Value at Risk (VaR) is a widely used risk management metric that quantifies the potential loss in the value of a portfolio or investment over a specified time period and at a given confidence level. VaR is used to estimate the maximum potential loss that an investment or portfolio could incur under normal market conditions. There are several methods for calculating VaR, one of which is the Historical VaR method. Historical VaR, also known as empirical VaR or non-parametric VaR, is a method of calculating Value at Risk that relies on historical data to estimate the potential loss of an investment or portfolio. It involves analyzing the historical returns of the investment or portfolio over a specified time period to determine the likelihood of experiencing a certain level of loss in the future. The Historical VaR method is based on the assumption that past market behavior is a good indicator of future market behavior. It does not make any assumptions about the distribution of returns, which distinguishes it from other VaR calculation methods, such as Parametric VaR and Monte Carlo VaR. The first step in calculating Historical VaR is collecting historical data. The chosen time period, frequency, and data source will have an impact on the results. It is essential to use reliable data sources and consider factors such as market conditions, structural changes, and economic events when selecting the time period. Once the data is collected, the next step is to calculate returns, sort them, and identify the VaR threshold. The returns are calculated as the percentage change in value over the specified time period. The sorted returns are then used to determine the VaR threshold, which represents the loss amount at the specified confidence level. Historical VaR is determined by selecting a confidence level, holding period, and identifying the corresponding loss amount. The confidence level represents the probability of not exceeding the potential loss, while the holding period is the length of time for which the risk is being estimated. Historical VaR has several advantages, including simplicity and ease of calculation. It does not require any distribution assumptions and incorporates actual historical events, making it a more realistic representation of potential losses. However, Historical VaR also has limitations. It assumes history will repeat itself, making it sensitive to the chosen time period. It may not accurately capture recent trends or structural changes in the market and has limited usefulness in stress testing, as it may not adequately account for extreme events. Parametric VaR, also known as Variance-Covariance VaR, assumes that asset returns follow a known distribution, typically the normal distribution. This method relies on the calculation of the mean and standard deviation of returns to estimate potential losses. Parametric VaR is calculated using the mean, standard deviation, and confidence level. It assumes that the returns are normally distributed and uses the standard normal distribution to determine the VaR threshold. Parametric VaR is computationally efficient and easy to calculate. However, its reliance on distribution assumptions can lead to inaccurate estimates, especially for assets with non-normal return distributions. Monte Carlo VaR is a simulation-based method that generates multiple scenarios of future asset returns to estimate potential losses. It is a more advanced approach that accounts for the correlations and non-linearities in asset returns. Monte Carlo VaR involves simulating a large number of scenarios based on historical data, calculating returns for each scenario, and determining the VaR threshold by sorting the simulated returns. Monte Carlo VaR can provide more accurate estimates, as it accounts for non-normal return distributions and correlations. However, it is computationally intensive and requires sophisticated modeling techniques. Historical VaR, Parametric VaR, and Monte Carlo VaR have their unique advantages and limitations. Historical VaR is suitable for portfolios with limited historical data and is easy to compute, but may not capture recent trends or extreme events. Parametric VaR is computationally efficient but relies on distribution assumptions that may not hold for all assets. Monte Carlo VaR is more accurate and accounts for non-normal return distributions and correlations, but requires advanced modeling techniques and is computationally intensive. VaR is widely used by financial institutions such as banks, investment funds, and insurance companies for risk management, portfolio optimization, and regulatory compliance. In the regulatory environment, the Basel accords and other regulatory frameworks require financial institutions to maintain adequate capital levels based on their risk exposure, with VaR being one of the key metrics used to assess this risk. Investment managers use VaR to optimize their portfolios, identifying the optimal trade-offs between risk and return. It is also used as a performance evaluation tool, allowing investors to assess risk-adjusted returns and make informed investment decisions. Despite its widespread use, the reliability of VaR has been questioned, particularly during extreme market events. The 2008 financial crisis highlighted the limitations of VaR in predicting and managing risk during periods of market turbulence. As a result, alternative risk measures have gained prominence, such as Expected Shortfall (ES), Conditional Value at Risk (CVaR), and tail risk measures. These metrics aim to provide a more comprehensive view of risk, focusing on the potential losses in the extreme tail of the distribution. Historical VaR is a widely used method for estimating portfolio risk, offering simplicity and ease of calculation. However, its limitations, including its sensitivity to the chosen time period and its assumption that history repeats itself, should be considered when using it as a risk management tool. Despite its limitations, VaR remains an essential risk management tool in modern finance, helping financial institutions manage risk, comply with regulatory requirements, and make informed investment decisions. As data and computation capabilities improve, more sophisticated VaR models can be developed to better account for market dynamics, correlations, and extreme events. Integration with other risk measures and evolving regulatory requirements will ensure that VaR continues to play a critical role in managing risk in the financial sector.What Is Historical VaR?

