A Waiver of Coinsurance Clause is a provision in certain insurance policies that eliminates or reduces the policyholder's coinsurance obligation for covered claims, thereby potentially minimizing their out-of-pocket expenses during the claims process. This clause is typically activated when the policyholder meets specific conditions outlined in the policy, such as maintaining adequate coverage levels or implementing effective risk management strategies. Coinsurance is a term used in insurance policies to describe a cost-sharing mechanism between the policyholder and the insurance company. It is typically expressed as a percentage and indicates the portion of a claim that the policyholder is responsible for, while the insurance company covers the remaining amount. Coinsurance encourages policyholders to maintain appropriate coverage limits and share the risk with the insurance company, which can help keep insurance premiums more affordable. To calculate the coinsurance amount, policyholders multiply the claim amount by the coinsurance percentage. For example, if a policy has a coinsurance of 80%, the policyholder would be responsible for 20% of the claim. If the claim amount were $10,000, the policyholder would pay $2,000, and the insurance company would cover the remaining $8,000. Coinsurance can have significant financial implications for policyholders. If a policyholder underestimates the value of their property or fails to maintain adequate coverage limits, they may face higher out-of-pocket expenses when a claim is filed. On the other hand, if policyholders maintain appropriate coverage levels and understand their coinsurance obligations, they can better manage their risk and reduce their financial burden during the claims process. The waiver of coinsurance clause is a provision found in some insurance policies that eliminate the coinsurance requirement for policyholders, either partially or entirely. When this clause is triggered, the policyholder is not required to pay their portion of the coinsurance for a covered claim. Instead, the insurance company covers the full claim amount up to the policy limits. Waiver of coinsurance clauses is often implemented in situations where the policyholder has met specific conditions outlined in the policy. These conditions may include maintaining a specific coverage level, having a loss prevention program in place, or meeting other risk management requirements. The clause can be especially beneficial for policyholders facing large claims, as it can significantly reduce their financial burden. The primary benefit of a waiver of coinsurance clause for policyholders is the potential for reduced out-of-pocket expenses during the claims process. By eliminating or reducing the coinsurance obligation, policyholders can better manage their financial risk and protect their assets. Additionally, the clause can serve as an incentive for policyholders to maintain adequate coverage levels and implement effective risk management strategies. Insurance brokers play a crucial role in helping policyholders understand and take advantage of waiver of coinsurance clauses. Brokers must stay informed about the availability of these clauses in various policies and educate their clients on the potential benefits. By identifying policies with a waiver of coinsurance clauses, brokers can help their clients make more informed decisions about their insurance coverage and minimize their financial risk. One of the primary responsibilities of insurance brokers is to help their clients understand the complexities of their policies, including waiver of coinsurance clauses. Brokers should explain the purpose of the clause, how it works, and the specific conditions that must be met to trigger its benefits. Additionally, brokers should provide guidance on how clients can maintain compliance with these conditions and offer recommendations for risk management strategies that can help them qualify for the waiver of coinsurance clause. Insurance brokers also act as advocates for their clients, working with insurance companies to negotiate policy terms that best meet their clients' needs. This may include negotiating the inclusion of a waiver of coinsurance clause or ensuring that the conditions for its implementation are reasonable and achievable. By advocating for their clients, brokers can help policyholders obtain more favorable policy terms and maximize their potential benefits. In property insurance, waiver of coinsurance clauses can be particularly beneficial for policyholders who own high-value assets or properties. By including this clause in their policy, property owners can ensure that they are adequately protected in the event of a significant loss, without the burden of coinsurance. Insurance brokers should work closely with their clients to identify suitable property insurance policies that include waiver of coinsurance clauses and help them meet the necessary conditions for its activation. Waiver of coinsurance clauses can also be found in some health insurance policies, particularly those with high deductibles or out-of-pocket maximums. In these cases, the clause can help reduce the policyholder's financial burden when faced with significant medical expenses. Insurance brokers specializing in health insurance should educate their clients on the benefits of waiver of coinsurance clauses and guide them in selecting appropriate policies that include this provision. Business interruption insurance policies often include waiver of coinsurance clauses to help business owners minimize their financial risk during periods of unexpected disruption. These clauses can be especially valuable for small business owners who may struggle to absorb the costs associated with a temporary shutdown or loss of income. Insurance brokers working with business clients should prioritize policies with a waiver of coinsurance clauses and assist clients in meeting the necessary requirements for its implementation. Insurance brokers must be aware of state-specific regulations and laws that govern the use of waiver of coinsurance clauses. These regulations can vary significantly between states, with some states imposing strict requirements on the inclusion of these clauses in insurance policies. Brokers should stay up-to-date on the regulatory landscape in their state and ensure that they are providing accurate and compliant advice to their clients. In addition to state-specific regulations, insurance brokers should also follow industry best practices and guidelines when advising clients on waiver of coinsurance clauses. These best practices may include recommendations on coverage levels, risk management strategies, and other factors that can impact the activation of the waiver of coinsurance clause. By adhering to these guidelines, brokers can help their clients maximize their potential benefits while maintaining compliance with industry standards. Insurance brokers must maintain strict compliance with all relevant regulations and requirements related to the waiver of coinsurance clauses. This includes obtaining the necessary licenses and certifications, adhering to state-specific regulations, and following industry best practices. Failure to comply with these requirements can result in penalties, fines, or even the revocation of the broker's license. The Waiver of Coinsurance Clause is a valuable provision found in certain insurance policies that can significantly benefit policyholders. By eliminating or reducing the coinsurance obligation, policyholders can minimize their out-of-pocket expenses during the claims process. This clause is typically activated when specific conditions outlined in the policy are met, such as maintaining adequate coverage levels or implementing effective risk management strategies. Insurance brokers play a crucial role in identifying policies with waiver of coinsurance clauses, educating clients on the benefits, and negotiating favorable policy terms. The application of this clause can vary across different types of insurance. Property insurance benefits high-value asset owners, health insurance helps reduce financial burden for significant medical expenses, and business interruption insurance aids business owners during unexpected disruptions. Insurance brokers should also consider legal and regulatory considerations, including state-specific regulations and industry best practices, to ensure compliance and provide accurate advice to their clients.Overview of Waiver of Coinsurance Clause

