Tax-efficient gifting strategies are methods individuals can use to transfer assets to others while minimizing their tax liability. They play a critical role in wealth management and estate planning. By minimizing the tax burden associated with transferring assets to loved ones or charitable organizations, individuals can maximize the value of their gifts and ensure their intentions are fulfilled. These strategies often involve the use of trusts, charitable donations, or other legal structures to take advantage of tax laws and reduce the amount of taxes owed on gifts or transfers of assets. Common tax-efficient gifting strategies include donor-advised funds, charitable remainder trusts, qualified charitable distributions, family limited partnerships, grantor retained annuity trusts (GRATs), and sales to intentionally defective grantor trusts (IDGTs), among others. The federal gift tax applies to transfers of property or assets from one individual to another when the donor receives nothing or less than full value in return. The tax implications of these transfers depend on the annual exclusion, lifetime exemption, and tax rates. 1. Annual exclusion: For 2026, the annual gift tax exclusion is $19,000 (also $19,000 in 2025) per recipient. This means that an individual can give up to $19,000 to any number of recipients in 2025 without incurring federal gift tax. 2. Lifetime exemption: In addition to the annual exclusion, each individual has a lifetime gift tax exemption. In 2026, the lifetime exemption is $15 million ($13.99 million in 2025). Gifts exceeding the annual exclusion are applied against this lifetime exemption, which is also applicable to estate taxes. 3. Tax rates: Gifts exceeding both the annual exclusion and the lifetime exemption are subject to federal gift tax rates, which can reach up to 40%. Some states also impose gift taxes, with state-level exemptions and rates varying significantly. However, many states do not have a gift tax, so it is essential to consult with a tax professional to understand your state's specific rules. Maximizing the annual gift tax exclusion is one of the simplest and most effective tax-efficient gifting strategies. Splitting gifts between spouses: Married couples can combine their annual exclusions to give up to $38,000 per recipient in 2026 (also $38,000 in 2025) without incurring gift tax. Gifting to multiple recipients: By giving to multiple recipients, an individual can maximize the use of their annual exclusion and transfer significant wealth without gift tax consequences. Larger gifts may be subject to gift tax, but the lifetime gift tax exemption allows for substantial transfers with no tax liability. Unified credit: The unified credit combines the lifetime gift tax exemption with the estate tax exemption, allowing individuals to make significant lifetime gifts without reducing the available estate tax exemption. Strategic timing of gifts: Consider the timing of your gifts to maximize the use of your annual exclusions and lifetime exemption, as well as any potential appreciation in the value of the gifted assets. Transferring appreciated assets can be a tax-efficient gifting strategy, as the recipient typically assumes the donor's cost basis, potentially reducing capital gains tax liability upon sale. Stocks and other securities: Gifting appreciated stocks or securities can be particularly advantageous, as the recipient can defer capital gains taxes until the assets are sold. Real estate: Transferring appreciated real estate can also provide tax benefits, particularly if the property has been held for a long time and has significantly increased in value. Art and collectibles: Gifting art or collectibles can be another tax-efficient strategy, especially if the assets have appreciated significantly and are subject to capital gains taxes. Charitable giving can provide significant tax benefits while supporting meaningful causes. 1. Donor-advised funds: These funds allow donors to make charitable contributions and receive an immediate tax deduction, while retaining the ability to recommend grants to specific charities over time. 2. Charitable remainder trusts: This type of trust enables donors to contribute assets to a trust, which provides an income stream to the donor or beneficiaries for a specified period. At the end of the term, the remaining assets are transferred to a designated charity, offering both income tax deductions and potential estate tax benefits. 3. Charitable lead trusts: A charitable lead trust is the opposite of a charitable remainder trust, in that the income generated by the trust is donated to a designated charity for a specific period. At the end of the term, the remaining assets are transferred to the donor's beneficiaries, often with reduced estate and gift tax implications. 4. Qualified charitable distributions: Individuals aged 70½ or older can make qualified charitable distributions from their Individual Retirement Accounts (IRAs) directly to charities, which can count toward their required minimum distributions and potentially reduce income taxes. Certain gifting strategies can help minimize the tax burden when contributing to education and medical expenses. Paying tuition expenses directly to a qualifying educational institution on behalf of a student is exempt from gift tax, regardless of the amount. This exclusion applies only to tuition and not to other education-related expenses, such as room and board or books. 