Calculation Methodology of Historical VaR

Data Collection

Data Processing

Determination of Historical VaR

Advantages of Historical VaR

Limitations of Historical VaR

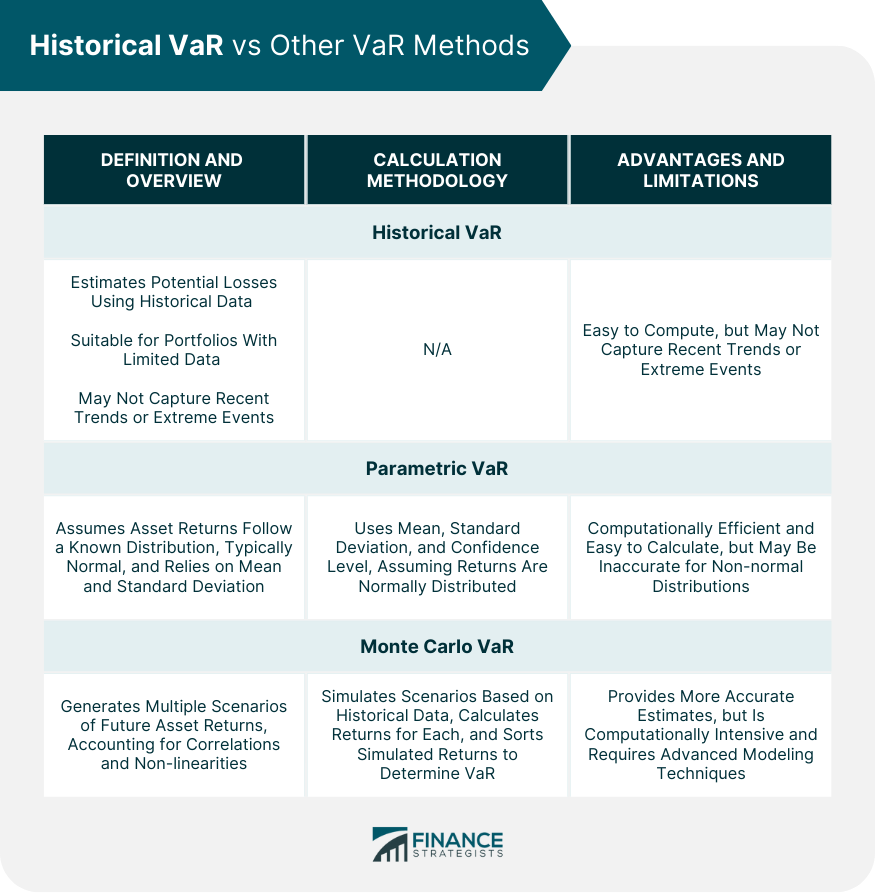

Historical VaR vs Other VaR Methods

Parametric VaR

Definition and Overview

Calculation Methodology

Advantages and Limitations

Monte Carlo VaR

Definition and Overview

Calculation Methodology

Advantages and Limitations

Comparison Summary

Real-World Applications of Historical VaR

Financial Institutions

Regulatory Environment

Investment Strategies

Criticisms and Controversies of Historical VaR

Reliability of VaR

Alternative Risk Measures

Conclusion

Historical VaR FAQs

Historical VaR stands for Historical Value at Risk, which is a risk management technique that estimates the potential losses that an investment or portfolio may face based on the historical returns of the asset.

To calculate Historical VaR, historical returns are used to determine the volatility of the asset or portfolio. The VaR calculation involves selecting a confidence level (e.g. 95%) and finding the corresponding percentile of the distribution of historical returns. The result is the maximum potential loss that can be expected at the selected confidence level.

Historical VaR is a simple and transparent method of measuring risk that does not rely on complex models or assumptions. It is also useful for evaluating the risk of investments that have limited data available, or for assessing the risk of new products that have not been tested in the market.

Historical VaR only considers past market movements and assumes that future market conditions will be similar. This can lead to underestimating the risk of events that have not been observed in the historical data. Additionally, Historical VaR does not take into account the possibility of extreme events that may occur beyond the selected confidence level.

Historical VaR is one of the simplest VaR methods, but it is also the least precise. Other VaR methods, such as Monte Carlo simulation and parametric VaR, can provide more accurate risk estimates by incorporating more complex models and assumptions. However, these methods can also be more time-consuming and require more data and expertise to implement.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.