An IUL is a type of permanent life insurance that is based on a stock market index. IULs allow people to invest directly into an equity index or a basket of stocks through the life insurance policy that they bought from the company. When you buy a policy, you’re covered for the rest of your life. IULs are considered permanent because you can keep the policy until you die or surrender it. When you die, your beneficiaries will receive the death benefit. IULs have no penalties for making early withdrawals and the cash value within the IUL policy grows tax-deferred. IUL is different from fixed universal life insurance (FUL) and variable universal life insurance (VUL). IUL is not based on the premium amount that you pay, the premiums for IUL are guaranteed. Have questions about Indexed Universal Life and 401(k)s? Click here. 401(k) stands for Section 401 of the Internal Revenue Code, which governs employer-sponsored retirement plans in the United States. It is a retirement savings plan that allows employees to save money for retirement. The money contributed to a 401(k) is not taxed until it is withdrawn. Employers can match a portion of employee contributions. 401(k) plans are available to employees of companies with more than 50 employees. Employees of smaller companies may be able to participate in a similar plan called a 403(b). The money in a 401(k) can be invested in stocks, bonds, and mutual funds. When you buy an IUL policy, you’re covered for the rest of your life. The IUL is a tax-advantaged investment product that offers a death benefit. IULs allow you to invest in the stock market without having to worry about losing your entire investment if the value of your portfolio drops. IUL gains are not taxed since they grow within the life insurance policy. You don’t have to worry about making early withdrawals from IUL policies. IULs also offer cash value growth that is tax-deferred. This means that you don’t have to pay taxes on any of the growth in your IUL policy until you withdraw the money. IULs are not subject to required minimum distributions (RMDs). It also offers an additional cash value that can be borrowed if you’d like to use the money for other expenses. When you contribute to a 401(k), your contributions are not taxed. That means that you don’t have to pay taxes on the money until you withdraw it from the account. Employers often match a portion of employee contributions, which can help employees save more for retirement. You can contribute to your 401(k) through payroll deductions or automatic transfers from your bank account. Your retirement savings grow tax-deferred until you withdraw the money. You can invest your 401(k) in stocks, bonds, mutual funds, ETFs, and money market funds. IUL and 401(k) offer a variety of investment options, including stocks, bonds, and mutual funds. IULs and 401(k) plans often offer low-cost investments (like index funds), which can help your money grow faster. Both IULs and 401(k)s are tax-deferred investments, meaning the money invested in them does not have to be paid taxes on the gains until it is withdrawn. This allows both to grow at a faster rate than if the money was taxed as it was earned. Both IULs and 401(k)s are available to employers with more than 50 employees. IUL policies are also available to employees of smaller companies through a similar plan called a 403(b). Many employers offer a matching contribution to their employees' 401(k) plan. This means that the employer will match a certain percentage of what the employee contributes to the account. IUL policies do not offer a matching contribution. IULs are not subject to required minimum distributions (RMDs). This means that you don’t have to take money out of your IUL policy each year, regardless of how old you are. 401(k)s are subject to RMDs, which require account holders to withdraw a certain amount of money from their account each year. IUL policies offer a death benefit while 401(k) plans do not. IUL policies also come with an additional cash value that IUL account holders can borrow against if they would like to use the money for other expenditures. The answer to this question largely depends on the individual. IULs and 401(k)s offer many of the same benefits, and each has its own unique advantages. It’s important to consider your needs and goals when deciding which is better for you. If you are looking for a death benefit or want tax-advantaged growth, IULs are a great option. IUL policies offer cash value growth, which is tax-deferred until account holders withdraw the money. IUL policies also come with an additional cash value that can be borrowed against in case you need to use the money for other expenses. If you want more investment options or contribute to your retirement plan through payroll deductions, 401(k)s are a better choice. Employers often match a portion of employee contributions, which can help employees save more for retirement. 401(k) account holders can also invest in stocks, bonds, mutual funds, ETFs, and money market funds. Whichever option you choose, it’s important to start saving for retirement as soon as possible. The earlier you save, the more time your money has to grow. IULs and 401(k)s are both excellent options for retirement savings. IULs offer a death benefit, while 401(k)s do not. IUL policies come with an additional cash value that can be borrowed against if you need the money for other expenses. 401(k)s offer more investment options than IULs, and employers often match a portion of employee contributions. It’s important to consider your needs and goals when deciding which is better for you. Start saving for retirement as soon as possible – the earlier you save, the more time your money has to grow.What Is an IUL?

