Retirement debt management refers to the process of handling and reducing outstanding debts during the retirement phase of life. This typically involves a combination of strategies, such as budgeting, prioritizing debt repayment, and finding additional sources of income. Managing debt during retirement is crucial for maintaining financial stability and ensuring a comfortable lifestyle. As retirees generally rely on fixed or reduced incomes, any outstanding debts can significantly strain their financial resources and limit their ability to cover essential expenses. Debt can negatively impact retirees' quality of life by causing financial stress, limiting their ability to participate in leisure activities, and potentially leading to health problems. Managing and reducing debt is essential for retirees to enjoy their golden years without constant worry about their financial situation. Before entering retirement, it is essential to evaluate your current financial situation, including income sources, expenses, and outstanding debts. This assessment provides a clear picture of where you stand financially and informs the development of an effective debt management plan. Identifying all sources of income, such as Social Security benefits, pensions, and investments, is crucial for determining your financial resources during retirement. Understanding these income streams allows you to make informed decisions about managing your debt and maintaining your desired lifestyle. Evaluating your current expenses helps identify areas where you can cut costs and allocate more funds toward debt repayment. This assessment should include both essential and discretionary spending to ensure you maintain a balanced budget in retirement. Examining your outstanding debts, including interest rates and minimum payments, is essential for prioritizing which debts to pay off first. This analysis allows you to develop a strategic plan for reducing your overall debt burden before entering retirement. A retirement budget is a crucial tool for managing your finances and ensuring you can cover essential expenses while reducing debt. This budget should account for future expenses, and inflation, and prioritize necessary spending. Estimating your future expenses in retirement helps you create a realistic budget that accounts for changes in spending habits, such as increased healthcare costs or reduced discretionary spending. Accurate expense projections are critical for effective debt management and maintaining financial stability. Inflation erodes the purchasing power of money over time, which can impact your ability to cover expenses and repay debt. Adjusting your retirement budget for inflation helps ensure you maintain a realistic view of your future financial needs and can adapt your debt management strategies accordingly. Distinguishing between essential and discretionary expenses in your retirement budget helps you allocate resources effectively and prioritize debt repayment. This prioritization allows you to maintain a comfortable lifestyle while still focusing on reducing your debt burden. Creating a plan to reduce your debt before retirement is essential for entering this phase of life with financial stability. This plan should include strategies for paying off high-interest debt, consolidating debts, and saving and investing in reducing future debt. Paying off high-interest debt before retirement can significantly reduce your overall debt burden and save you money on interest payments. Strategies may include allocating extra funds toward these debts, refinancing, or utilizing balance transfer offers with lower interest rates. Consolidating multiple debts into a single loan with a lower interest rate can simplify debt management and reduce overall interest costs. This strategy may involve using a debt consolidation loan or a home equity loan to pay off existing debts, resulting in a single, more manageable monthly payment. Saving and investing money before retirement can help you build a financial cushion, reducing your reliance on debt during your golden years. By growing your savings and investments, you can ensure you have adequate funds to cover unexpected expenses without resorting to additional borrowing. Even during retirement, it's essential to continue focusing on debt reduction strategies. Prioritizing debt repayment based on interest rates, refinancing or renegotiating debt terms, and utilizing debt relief programs can all help you maintain financial stability and reduce your debt burden. Focusing on paying off debts with the highest interest rates first can save you money and accelerate your overall debt reduction. By prioritizing these high-interest debts, you can minimize the amount of interest paid and free up more funds to allocate toward other financial goals. Refinancing or renegotiating your debt terms may help you secure lower interest rates or extend repayment periods, making your debt more manageable during retirement. This strategy can reduce your monthly payments, freeing up more money for essential expenses or additional debt reduction. Debt relief programs, such as government-sponsored programs or nonprofit credit counseling services, can provide assistance and guidance for managing and reducing your debt during retirement. These programs may offer debt consolidation, repayment plans, or even debt forgiveness, depending on your circumstances. Balancing your income sources during retirement is critical for ensuring you have adequate funds to cover your expenses and continue reducing your debt. This may