An insurance claim is a formal request made by a policyholder to an insurance company for financial reimbursement or coverage based on the terms and conditions of the insurance policy. The claim is submitted when the insured individual or entity experiences a loss or damage covered under the policy, such as an accident, illness, or property damage. Insurance claims are an essential aspect of the insurance system, as they ensure that policyholders receive the financial protection they have paid for through their premiums. The insurance claim process is crucial for both policyholders and insurance companies. For policyholders, claims are the primary means of obtaining financial support and protection in the event of a loss, ensuring that they can recover and return to their pre-loss financial situation. For insurance companies, processing and settling claims is a critical part of their business operations, as it demonstrates their commitment to honoring the policies they have sold. A well-managed claims process helps build trust between insurers and policyholders, ensuring customer satisfaction and long-term business success. Health insurance claims are filed when policyholders seek reimbursement for medical expenses incurred due to illness, injury, or other health-related issues covered by their health insurance policy. These claims can include costs for hospital stays, surgeries, prescription medications, or other treatments and services. Health insurance claims can be submitted either by the healthcare provider or the policyholder, depending on the insurance plan's structure and requirements. In some cases, the insurer may pay the provider directly, while in others, the policyholder may be required to pay the expenses upfront and seek reimbursement later. Auto insurance claims are filed when policyholders experience vehicle damage, theft, or personal injury resulting from an accident or other covered event. These claims can cover a range of costs, including vehicle repairs, replacement costs, medical expenses, and even legal fees in case of a lawsuit. Filing an auto insurance claim typically requires the policyholder to report the incident to their insurer, provide documentation such as police reports or photographs, and cooperate with the insurance company's investigation and assessment of the claim. Policyholders file homeowner insurance claims when their home or personal property sustains damage or is destroyed due to a covered event like a fire, storm, or theft. Repair or replacement expenses for the house and compensation for damaged or lost personal belongings may be included in these claims. Detailed information about the incident, including an inventory of damaged or lost items and any pertinent documentation such as photos, receipts, or appraisals, must be provided by policyholders when filing a homeowner insurance claim. Additionally, an inspection of the property might be necessary for the insurance company to evaluate the extent of the damage and establish the suitable compensation. When a policyholder passes away, beneficiaries file life insurance claims, and the death benefit, as outlined in the life insurance policy, becomes payable. Financial assistance is provided to the beneficiaries through these claims, aiding them in covering various expenses including funeral costs, outstanding debts, and ongoing living expenses. In order to initiate a life insurance claim, beneficiaries are required to submit a claim form along with a certified copy of the policyholder's death certificate to the insurance company. Following this, the insurer will review the claim and, upon approval, disburse payment to the beneficiaries in accordance with the terms of the policy. Policyholders file travel insurance claims for losses or disruptions during their trip, like trip cancellations, medical emergencies, lost luggage, or travel delays. The coverage included in the policy determines the expenses that can be covered. To file a claim, policyholders need to submit a claim form and any necessary documentation, such as receipts or proof of trip cancellation. The insurer reviews the claim and provides reimbursement according to the policy's terms and conditions. The first step in the insurance claim process is notifying the insurer of the loss or damage that has occurred. Policyholders should report the incident as soon as possible, providing details about the event and any relevant documentation that may be required. Once the insurer has been notified of the claim, they will begin an investigation to determine the cause of the loss, the extent of the damage, and the validity of the claim. This may involve reviewing documentation, conducting interviews, and inspecting the property or vehicle involved. The investigation helps the insurer assess the claim and determine the appropriate compensation based on the policy's terms and conditions. During the claim process, policyholders may be required to submit various documents to support their claim, such as police reports, medical records, receipts, or photographs. It is essential to provide accurate and complete information to help the insurer assess the claim and expedite the process. After the investigation and