What Is 401(k)?

How Does IUL Work?

How Does 401(k) Work?

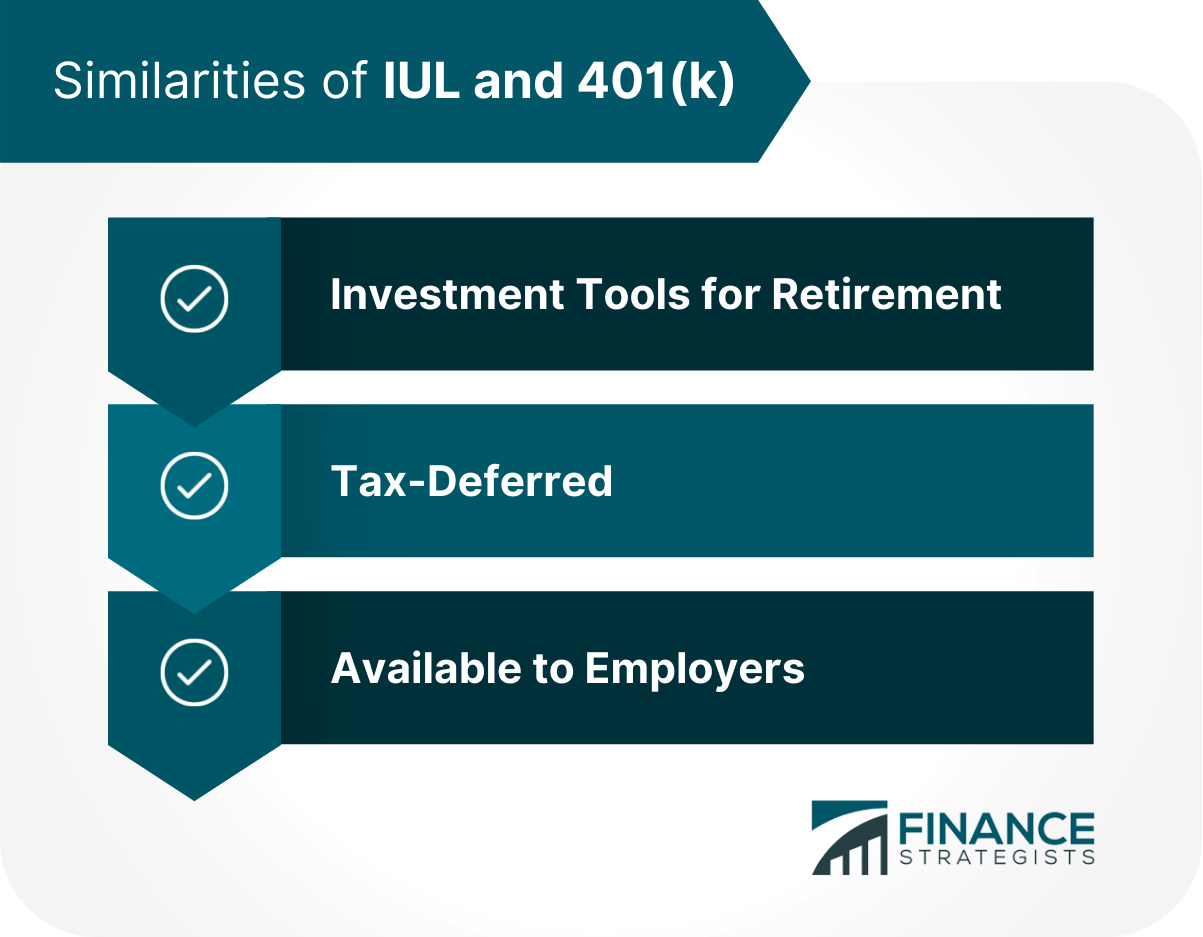

Similarities IUL and 401(k)

