Surplus lines insurance is a type of insurance coverage that is provided by insurers that are not licensed or admitted to sell insurance in a particular state. This type of insurance is typically used to provide coverage for unique or high-risk exposures that are not covered by traditional insurance policies. The purpose of surplus lines insurance is to provide coverage for risks that are not covered by traditional insurance policies. These risks may be unique or high-risk and may be difficult or impossible to insure through traditional insurance markets. Surplus lines insurance has been around for over a century, and its origins can be traced back to the early 1900s when it was used to provide coverage for hard-to-place risks such as ships and cargo. Over time, the market for surplus lines insurance has grown and expanded to include a wide range of risks and exposures. Surplus lines insurers are typically non-admitted insurance companies that are not licensed or authorized to sell insurance in a particular state. In order to be eligible to provide surplus lines insurance, insurers must meet certain financial and regulatory requirements and must be approved by the state insurance department. Surplus lines insurance policies are typically used to provide coverage for unique or high-risk exposures that are not covered by traditional insurance policies. In order to be eligible for coverage, these risks must meet certain criteria and must be difficult or impossible to insure through traditional insurance markets. Surplus lines insurance policies may provide coverage for a wide range of risks and exposures, including property, casualty, liability, and professional liability. However, these policies may also have limitations and exclusions that are not found in traditional insurance policies, and may have higher premiums and deductibles. Surplus lines insurance is typically used to provide coverage for risks that are difficult or impossible to insure through traditional insurance markets. These risks may be unique or high-risk and may require specialized coverage that is not available through traditional insurance policies. Surplus lines insurance is typically sold through brokers who specialize in placing coverage for hard-to-place risks. These brokers have expertise in the specific risks and exposures that are covered by surplus lines insurance and can help clients find the right coverage for their needs. The insurance placement process for surplus lines insurance is typically more complex than for traditional insurance policies. This is because the insurer is not licensed or admitted to sell insurance in the state where the coverage is being provided, and the broker must follow specific regulatory requirements in order to place the coverage. Surplus lines insurance policies are typically issued by the non-admitted insurer, rather than by the broker. These policies may have different terms and conditions than traditional insurance policies, and may have higher premiums and deductibles. Surplus lines insurance provides access to coverage for unique or hard-to-place risks that may not be covered by traditional insurance policies. This can be particularly valuable for businesses or individuals that have specialized insurance needs. Surplus lines insurance policies can be customized to meet the specific needs of the insured. This can include tailored coverage, higher limits, or unique terms and conditions. Surplus lines insurance can provide coverage for high-risk policies that may be difficult or impossible to insure through traditional insurance markets. This can include risks such as terrorism, cyber liability, or environmental liability. Surplus lines insurance may be less expensive than traditional insurance policies for certain types of risks. This is because the market for surplus lines insurance is not subject to the same regulatory requirements as traditional insurance markets, which can result in lower costs. Surplus lines insurance is not subject to the same regulatory oversight as traditional insurance markets, which can result in limited consumer protection. This can include less stringent underwriting and claims handling requirements, as well as fewer options for recourse in the event of a dispute. Surplus lines insurance policies may have higher premiums and deductibles than traditional insurance policies. This is because the market for surplus lines insurance is less competitive than traditional insurance markets, which can result in higher costs for consumers. Surplus lines insurers may be more likely to become insolvent or go out of business than traditional insurance companies. This is because they are not subject to the same regulatory requirements as traditional insurance companies, and may not have the same financial strength or stability. Surplus lines insurance is typically excluded from state guarantee funds, which are designed to protect consumers in the event that their insurance company becomes insolvent. This means that consumers who purchase surplus lines insurance may not have the same level of protection as those who purchase traditional insurance policies. The surplus lines insurance market is a relatively small segment of the overall insurance market, accounting for approximately 14% of total premiums written in the U.S. in 2020. However, the market has grown in recent years and is expected to continue to expand. The surplus lines insurance market provides coverage for a wide range of risks and exposures, including hard-to-place risks, high-risk policies, and unique insurance needs. This can include coverage for terrorism, cyber liability, environmental liability, and other specialized risks. The surplus lines insurance market is constantly evolving, and there are a number of emerging trends that are shaping the market. These include increased competition, new product offerings, and changes in regulatory requirements. Surplus lines insurance is a type of insurance coverage that is provided by non-admitted insurers for unique or high-risk risks that are difficult or impossible to insure through traditional insurance markets. Surplus lines insurance is typically sold through brokers who specialize in hard-to-place risks, and policies are issued by non-admitted insurers. Surplus lines insurance may have higher premiums and deductibles than traditional insurance policies, but can provide access to unique coverage and customized policies. Advantages of surplus lines insurance include access to unique coverage, customized policies, and the ability to insure high-risk policies. Disadvantages include limited consumer protection, higher premiums and deductibles, insolvency risk, and exclusion from state guarantee funds. The surplus lines insurance market is a small but growing segment of the overall insurance market, and provides coverage for a wide range of risks and exposures. Emerging trends in the market include increased competition, new product offerings, and changes in regulatory requirements.Definition of Surplus Lines Insurance

