Real Estate Mortgage Investment Conduit (REMIC) is a tax vehicle established under the United States Internal Revenue Code. A REMIC assembles mortgages and similar types of debt into a pool and then issues securities representing an interest in the mortgage pool. These financial instruments are mainly used to securitize mortgage loans, allowing lenders to free up capital for further lending and providing investment opportunities for individuals and institutions. The concept of REMICs was introduced by the Tax Reform Act of 1986 to support the housing market. It was intended to address issues with the then-existing mortgage-backed securities, ensuring improved liquidity and offering an efficient and transparent vehicle for channeling funds from investors to the housing market. The sponsor, often a bank or other financial institution, initiates the REMIC process. It identifies and assembles the mortgages to be pooled and sold to a depositor. The depositor, usually a special-purpose vehicle, purchases the pool of mortgages from the sponsor. The depositor then transfers the mortgages to the REMIC, effectively transforming them into securities backed by the pooled mortgages. The servicer's role involves managing the mortgages in the pool. They are responsible for activities such as collecting payments from borrowers, handling defaults and foreclosures, and distributing the collected payments to REMIC investors. The trustee is responsible for ensuring that the REMIC operates in the best interests of the investors. This includes overseeing the servicer's activities, managing the trust's funds, and distributing payments to the investors. A notable feature of REMICs is the creation of separate classes of securities, or "tranches," with different risk profiles, maturity dates, and yields to satisfy varying investor needs. Different Classes of Securities: Tranches allow for dividing the total mortgage pool into different segments based on the expected cash flow of the underlying mortgages. Variable Risk Profiles: Each tranche has a unique risk profile that caters to different types of investors. Senior tranches are less risky and offer lower yields, while junior tranches are more risky and provide higher yields. Diverse Maturity Dates: Tranches can have varying maturities. This allows investors to choose tranches that match their investment horizon. Sequential Pay Structure: Usually, REMIC tranches follow a sequential pay structure where senior tranches receive principal repayments before junior tranches. REMIC tranches are a cornerstone of the mortgage-backed securities market. They allow for repackaging mortgage loans into securities that can be sold to investors. These securities provide investors with cash flows generated from the underlying mortgages. Investment Opportunities: REMIC tranches provide various investment opportunities for different types of investors, from those seeking stable, lower-risk investments to those seeking higher returns and willing to accept more risk. Liquidity in the Housing Market: By pooling mortgages and creating securities that can be sold to investors, REMIC tranches help to provide liquidity in the housing market, enabling lenders to make more loans. Risk Management: The tranche structure allows for the distribution of risk among various types of investors, which can help to stabilize the mortgage market. REMICs are a form of tax-efficient investment vehicle designed for the securitization of mortgage loans. They enjoy a unique status in terms of federal income taxation, which can make them attractive to investors. REMICs are structured as "pass-through" entities for federal income tax purposes. No Double Taxation: As pass-through entities, REMICs themselves generally aren't subject to federal income tax. Instead, the tax liability is "passed through" to the investors. This structure avoids the double taxation issue (corporate and shareholder levels) associated with traditional corporations. Taxable Income: Investors are taxed on their share of the REMIC's taxable income, regardless of whether the income is distributed. Investors can receive two types of income from a REMIC investment: Regular Interest: This is the most common form of REMIC income. It's treated as ordinary interest income for tax purposes and is taxed at the investor's ordinary income tax rate. Excess Inclusions: These amounts exceed the investor's REMIC net income share. They are taxable as ordinary income and may not be offset by net operating losses. REMICs must adhere to certain rules to maintain their tax status: Static Pool Requirement: A REMIC must consist of a fixed pool of mortgages and cannot actively trade its mortgage assets. Single Class of Ownership Requirement: A REMIC can only have one class of ownership interest, although this interest may be divided into different maturity and payment rights tranches. Tax on Prohibited Transactions: REMICs are subject to a 100% tax on income from prohibited transactions, such as the disposition of a qualified mortgage or receipt of income from services. REMICs operate within a specific legal and regulatory framework. Here are the main elements: The U.S. tax code, specifically sections 860A-860G, governs REMICs. It outlines their tax status, allowable activities, and reporting requirements. The Tax Reform Act of 1986, which introduced the REMIC, sets forth the rules for establishing and maintaining a REMIC. This includes requiring a REMIC to have a fixed pool of real estate mortgages and permissible investments. REMICs often involve securities transactions. As a result, they're subject to SEC rules and regulations, particularly if the REMIC interests are publicly traded. REMICs must also comply with FASB financial reporting guidelines. This includes the requirement to provide transparent and accurate information to investors. State laws may also apply, particularly regarding real estate transactions and securities offerings. The specifics can vary from state to state. If a bank or other financial institution is involved in the formation or operation of a REMIC, it may be subject to additional