Investment Tools for Retirement

Tax-Deferred

Available to Employers

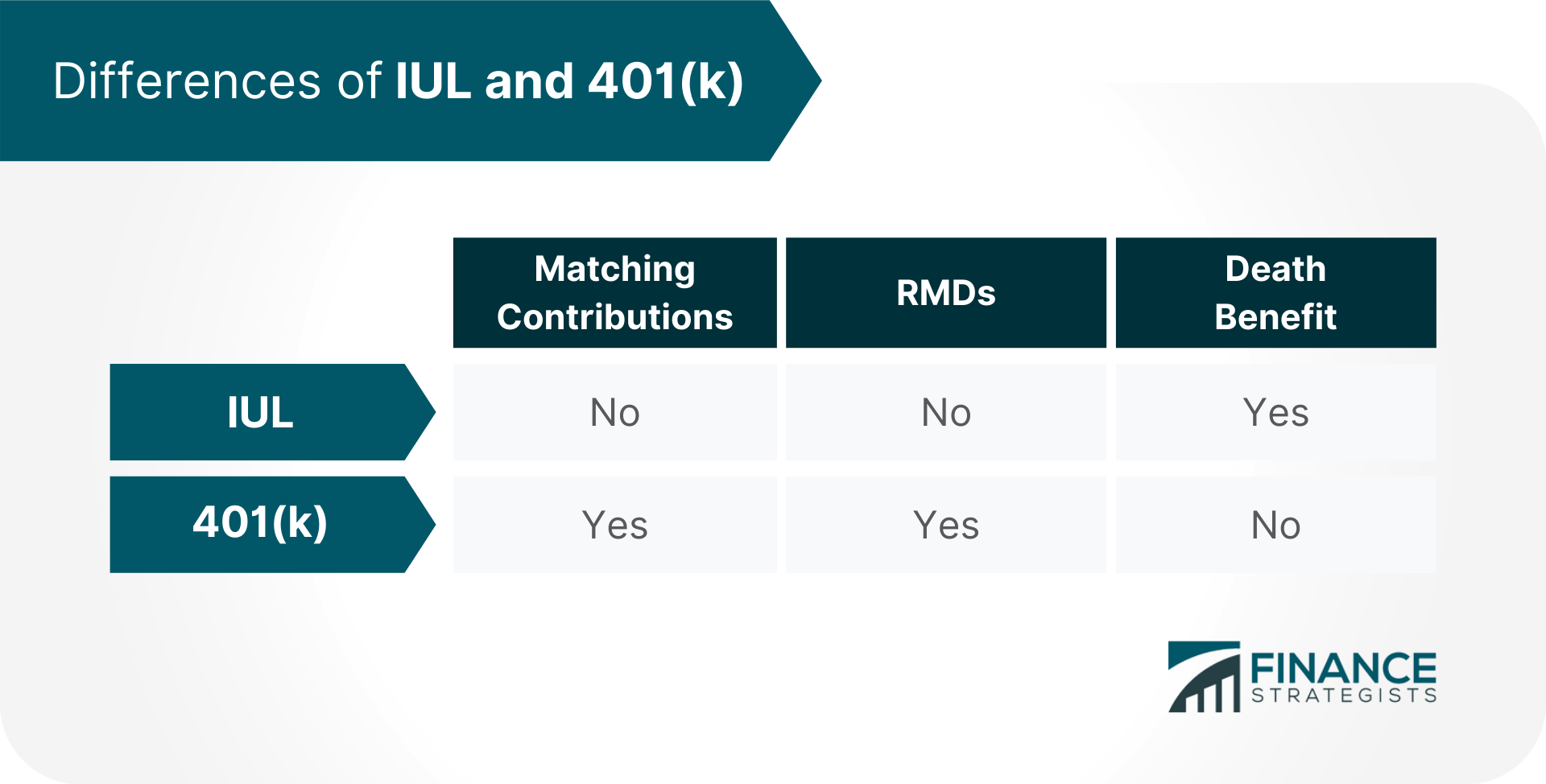

Differences IUL and 401(k)

Matching Contributions

RMDs

Death Benefit

Which Is Better?

IULs

401(k)

Key Takeaways

IUL vs 401(k) FAQs

IUL stands for Index Universal Life. IULs are hybrid life insurance policies with investment accounts.

A 401(k) is a type of retirement savings account that allows employees to contribute pre-tax income to the account. Employers often match a portion of employee contributions.

IULs provide IUL account holders with a death benefit. It also comes with an additional cash value that IUL account holders can borrow against if they would like to use the money for other expenditures.

A 401(k) is a type of retirement savings account that allows employees to contribute pre-tax income to the account. Employers often match a portion of employee contributions.

IUL policies and 401(k)s both offer tax-advantaged growth on contributions. Both can also be a tool to prepare for retirement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.