Basics of Coinsurance

Definition and Purpose

Coinsurance Calculation

Implications for Policyholders

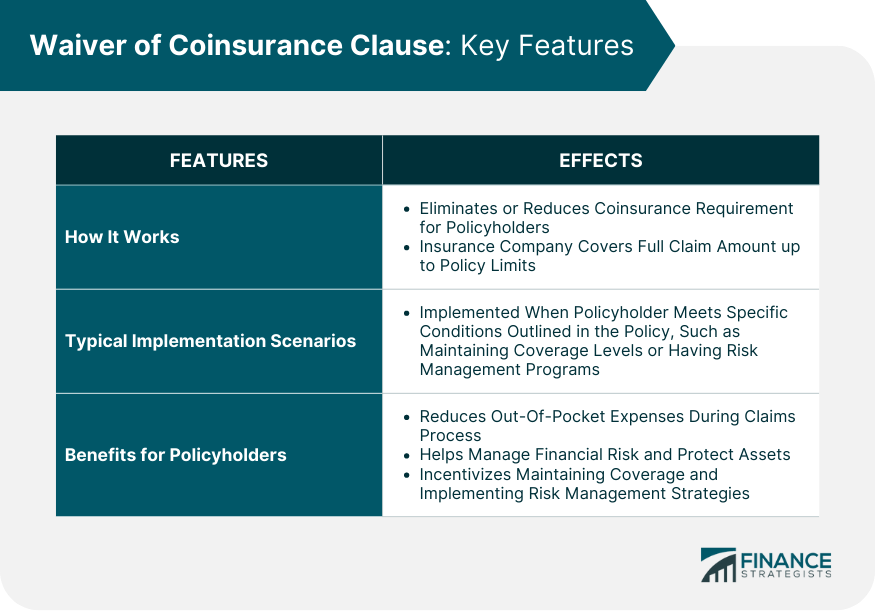

Waiver of Coinsurance Clause: Key Features

How the Clause Works

Typical Scenarios for Implementation

Benefits for Policyholders

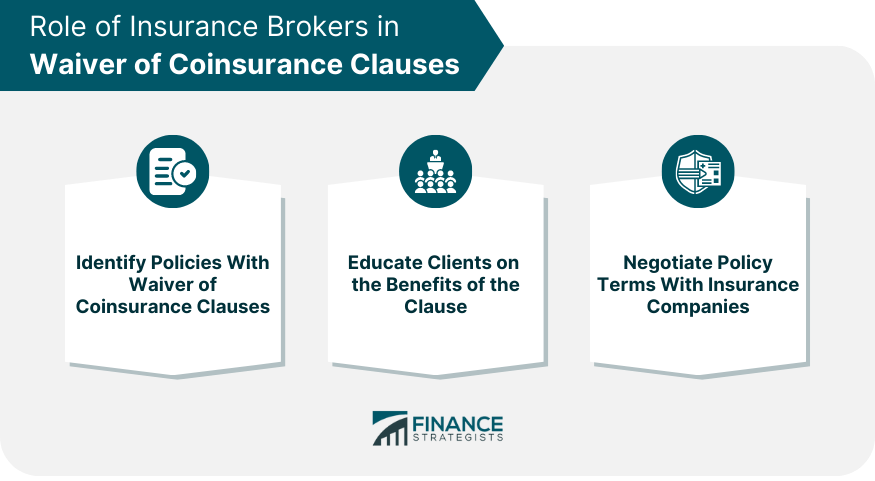

Role of Insurance Brokers in Waiver of Coinsurance Clauses

Identifying Policies With Waiver of Coinsurance Clauses

Educating Clients on the Benefits of the Clause

Negotiating Policy Terms With Insurance Companies

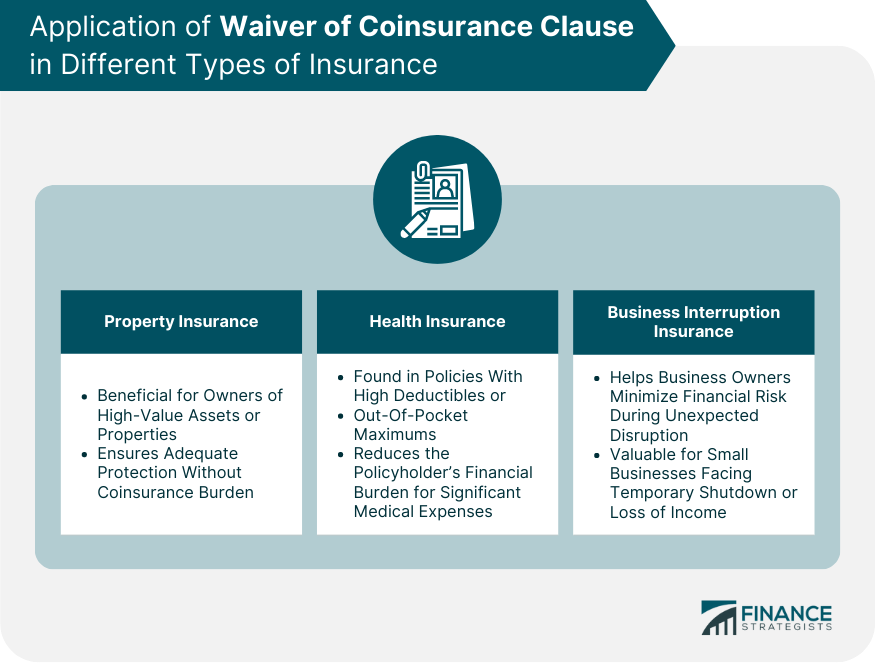

Application of Waiver of Coinsurance Clause in Different Types of Insurance

Property Insurance

Health Insurance

Business Interruption Insurance

Legal and Regulatory Considerations

State-Specific Regulations and Laws

Industry Best Practices and Guidelines

Compliance Requirements for Insurance Brokers

Conclusion

Waiver of Coinsurance Clause FAQs

A Waiver of Coinsurance Clause is a provision in certain insurance policies that eliminates or reduces the policyholder's coinsurance obligation for covered claims. This clause can benefit policyholders by potentially reducing their out-of-pocket expenses during the claims process and encouraging them to maintain adequate coverage levels.

Insurance brokers can help their clients take advantage of Waiver of Coinsurance Clauses by identifying policies with these clauses, educating clients about the benefits and conditions associated with the clause, and negotiating policy terms with insurance companies to ensure the clause is included and reasonable.

Waiver of Coinsurance Clauses can be found in various types of insurance policies, such as property insurance, health insurance, and business interruption insurance. These clauses can be particularly beneficial for policyholders who own high-value assets, face significant medical expenses, or experience business disruptions.

Insurance brokers need to be aware of state-specific regulations and laws governing Waiver of Coinsurance Clauses, as well as industry best practices and guidelines. Additionally, brokers must maintain compliance with all relevant requirements, including obtaining necessary licenses and certifications and following state-specific regulations and industry standards.

Technological advancements, such as data analytics and artificial intelligence, may help insurance companies assess risk more accurately, potentially making it easier for policyholders to qualify for Waiver of Coinsurance Clauses. Changing regulations may also impact the availability and conditions of these clauses, requiring insurance brokers to stay up-to-date on the latest developments to provide the best possible service to their clients.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.