banking regulations. This could include regulations from the Office of the Comptroller of the Currency (OCC), the Federal Reserve, and the Federal Deposit Insurance Corporation (FDIC). Securitization of mortgages is a significant financial process, and REMICs play a crucial role in this system. Mortgage securitization is how individual mortgages are bundled into a pool and sold as a single security on the investment market. This process allows banks and other lending institutions to remove the loans from their books, freeing up capital to make additional loans. REMICs are a type of special-purpose vehicle used to hold the mortgage pool in the securitization process. They acquire mortgages from originators, pool them together, and then issue mortgage-backed securities (MBS) to investors. One of the unique aspects of REMICs is the concept of "tranching." The mortgage pool is divided into different "tranches," or segments with risk and return profiles. This allows investors to choose the level of risk and potential return that best suits their investment goals. The securitization of mortgages through REMICs substantially impacts the mortgage market. Providing a mechanism to move loans off the original lenders' books increases the liquidity in the housing market and allows for the origination of more loans. However, it also can lead to increased risk, as seen during the financial crisis of 2008 when the collapse of the mortgage-backed securities market led to a widespread financial meltdown. Steady Cash Flow: One of the main benefits of investing in REMICs is the steady cash flow. REMICs pay regular income to investors from mortgage payments, providing a consistent revenue stream. Risk Diversification: Investing in REMICs allows diversification because the mortgage-backed securities are pooled from various mortgages. This spreads the risk across multiple assets, reducing the impact of a single loan default. Flexibility: REMICs offer different tranches catering to varying risk appetites. Investors can choose a tranche that best aligns with their investment goals and risk tolerance. Interest Rate Risk: The value of REMICs can be sensitive to changes in interest rates. If rates increase, the value of existing mortgage-backed securities can decrease, potentially leading to investor losses. Prepayment Risk: Mortgage borrowers often have the option to pay off their mortgages early. When this happens, the investor may not receive the expected interest income, disrupting their expected cash flow. Credit Risk: There's a risk that borrowers may default on their mortgage payments. This risk can be higher with mortgages that have been issued to borrowers with lower creditworthiness. Complexity and Lack of Transparency: REMICs can be complex investment vehicles, and it can be challenging for investors to understand the underlying mortgages' quality. The 2008 financial crisis highlighted the potential for information asymmetry and misaligned incentives in the securitization process. REMICs, like other investment vehicles, are affected by economic trends. Factors such as interest rates, housing market conditions, and overall economic health can impact the performance of REMICs and the returns they offer to investors. The 2008 financial crisis highlighted the risks of mortgage-backed securities, including REMICs. Since then, changes have been implemented to improve transparency and risk management in the REMIC and broader MBS market. These include tighter regulations, enhanced disclosure requirements, and the implementation of risk retention rules. REMICs have played a pivotal role in the financial innovation of mortgage-backed securities. REMICs are expected to remain integral to the MBS market, contributing to housing finance and offering diverse investment opportunities. The future of REMICs will be influenced by evolving regulatory landscapes, technological advances, and changes in the housing market and the broader economy. When discussing Mortgage-Backed Securities (MBS), it's important to understand the differences and similarities between REMICs and other types of MBS. REMIC: This special vehicle is designed to securitize mortgages. REMICs allow the pooling of mortgage loans and issuance of multiple classes of securities. This provides flexibility to suit different investors' needs. Other MBS: Other types of MBS, like pass-through securities, also pool mortgages but typically issue a single security class. These securities pass the principal and interest payments directly to the investors. REMIC: By structuring the mortgages into different tranches, REMICs provide a tiered risk structure. This allows investors to choose tranches that match their risk tolerance. Other MBS: Other MBS, such as pass-through securities, spread the risk across all investors equally. The risk is generally tied to the creditworthiness of the overall pool of mortgages. REMIC: In a REMIC, prepayment risk is typically allocated among the different tranches based on their structure. Some tranches may be designed to absorb more prepayment risk than others. Other MBS: In traditional MBS, all investors share the prepayment risk equally. If mortgage holders prepay their loans, all investors are affected proportionately. REMICs play a significant role in the financial market by facilitating the securitization of mortgages, contributing to the liquidity of the mortgage market, and offering diverse investment opportunities. Understanding the structure, risks, and benefits of REMICs is crucial for potential investors. For individual and institutional investors, REMICs offer a way to invest indirectly in the real estate market. With various risk and return profiles available, investors can choose securities that align with their investment goals and risk tolerance. Proper wealth management is crucial to fully realize the potential benefits of investing in REMICs. Working with a professional financial advisor can help investors navigate the complexities of REMICs, align investments with financial goals, and mitigate potential risks.What Is a Real Estate Mortgage Investment Conduit (REMIC)?

