is intended for Social Security and Medicare.What Is the Federal Unemployment Tax Act (FUTA)?

Who Needs to Pay FUTA?

Businesses

Household Employers

Agricultural Employers

Other Employers

How to Calculate FUTA Tax Liability

FUTA Credit Reduction State

Payments Exempt From FUTA Tax

Reporting FUTA Tax Return

Form 940

When to File Form 940

Where to File Form 940

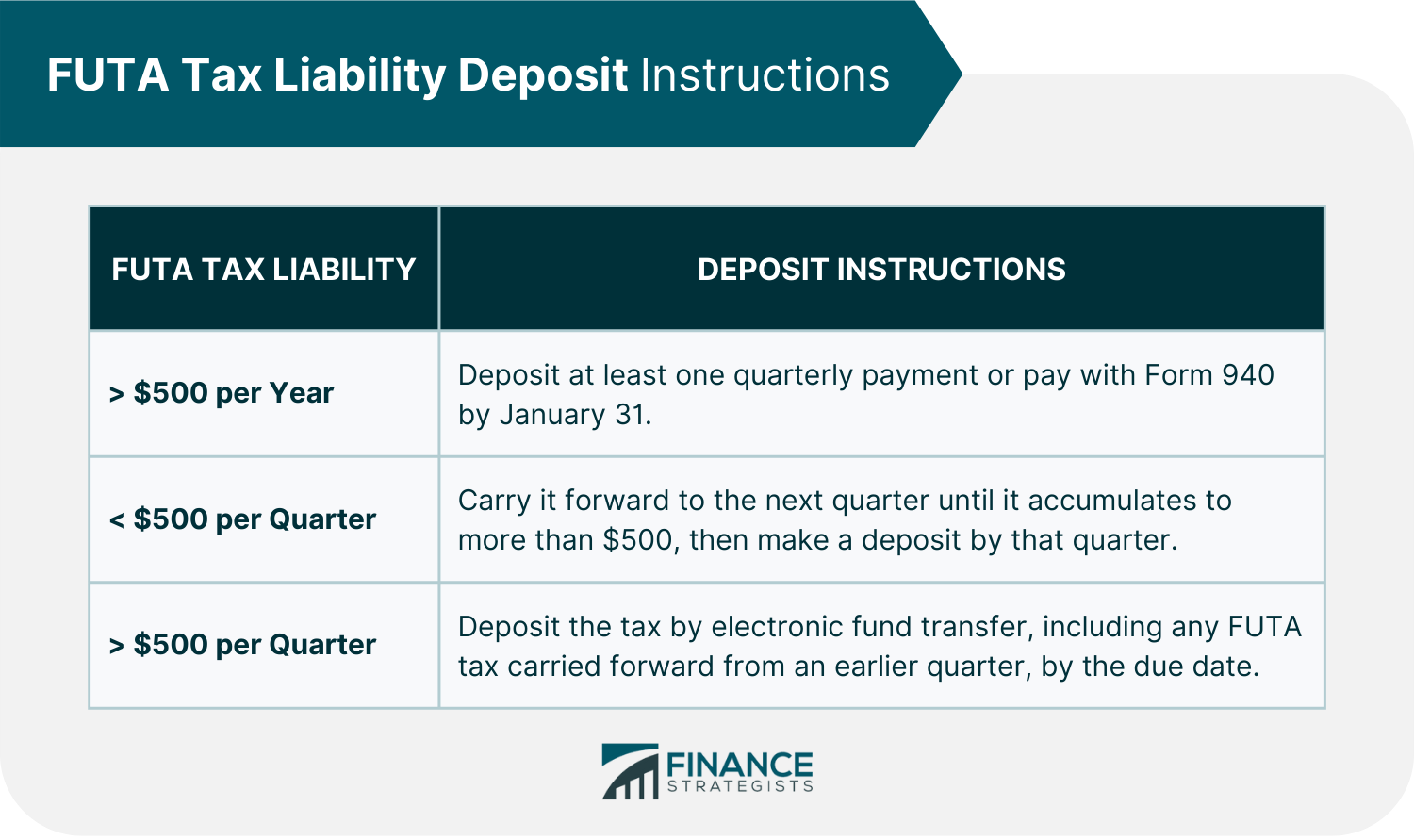

How to Deposit FUTA Tax

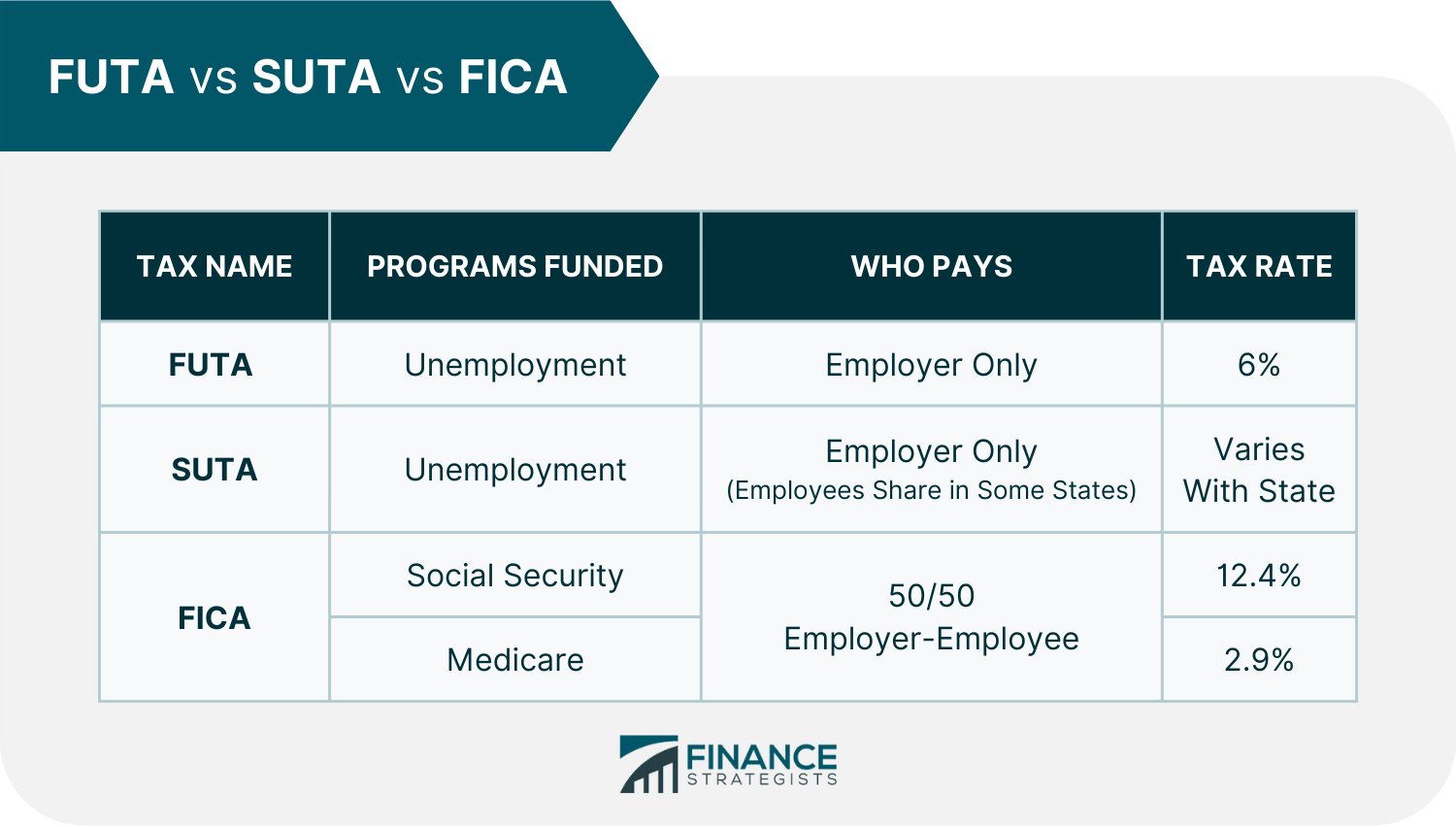

FUTA vs SUTA vs FICA

Final Thoughts

Federal Unemployment Tax Act (FUTA) FAQs

The FUTA tax rate for 2024 and 2025 is 6.0%.

Employers who paid $1,000 or more in compensation in any calendar quarter of the current or prior year are required to pay FUTA tax. You are also liable if you employed at least one person for a portion of each day throughout the course of 20 or more different weeks. Employers in households and agriculture are likewise covered by FUTA.

The FUTA tax is calculated as 6.0% of the first $7,000 of each employee's annual salary. Any amounts exceeding $7,000 are tax-exempt. A tax credit of 5.4% is applicable in certain conditions.

FUTA tax is paid exclusively by employers. Employees do not pay this tax or have it taken out of their paychecks. An organization exempt from federal income tax under section 501(c)(3) of the Internal Revenue Code is also exempt from federal unemployment tax. There can be no exception to this rule.

FUTA is the federal equivalent of the state taxes known as SUTA that are paid at the state level. The federal government oversees the state-run individual unemployment insurance systems through a fund that receives money from FUTA levies. A state may even borrow from FUTA funds to provide benefits for unemployed persons in their state when it is essential during periods of high unemployment.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.