Sales concessions refer to incentives or inducements offered by property sellers to attract buyers and encourage them to complete a purchase. These concessions can come in various forms, including non-realty items and financing concessions. The aim of sales concessions is often to make a property more appealing, to achieve a quicker sale, or to negotiate with a potential buyer who might be on the fence. However, it's important to note that sales concessions can impact the actual perceived value of the property, especially when it comes to appraisals and loan underwriting. Traditionally, when thinking about real estate transactions, it's properties, land, and fixed structures that come to mind. However, sales concessions venture away from these norms. These concessions, often added as sweeteners to seal a deal, are not typically part of the realty. Instead, they diverge to offer more than just brick and mortar. Cash, the universal pleaser. It's not uncommon for sellers to offer cash incentives as a part of the sales deal. This cash can be directed towards closing costs, repairs, or even as a straightforward discount. It's a clear, tangible benefit that most buyers find hard to resist. While a home is an emotional purchase, finances are very much at its heart. Cash incentives speak directly to this, offering a monetary advantage that can make all the difference in a buyer's decision. Walking into a staged home, it's easy to fall in love with a stylish sofa or a chic dining set. Some sellers tap into this appeal, offering furniture as a part of the sales concession. This not only adds value but also reduces the hassle for buyers who may be dreading the move. For a buyer, the prospect of a ready-furnished home is appealing. It saves time, reduces moving expenses, and ensures that the house looks as great in reality as it did during the viewing. Believe it or not, cars, boats, or even motorcycles have been known to be included in real estate deals. They're high-value items that can seal deals, especially in luxury property markets or unique circumstances. An automobile thrown into a deal is more than just a vehicle; it's a statement. It symbolizes luxury, extravagance, and a deal that's a little out of the ordinary. Giving a home a personal touch is important for new homeowners. Sellers sometimes offer decorator allowances to entice buyers. This is essentially a budget set aside for decorating, allowing buyers to customize their new home to their liking. Personalization is a powerful draw. A decorator allowance not only provides financial relief but also an emotional connection, allowing buyers to envision their life in the new space. The process of moving can be daunting. By offering to cover moving costs, sellers can provide a significant boost in the deal's attractiveness. It's a practical and often appreciated gesture that can sway buyers who are weighing the logistical challenges of moving. From packing to transportation, moving is multifaceted. Alleviating this burden can act as a strong incentive for buyers on the verge of making a decision. From free lawn maintenance to gym memberships, the world of sales concessions is vast. These additional giveaways, although not always significant in monetary terms, can add unique flavor to a deal, making it stand out in a crowded market. Every buyer is different. Sometimes, it's these unconventional giveaways that resonate most, offering something unique that meets an unexpected desire or need. Financing concessions relate to the terms of a mortgage or loan. They can include reduced interest rates, waived fees, or even adjustments in loan duration. They're not physical or tangible like a sofa or a car but can be equally impactful, if not more. Navigating the financing landscape can be daunting. Concessions in this domain directly address the financial apprehensions of buyers, providing them with terms that can ease their long-term monetary commitments. There are industry standards and limits set by entities like Fannie Mae regarding financing concessions. However, in some scenarios, the concessions offered can exceed these predefined limits, making the deal even sweeter for the buyer. Pushing boundaries has its allure. By offering terms that surpass established norms, sellers can present buyers with opportunities that are both rare and enticing. Sales concessions, while beneficial to the buyer, have a direct impact on the overall value of the property. The value of these concessions is often deducted from the sales price, essentially decreasing the home's recorded selling price. This lowered valuation might seem detrimental, but it's a calculated move. It balances the immediate incentives provided to the buyer against the long-term value representation of the property. The Loan-to-Value ratio, a critical metric in real estate financing, is affected by sales concessions. When concessions are provided, they influence the home's final sale price, which, in turn, impacts the LTV ratio — a key figure lenders consider when approving a mortgage. The math behind mortgage approvals is intricate. Every component, including sales concessions, plays a pivotal role in shaping the final picture. Beyond the standard LTV, there's the combined LTV, which factors in additional loans on the property. Sales concessions can influence this combined figure, further complicating the valuation and financing landscape. The financial intricacies of real estate aren't always straightforward. As sales concessions are thrown into the mix, the calculations and their implications become even more multifaceted. At the heart of any lending process lies risk assessment. Sales concessions introduce a variable that underwriters must consider when evaluating the risk associated with a particular mortgage. These concessions can skew the traditional valuation methods, making risk assessment a more intricate task. Diving into the world of underwriting is like piecing together a jigsaw puzzle. Every element, sales concessions included, influences the broader risk landscape. Integrity in property valuation is paramount. Underwriters are the gatekeepers ensuring that the property's recorded value isn't inflated due to generous sales concessions. They sift through the extras to arrive at a genuine valuation, ensuring the lending institution's interests are protected. Behind every property transaction lies a story. By ensuring transparent valuations, underwriters are pivotal in penning tales that stand the test of time. At the end of the day, lending institutions are in the business of risk and reward. They need to protect their interests, and understanding sales concessions is pivotal to this. By dissecting and understanding the implications of these concessions, underwriters safeguard the lenders' investments. It's a delicate balance. While sales concessions can be enticing for buyers, they bring with them nuances that need careful consideration to protect everyone involved in the lending process. Mortgage eligibility often hinges on this ratio, and sales concessions directly influence it. A higher concession might lead to a higher LTV ratio, which could affect a buyer's mortgage terms. When numbers dance, outcomes can shift. The