529 plans are tax-advantaged investment accounts designed to help save for education expenses. Benefits of 529 plans: Contributions to 529 plans grow tax-deferred, and withdrawals for qualified education expenses are tax-free at the federal level. Additionally, many states offer state income tax deductions for contributions to their 529 plans. Gifting strategies for 529 plans: Individuals can contribute up to five years' worth of annual gift tax exclusions to a 529 plan in a single year without incurring gift tax, provided no other gifts are made to the same beneficiary during the five-year period. Similar to education expenses, direct payments made to healthcare providers for another individual's medical expenses are not subject to gift tax. This tax benefit applies only to payments made for qualifying medical expenses and does not cover reimbursed expenses or payments to the individual receiving the medical treatment. Transferring family business interests can have significant tax implications, but certain strategies can help minimize tax liability. A family limited partnership (FLP) allows business owners to transfer business interests to family members while retaining control of the business. This strategy can help reduce the value of the owner's taxable estate and provide family members with limited partnership interests that may qualify for valuation discounts for gift and estate tax purposes. A GRAT enables the grantor to transfer assets, such as business interests, to a trust and receive an annuity for a specified term. If the assets appreciate beyond the IRS's assumed interest rate during the trust term, the excess appreciation passes to the trust beneficiaries free of gift tax. An IDGT is a trust that is "defective" for income tax purposes but effective for estate and gift tax purposes. By selling business interests to an IDGT in exchange for an installment note, the grantor can potentially freeze the value of the transferred assets for gift and estate tax purposes while shifting future appreciation to the trust beneficiaries. Life insurance can play a crucial role in tax-efficient gifting and wealth transfer. An ILIT is a trust designed to hold a life insurance policy outside of the grantor's taxable estate. When properly structured, an ILIT can help reduce estate taxes, provide liquidity for estate tax payments, and ensure that policy proceeds pass to beneficiaries as intended. A wealth replacement strategy involves using life insurance proceeds to replace the value of assets that have been gifted or donated to a trust or charity. This strategy can provide heirs with tax-free death benefits and ensure that the family's wealth is preserved while still taking advantage of tax-efficient gifting strategies. Proper estate planning can help maximize the benefits of tax-efficient gifting strategies. Coordinating gifting strategies with overall estate planning objectives ensures that assets are transferred efficiently and in accordance with the individual's wishes. This coordination may involve updating wills, trusts, and beneficiary designations to align with the chosen gifting strategies. Gifts made during an individual's lifetime can have a direct impact on estate taxes. Gifts that exceed the annual exclusion and the lifetime exemption may reduce the available estate tax exemption and increase estate tax liability. However, strategic gifting can help reduce the overall taxable estate. In some cases, significant gifting during an individual's lifetime can result in a lack of liquidity to cover estate tax payments upon their death. Life insurance or other assets may be used to provide the necessary liquidity to settle estate tax obligations and avoid the forced sale of other assets. Tax-efficient gifting strategies play a vital role in wealth management and estate planning. By understanding and implementing these strategies, individuals can minimize tax burdens, maximize the value of their gifts, and ensure their wealth is transferred according to their wishes. Tax laws and regulations are subject to change, and it is crucial to stay informed about these changes to maintain the effectiveness of tax-efficient gifting strategies. Regularly consulting with tax and financial professionals can help you stay updated on any adjustments to gift tax exclusions, exemptions, and rates, as well as the introduction of new tax-efficient strategies or modifications to existing ones. Each individual's financial situation and estate planning objectives are unique, and certain factors may warrant additional considerations when implementing tax-efficient gifting strategies. As tax laws and personal circumstances change, it is essential to consult with tax and financial professionals to regularly review and update gifting strategies to maintain optimal tax efficiency.What Are Tax-Efficient Gifting Strategies?