involve maximizing Social Security benefits, drawing from retirement savings accounts, and considering part-time work or passive income streams. Maximizing your Social Security benefits can provide you with additional income, helping to alleviate financial stress and support your debt reduction efforts. This may involve delaying your benefits to receive a larger monthly payment or coordinating benefits with your spouse to optimize your combined income. Strategically drawing from your retirement savings accounts, such as IRAs or 401(k)s, can provide you with additional income to cover expenses and repay debt. Careful planning is necessary to avoid unnecessary taxes, penalties, or prematurely depleting your retirement savings. Part-time work or passive income streams, such as rental income or royalties, can supplement your retirement income and support your debt reduction efforts. These additional income sources can help relieve financial pressure and provide greater flexibility in managing your finances during retirement. Adopting a frugal lifestyle during retirement can help you reduce discretionary spending, freeing up more funds for essential expenses and debt repayment. This may involve taking advantage of senior discounts, evaluating housing and transportation options, and cutting back on nonessential spending. Cutting back on discretionary spendings, such as dining out or travel, can help you save money and allocate more resources toward debt reduction. By reevaluating your spending habits and focusing on what's truly important, you can maintain financial stability during retirement. Many businesses offer senior discounts, which can help you save money on everyday purchases and services. Taking advantage of these discounts can reduce your overall expenses, making it easier to manage your budget and allocate funds toward debt repayment. Considering alternative housing and transportation options, such as downsizing your home or utilizing public transportation, can significantly reduce your expenses during retirement. By exploring these options, you can free up more funds for essential expenses and debt repayment, improving your overall financial situation. Establishing an emergency fund during retirement can help you avoid accumulating new debt by providing a financial cushion for unexpected expenses. A sufficient emergency fund can cover several months' worth of living expenses, reducing your reliance on credit cards or loans during financial emergencies. Effectively managing healthcare costs in retirement is essential for avoiding new debt and protecting your financial well-being. Exploring Medicare and supplemental insurance options, utilizing Health Savings Accounts (HSAs), and prioritizing preventive care and wellness can help you control healthcare expenses. Understanding your Medicare coverage and evaluating supplemental insurance options can help you select the most cost-effective plan to meet your healthcare needs. This ensures you're adequately covered while minimizing out-of-pocket costs, helping you avoid new debt related to medical expenses. Health Savings Accounts (HSAs) allow you to save pre-tax dollars for medical expenses, reducing your overall healthcare costs and helping you avoid new debt. Contributing to an HSA can provide you with additional funds to cover medical expenses not covered by Medicare or supplemental insurance plans. Focusing on preventive care and wellness can help you maintain good health, reducing the need for costly medical treatments and minimizing healthcare expenses. Engaging in regular exercise, eating a balanced diet, and scheduling routine medical checkups can help you stay healthy and avoid new debts related to healthcare costs. Preparing for potential long-term care expenses is crucial for avoiding new debt during retirement. This may involve evaluating long-term care insurance options and considering assisted living and nursing home costs. Long-term care insurance can help cover the costs of care in assisted living facilities, nursing homes, or home healthcare services. Evaluating your options and selecting a policy that meets your needs can provide financial protection and help you avoid new debt related to long-term care expenses. Understanding the potential costs of assisted living and nursing home care can help you plan for these expenses and avoid new debt. Researching facilities in your area, comparing costs, and considering alternative care options can help you make informed decisions about your long-term care needs. Effectively managing debt during retirement can lead to numerous benefits, including reduced financial stress, the ability to enjoy leisure activities, and an improved overall quality of life. By focusing on debt reduction, you can achieve greater financial security and peace of mind during your golden years. Proactively addressing debt challenges and developing a comprehensive plan for managing debt in retirement can help you achieve financial security and peace of mind. This allows you to focus on enjoying your retirement without constant worry about your financial situation. There are numerous resources and support options available for retirees facing debt challenges. These may include government programs, nonprofit credit counseling services, and educational resources, all aimed at helping you better manage and reduce your debt during retirement. Taking action to seek retirement planning services can greatly improve your financial situation and set you on a path toward debt-free retirement.What Is Retirement Debt Management?