interplay between sales concessions and LTV ratios is a delicate waltz that shapes the contours of mortgage approvals. Another vital metric is the debt-to-income (DTI) ratio, which assesses a buyer's ability to manage monthly payments. Sales concessions can indirectly influence this ratio by altering the effective purchase price or through financing concessions. The financial health of a buyer isn't solely determined by their income or savings. The DTI ratio, influenced by elements like sales concessions, is a testament to this. Sales concessions can sometimes lead to scenarios where mortgage insurance becomes necessary. This insurance, while an added cost, protects lenders if a buyer defaults. The presence or absence of concessions can shape the need for such insurance. Mortgage insurance might seem like just another item on a checklist. Yet, its implications, especially in the realm of sales concessions, run deep, impacting both buyers and lenders. Different lenders have different appetites for risk. As such, they might have specific limits on the sales concessions they're willing to accept. These limits ensure that the lending institution isn't overly exposed to risk due to inflated property values or generous concessions. In the vast ocean of real estate financing, each lender charts its course. Sales concession limits are one of the compasses they use. The type of loan a buyer opts for can also dictate the acceptable sales concessions. For instance, a conventional loan might have different concession thresholds compared to an FHA or VA loan. It's not just about numbers. The very nature of a loan, influenced by sales concessions, can change the game for potential homeowners. Real estate, at its heart, is influenced by market dynamics. In hot markets, sales concessions might be sparse, while in buyer-favored markets, they might be generous. However, these market dynamics can also introduce restrictions on acceptable sales concessions. The market's ebb and flow sculpt the landscape of sales concessions. As trends shift and tides turn, the role and acceptability of these concessions evolve. The allure of added incentives can speed up the sale process. Sellers, by offering attractive sales concessions, can entice buyers to make quicker decisions, reducing the time a property lingers on the market. Time is of the essence. In real estate, this adage takes on a whole new meaning, with sales concessions acting as catalysts. In a market saturated with options, standing out is crucial. Sales concessions can provide that edge, making a property more appealing compared to others that might not offer such perks. In the vast sea of listings, sales concessions are the beacon, drawing buyers with their allure. By offering sales concessions, sellers can maintain a higher listing price while still providing value to potential buyers. This flexibility can be instrumental in negotiations, providing a win-win for both parties. Pricing isn't just about numbers. It's a dance, and sales concessions add rhythm to it. Sellers can sometimes list their property at a higher price, knowing that they'll be offering sales concessions. This strategy can attract a broader range of buyers, especially if they see the inherent value in the concessions provided. A listing price is more than just a figure. It's a statement, and with sales concessions in the mix, it resonates louder. Sales concessions can significantly reduce the financial burden buyers face when purchasing a property. From cash discounts to covered moving costs, these concessions ease the initial monetary strain. Every penny counts. Sales concessions acknowledge this, cushioning the financial leap buyers take when purchasing property. Beyond financial relief, sales concessions bring added value to the table. Whether it's a state-of-the-art appliance suite or a year's worth of lawn maintenance, buyers get more bang for their buck. It's not just about square footage or location. The value, enhanced by sales concessions, delves deeper, enriching the very essence of homeownership. Financing concessions can provide buyers with better mortgage terms, lower interest rates, or waived fees. This flexibility can make the long-term commitment of a mortgage more palatable. Beyond the immediate appeal of a property lies the intricate world of financing. Sales concessions shed light on this path, offering a smoother journey. Moving is more than just logistics; it's an emotional journey. Sales concessions like decorator allowances or covered moving costs can make this transition smoother, reducing both stress and expenses. A new home is a new chapter. Sales concessions ensure it starts on a positive note. One of the potential pitfalls of sales concessions is the risk of inflating a property's value. While these concessions offer immediate appeal, they can sometimes mask the real value of the property, leading to potential long-term financial implications for the buyer. Real estate is a long game. While immediate perks are enticing, the true value of a property stands the test of time. Generous sales concessions can sometimes complicate the mortgage approval process. They can influence critical metrics like LTV and DTI ratios, potentially impacting the terms of the loan or even its approval. Behind every mortgage approval is a maze of numbers and terms. Sales concessions introduce twists and turns that both buyers and lenders must navigate. For sellers, offering generous sales concessions might expedite the sale, but it can also reduce the net profit from the sale. It's a balancing act, weighing the immediate benefit of a quicker sale against potential reduced earnings. In the real estate equation, profit is pivotal. While sales concessions can be instrumental in closing deals, their impact on the bottom line cannot be overlooked. For buyers, the allure of sales concessions can sometimes cloud judgment. They might be swayed by the immediate perks, only to later realize that the property might not have been the perfect fit, leading to buyer’s remorse. Real estate decisions are monumental. While sales concessions dazzle, they should complement, not overshadow, the core value of a property. Sales concessions, comprising various incentives and inducements offered by sellers, play a pivotal role in the real estate landscape. Aimed at enhancing the appeal of a property, they can expedite sales, offer monetary advantages, and address specific buyer needs, from tangible offerings like furniture and vehicles to intangible ones like financing terms. However, while they present numerous benefits for both sellers, like faster sales and competitive edges, and buyers, such as reduced costs and added value, they're not devoid of complexities. Sales concessions can influence property valuations, complicating mortgage underwriting and potentially impacting loan approvals. Moreover, they may lead to inflated property values or spark buyer's remorse, emphasizing the need for judicious considerations. In sum, while sales concessions can be powerful tools in the real estate domain, both sellers and buyers must weigh their benefits against potential pitfalls to ensure informed decision-making.Definition of Sales Concessions