documentation submission, the insurance company will evaluate the claim, determining the coverage available under the policy and the amount of compensation owed to the policyholder. This evaluation may include reviewing the policy's terms and conditions, assessing the extent of the damage, and calculating the costs associated with the loss. Once the claim evaluation is complete, the insurer will issue a settlement, either approving the claim and providing the agreed-upon compensation or denying the claim based on the findings of the investigation and evaluation. In some cases, the insurer and policyholder may need to negotiate the settlement amount or involve third-party mediation or arbitration to resolve disputes. One common issue faced by policyholders during the claim process is coverage denial, where the insurer determines that the loss or damage is not covered under the terms of the policy. To avoid coverage denial, policyholders should thoroughly understand their policy's coverage and exclusions and ensure they have adequate protection for their needs. Another common issue is receiving a low settlement offer from the insurance company, which may not fully cover the costs associated with the loss or damage. In these cases, policyholders may need to negotiate with their insurer, provide additional documentation to support their claim, or seek legal assistance to obtain a fair settlement. Delayed payments can be frustrating for policyholders who are relying on their insurance claim to cover immediate expenses or financial needs. Delays may result from various factors, such as incomplete documentation, disputes over the claim amount, or administrative issues within the insurance company. Policyholders can help minimize delays by promptly submitting all required documentation and maintaining open communication with their insurer. In some claims, particularly auto insurance claims, liability for the loss or damage may be disputed between the parties involved. This can lead to delays in the claim process and potentially result in legal disputes or litigation. Policyholders should be prepared to provide evidence to support their claim, such as witness statements, photographs, or police reports, to help resolve liability disputes. Insurance fraud is a significant issue in the industry, with some individuals or entities submitting fraudulent claims to obtain financial compensation they are not entitled to. Insurers take fraud seriously and may thoroughly investigate claims to detect and prevent fraudulent activity. Policyholders should be aware of the potential consequences of insurance fraud, including claim denial, policy cancellation, and legal penalties. To ensure a smooth claim process, policyholders should have a thorough understanding of their insurance policy, including the coverage, exclusions, and any specific requirements for filing a claim. This knowledge will help policyholders navigate the claim process more effectively and avoid potential issues or disputes with their insurer. Policyholders should contact their insurer as soon as possible after a loss or damage occurs, providing all relevant information and documentation required. Timely reporting not only helps expedite the claim process but may also be a requirement under the policy's terms and conditions. Maintaining organized records of all documentation related to the claim, such as receipts, invoices, medical records, or police reports, can be beneficial during the claim process. These records can help support the policyholder's claim and provide evidence to the insurer, making it easier to assess the claim and determine the appropriate compensation. Policyholders should ensure that they are honest and thorough in their reporting of the incident and the resulting loss or damage, as providing false or misleading information can lead to claim denial, policy cancellation, or even legal consequences. Maintaining open and effective communication with the insurance company is critical throughout the claim process. Policyholders should respond promptly to any requests for information or documentation, ask questions if they are unclear about any aspect of the process, and keep their insurer informed of any developments related to the claim. An insurance claim is a formal request made by a policyholder to an insurance company for financial reimbursement or coverage based on the terms and conditions of the insurance policy. Claims are an essential aspect of the insurance system, providing financial protection and support to policyholders in the event of a loss or damage. There are various types of insurance claims, including health insurance claims, auto insurance claims, homeowner insurance claims, life insurance claims, and travel insurance claims. Each type of claim has its unique requirements and processes, depending on the specific coverage provided by the policy. The insurance claim process typically involves notification of the claim, investigation, documentation submission, claim evaluation, and settlement. By understanding each step in the process, policyholders can navigate the claim more effectively and increase their chances of a successful outcome.What Is an Insurance Claim?