Preparing for Retirement Debt Management

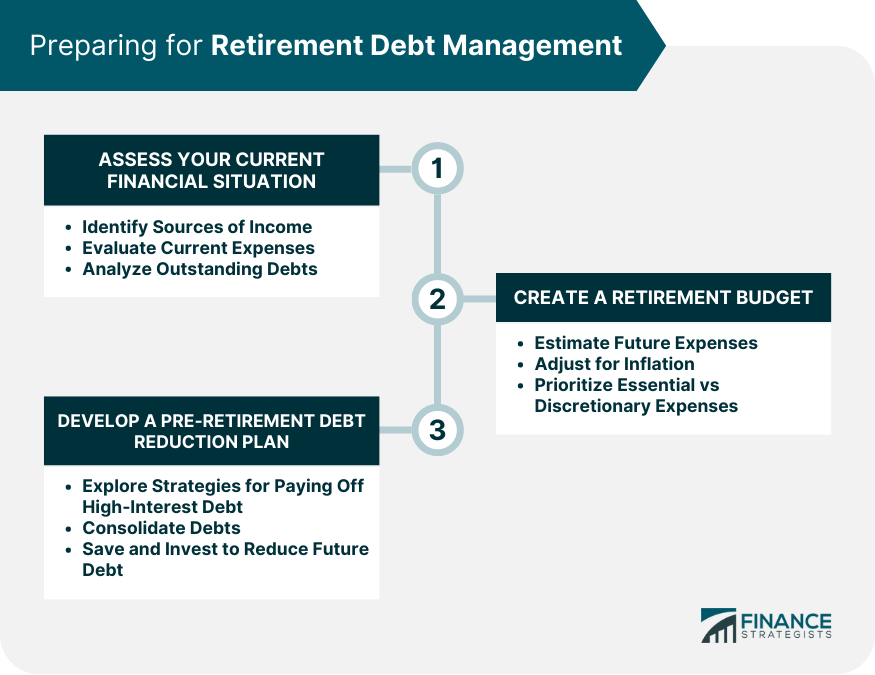

Assess Your Current Financial Situation

Identifying Sources of Income

Evaluating Current Expenses

Analyzing Outstanding Debts

Create a Retirement Budget

Estimating Future Expenses

Adjusting for Inflation

Prioritizing Essential vs Discretionary Expenses

Develop a Pre-retirement Debt Reduction Plan

Strategies for Paying Off High-Interest Debt

Consolidating Debts

Saving and Investing to Reduce Future Debt

Managing Debt During Retirement

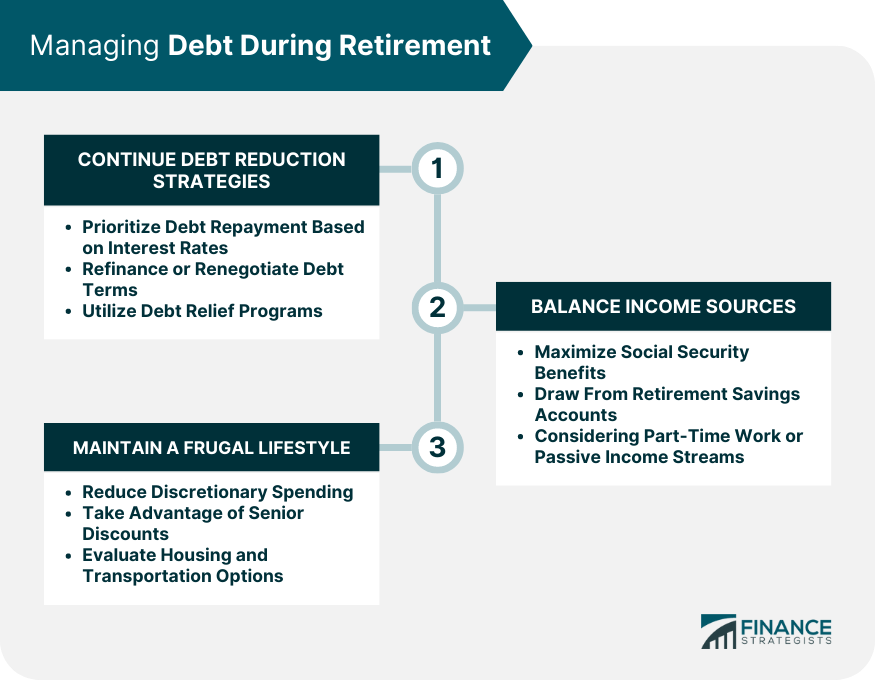

Continuing Debt Reduction Strategies

Prioritizing Debt Repayment Based on Interest Rates

Refinancing or Renegotiating Debt Terms

Utilizing Debt Relief Programs

Balancing Income Sources

Maximizing Social Security Benefits

Drawing from Retirement Savings Accounts

Considering Part-Time Work or Passive Income Streams

Maintaining a Frugal Lifestyle

Reducing Discretionary Spending

Taking Advantage of Senior Discounts

Evaluating Housing and Transportation Options

How to Avoid New Debt in Retirement

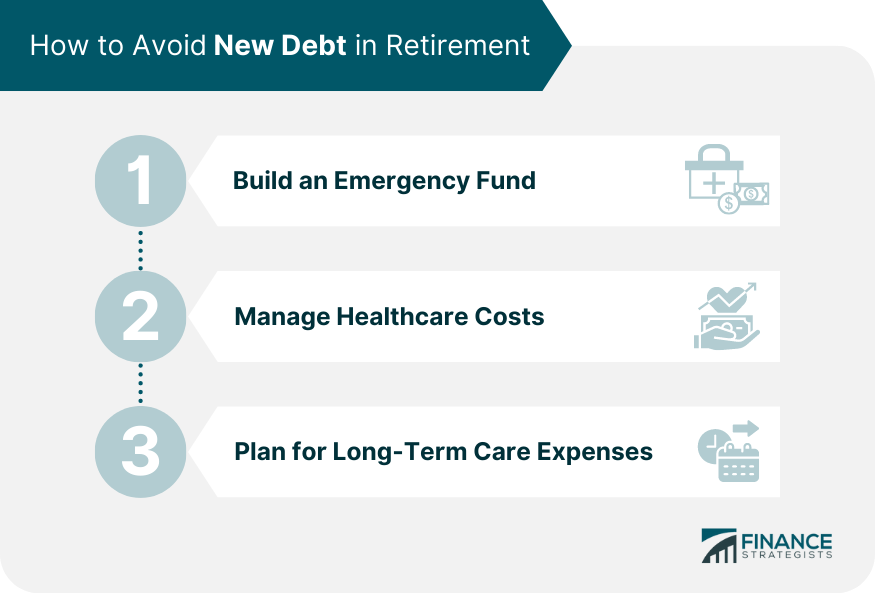

Build an Emergency Fund

Manage Healthcare Costs

Exploring Medicare and Supplemental Insurance Options

Utilizing Health Savings Accounts (HSAs)

Preventive Care and Wellness

Plan for Long-Term Care Expenses

Evaluating Long-Term Care Insurance Options

Considering Assisted Living and Nursing Home Costs

Final Thoughts

Retirement Debt Management FAQs

When creating a retirement budget that incorporates debt management, start by estimating future expenses, adjusting for inflation, and prioritizing essential vs. discretionary expenses. By carefully planning your retirement budgeting, you can allocate resources effectively and prioritize debt repayment.

Retirement budgeting can help you manage healthcare costs by allocating funds for Medicare and supplemental insurance premiums, contributing to Health Savings Accounts (HSAs), and setting aside money for preventive care and wellness. This helps you stay prepared for healthcare expenses and avoid new debt related to medical costs.

Retirement budgeting plays a crucial role in planning for long-term care expenses by helping you evaluate long-term care insurance options and consider potential assisted living and nursing home costs. By incorporating these expenses into your retirement budget, you can better prepare for the future and avoid new debt related to long-term care.

Using retirement budgeting to reduce debt during retirement involves creating a realistic budget that prioritizes debt repayment, adjusting for inflation, and managing your income sources to cover expenses while paying off debt. By maintaining a frugal lifestyle and focusing on essential expenses, retirement budgeting can help you achieve financial stability and reduce your overall debt burden.

Yes, retirement budgeting can help you avoid accumulating new debt by allocating funds for emergency savings, managing healthcare costs, and planning for long-term care expenses. By creating a comprehensive retirement budget and sticking to it, you can minimize the likelihood of incurring new debt and maintain greater financial stability during your retirement years.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.