Understanding the Structure of REMIC

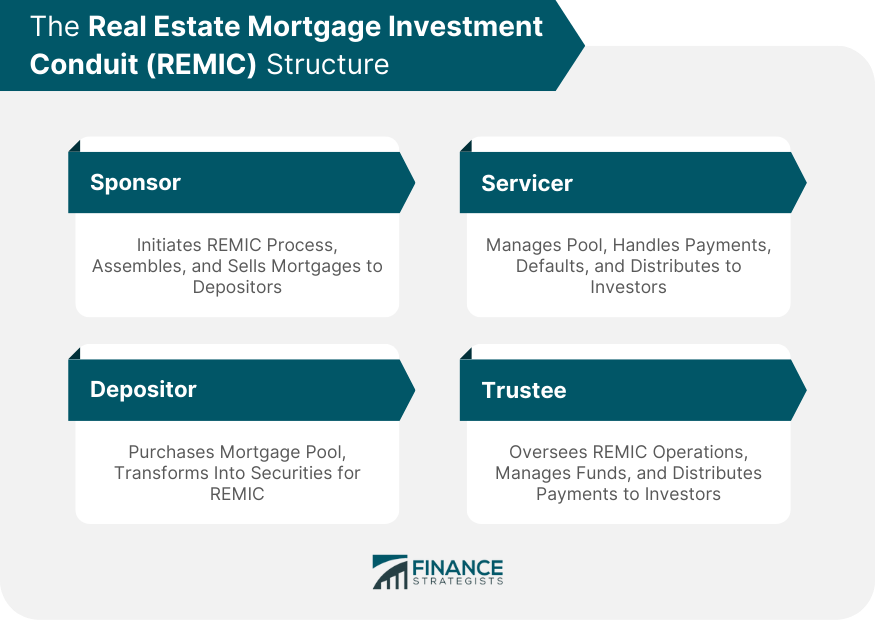

Role of the Sponsor

Involvement of the Depositor

Services Provided by the Servicer

Responsibilities of the Trustee

Concept of REMIC Tranches

Key Features

Role of REMIC Tranches in Mortgage-Backed Securities

Taxation Aspects of REMIC

REMICs as Pass-Through Entities

Types of REMIC Income

Special REMIC Rules

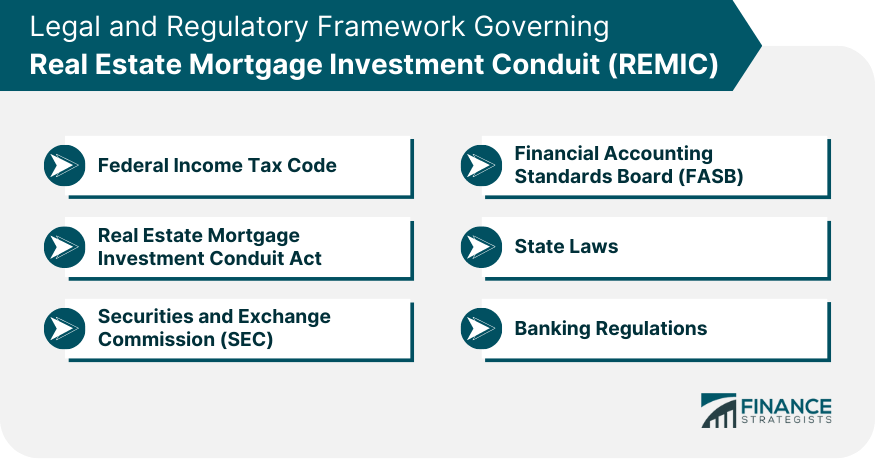

Legal and Regulatory Framework Governing REMIC

Federal Income Tax Code

Real Estate Mortgage Investment Conduit Act

Securities and Exchange Commission (SEC)

Financial Accounting Standards Board (FASB)