Understanding the Various Forms of Sales Concessions

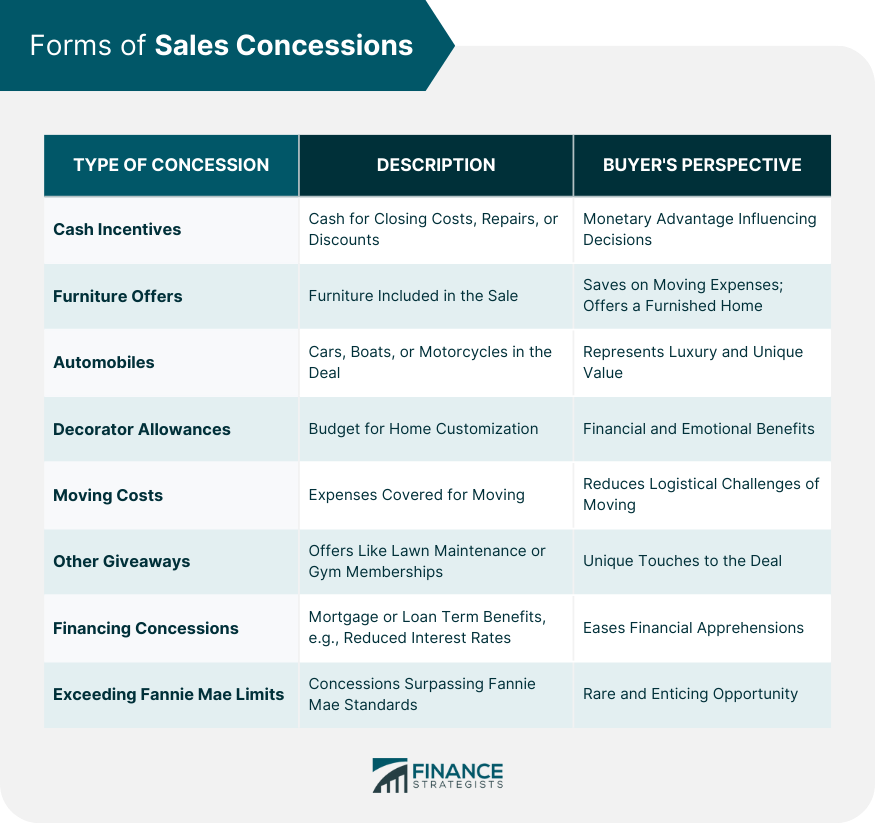

Non-Realty Items

Cash Incentives

Furniture Offers

Automobiles

Decorator Allowances

Moving Costs

Other Giveaways

Financing Concessions

Defining Financing Concessions

Exceeding Fannie Mae Limits

Impact of Sales Concessions on Property Valuation

Deducting Value From Sales Price

Implications on Loan-To-Value (LTV) Ratios

Calculating LTV With Concessions

Combined LTV Ratios

Implications of Sales Concessions for Underwriting and Eligibility

Why Underwriters Pay Attention to Sales Concessions

Risk Evaluation

Honest Valuation

Lender Interests Protection

How Concessions Influence Mortgage Eligibility

Loan-To-Value Ratios

Debt-To-Income Ratios

Mortgage Insurance Implications

Concession Limits and Restrictions

Lender-Specific Limits

Impact on Loan Types

Market-Based Restrictions

Pros and Cons of Offering and Accepting Sales Concessions

Benefits for Sellers

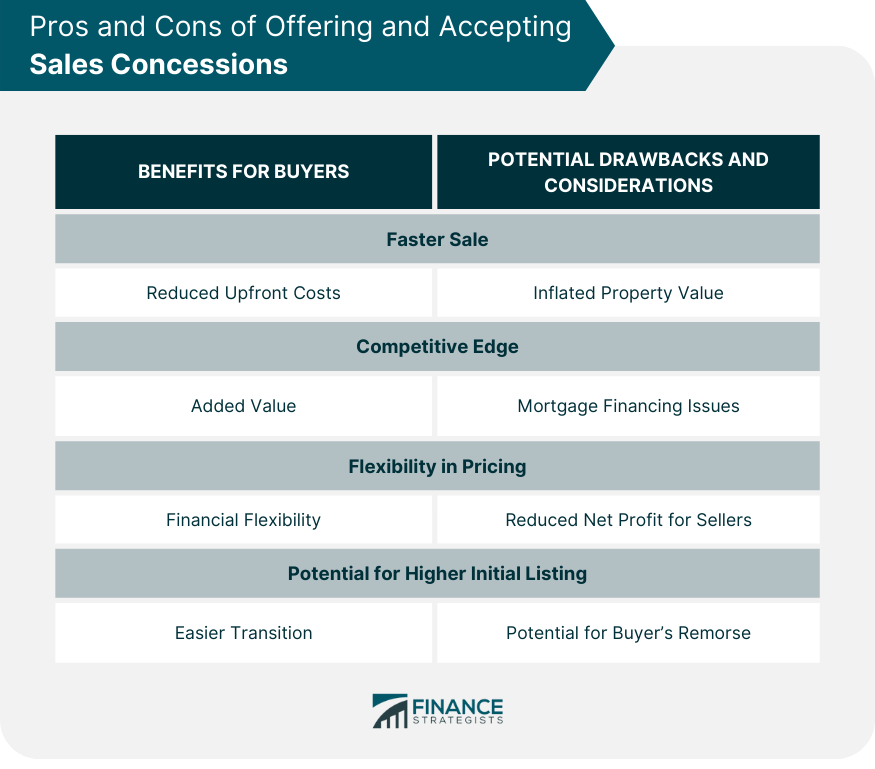

Faster Sale

Competitive Edge

Flexibility in Pricing

Potential for Higher Initial Listing

Benefits for Buyers

Reduced Upfront Costs

Added Value

Financial Flexibility

Easier Transition

Potential Drawbacks and Considerations

Inflated Property Value

Mortgage Financing Issues

Reduced Net Profit for Sellers

Potential for Buyer’s Remorse

Final Thoughts

Sales Concessions FAQs

Sales concessions are incentives or inducements offered by sellers, often in the form of non-realty items or financing terms, to encourage potential buyers to purchase a property.

Sales concessions can influence the perceived value of a property. They may require adjustments in the valuation, especially when considering loan-to-value (LTV) ratios.

Underwriters assess sales concessions to ensure honest property valuation, evaluate risks, and protect lender interests in the mortgage process.

Buyers can enjoy reduced upfront costs, added value, financial flexibility, and an easier transition into their new home through sales concessions.

Yes, they can lead to inflated property values, mortgage financing issues, reduced net profit for sellers, and potential buyer's remorse.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.