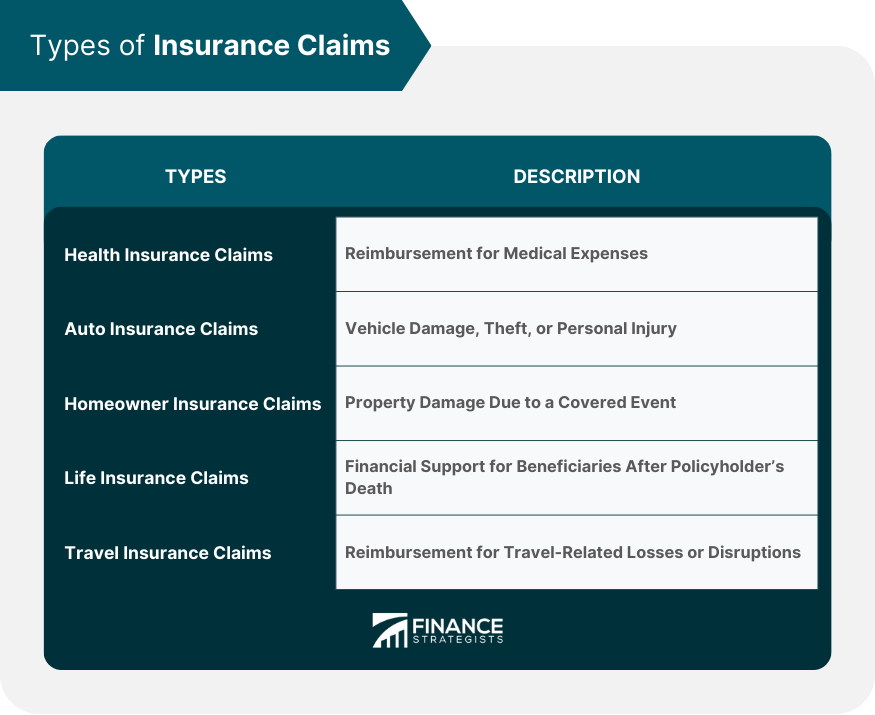

Types of Insurance Claims

Health Insurance Claims

Auto Insurance Claims

Homeowner Insurance Claims

Life Insurance Claims

Travel Insurance Claims

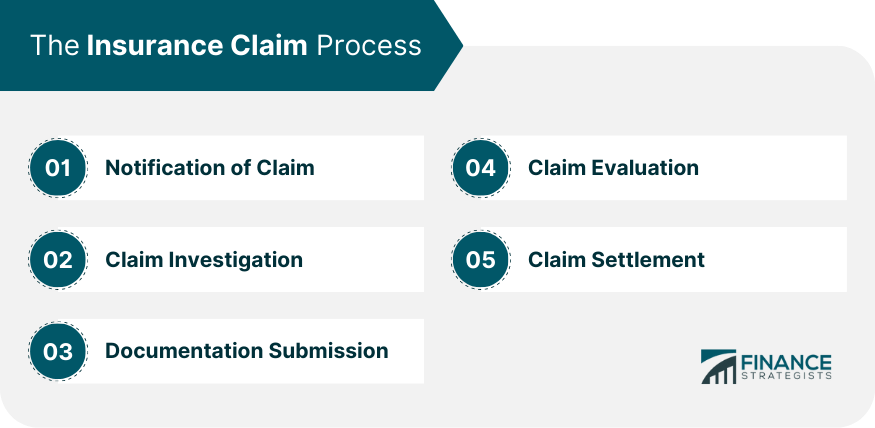

The Insurance Claim Process

Step 1: Notification of Claim

Step 2: Claim Investigation

Step 3: Documentation Submission

Step 4: Claim Evaluation

Step 5: Claim Settlement

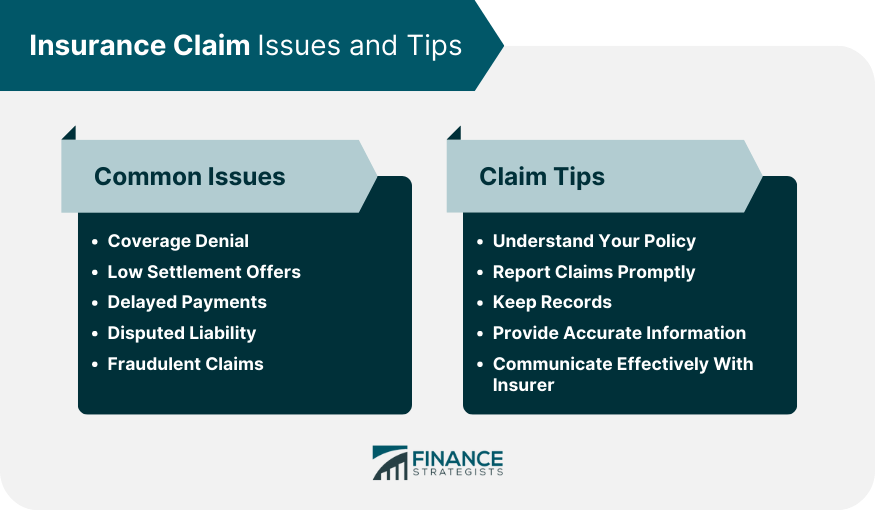

Common Issues in Insurance Claims

Coverage Denial

Low Settlement Offers

Delayed Payments

Disputed Liability

Fraudulent Claims

Insurance Claim Tips for Policyholders

Understand Your Policy

Report Claims Promptly

Keep Records

Provide Accurate Information

Communicate Effectively With Insurer

Final Thoughts

Insurance Claim FAQs

An insurance claim is a request made to an insurance company for financial compensation for a loss or damage covered by the policy.

There are various types of insurance claims, such as health, auto, homeowner, life, and travel insurance claims.

The insurance claim process includes notifying the insurer, claim investigation, documentation submission, claim evaluation, and claim settlement.

Common issues in insurance claims include coverage denial, low settlement offers, delayed payments, disputed liability, and fraudulent claims.

Policyholders should understand their policy, report claims promptly, keep records, provide accurate information, and communicate effectively with their insurer.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.