State Laws

Banking Regulations

REMIC and the Securitization of Mortgages

Process of Mortgage Securitization

Role of REMIC in Mortgage Securitization

REMIC Structure and Tranching

Impact on the Mortgage Market

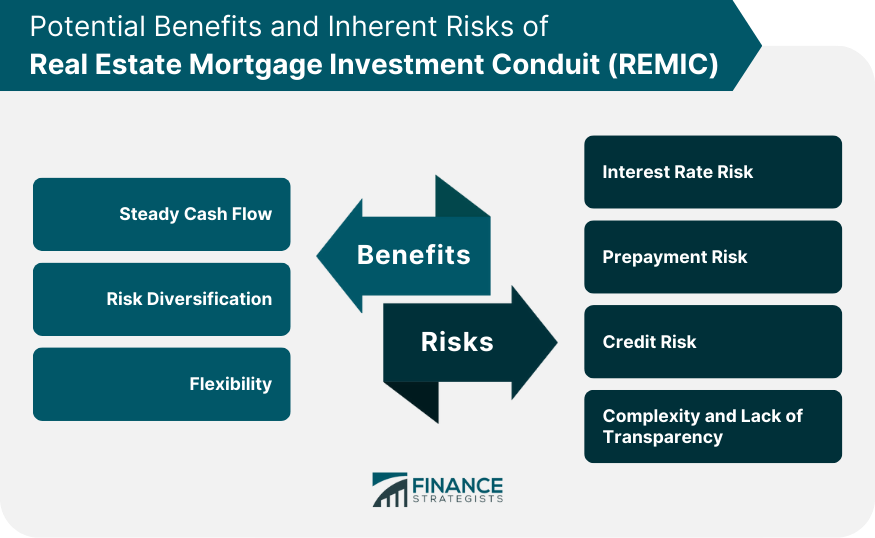

Potential Benefits of Investing in REMIC

Inherent Risks of Investing in REMIC

REMIC in the Current Financial Landscape

Impact of Economic Trends on REMICs

REMICs in the Aftermath of Financial Crises

REMIC's Role in Financial Innovation and Future Outlook

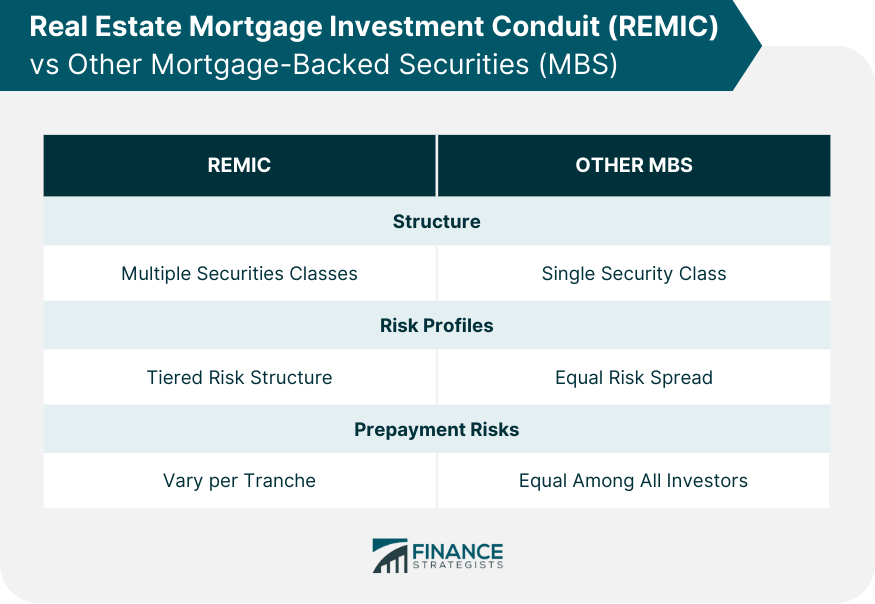

REMIC vs Other Mortgage-Backed Securities (MBS)

Structure and Function

Risk Profiles

Prepayment Risks

Final Thoughts

Real Estate Mortgage Investment Conduit (REMIC) FAQs

A Real Estate Mortgage Investment Conduit (REMIC) is a vehicle used to securitize mortgage loans, allowing lenders to free up capital for further lending and providing investment opportunities for individuals and institutions.

A REMIC pools mortgages and issues securities representing interests in these mortgages. It has a multilevel structure involving a sponsor, a depositor, a servicer, and a trustee, each playing a specific role in its operation.

Investing in a REMIC offers exposure to the real estate market without investing directly in property. It provides a regular income and allows for selecting investment tranches that align with the investor’s risk tolerance.

Investing in REMICs carries risks such as credit risk, prepayment risk, and interest rate risk. Economic trends, housing market conditions, and the quality of the underlying mortgages can influence the performance of a REMIC.

REMICs are considered "pass-through" entities, meaning the income they generate is passed directly to investors, who then pay taxes on it according to their individual tax rates. However, REMICs face certain tax considerations, such as a 100% tax on any prohibited transaction and potential tax consequences for non-compliance with certain requirements.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.