Characteristics of Surplus Lines Insurance

Insurer Eligibility Requirements

Policy Eligibility Requirements

Coverage and Limitations

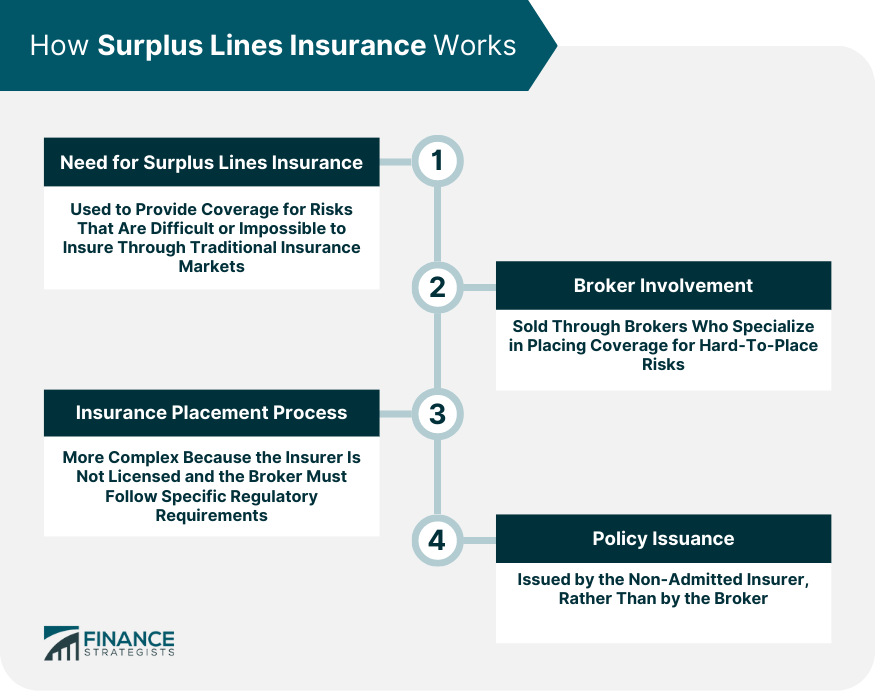

How Surplus Lines Insurance Works

Need for Surplus Lines Insurance

Broker Involvement

Insurance Placement Process

Policy Issuance

Advantages of Surplus Lines Insurance

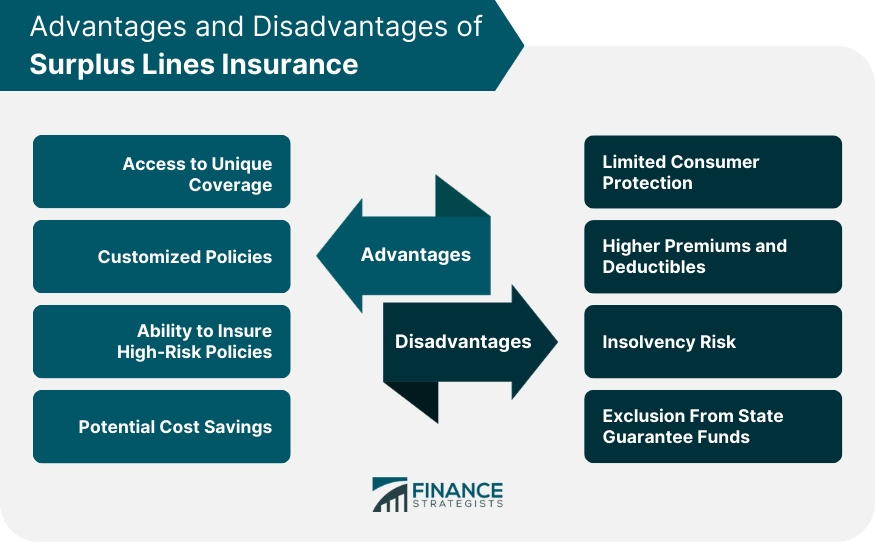

Access to Unique Coverage

Customized Policies

Ability to Insure High-Risk Policies

Potential Cost Savings

Disadvantages of Surplus Lines Insurance

Limited Consumer Protection

Higher Premiums and Deductibles

Insolvency Risk

Exclusion From State Guarantee Funds

Surplus Lines Insurance Market

Size of Surplus Lines Insurance Market

Types of Risks Covered

Emerging Trends in the Surplus Lines Insurance Market

Conclusion

Surplus Lines Insurance FAQs

Surplus Lines Insurance is a type of insurance that provides coverage for risks that are not covered by traditional insurance companies.

Surplus Lines Insurance involves the use of brokers to help place coverage with non-admitted insurers who can provide coverage for unique or high-risk situations.

Advantages of Surplus Lines Insurance include access to unique coverage, customized policies, and the ability to insure high-risk policies, potentially at a lower cost than traditional insurance.

Disadvantages of Surplus Lines Insurance include limited consumer protection, higher premiums and deductibles, insolvency risk, and exclusion from state guarantee funds.

Yes, Surplus Lines Insurance is regulated both at the state and federal levels, with the National Association of Insurance Commissioners (NAIC) providing a model law for states to follow.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.