Overview of Gift Taxes

Federal Gift Tax

State Gift Taxes

Tax-Efficient Gifting Strategies

Utilizing the Annual Gift Tax Exclusion

Taking Advantage of the Lifetime Gift Tax Exemption

Gifting Appreciated Assets

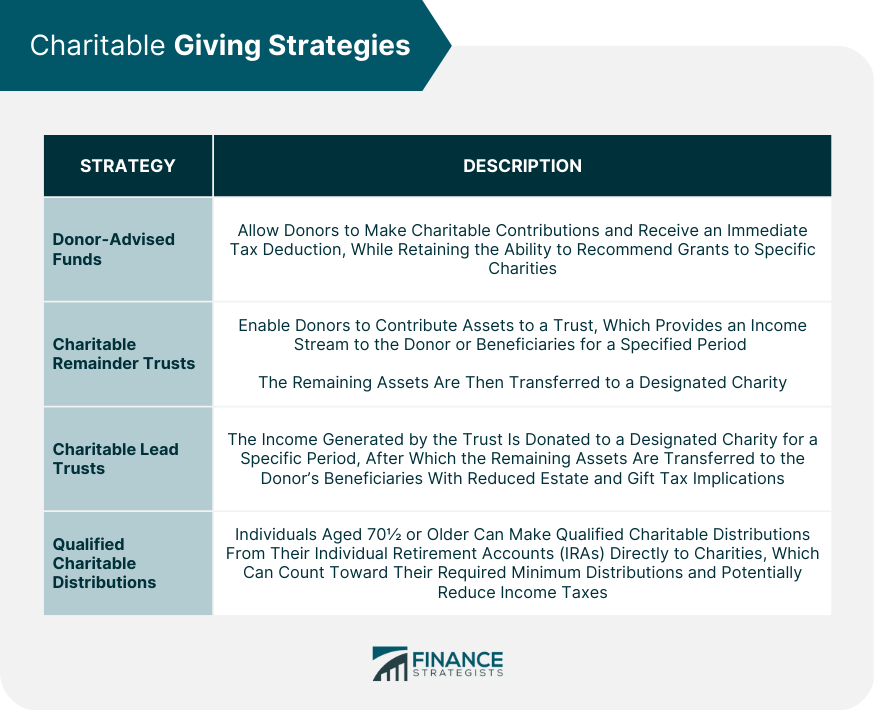

Charitable Giving Strategies

Gifting Strategies for Education and Medical Expenses

Direct Payment of Education Expenses

529 Plans

Direct Payment of Medical Expenses

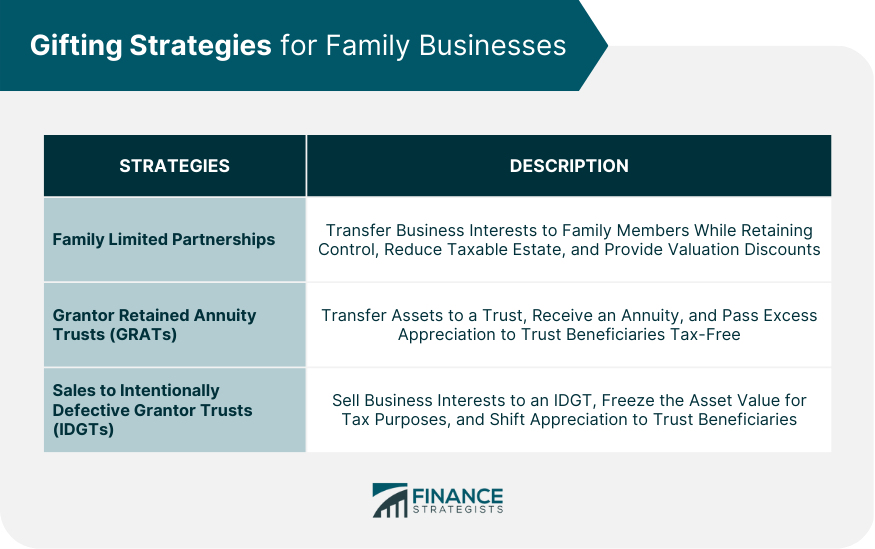

Gifting Strategies for Family Businesses

Family Limited Partnerships

Grantor Retained Annuity Trusts (GRATs)

Sales to Intentionally Defective Grantor Trusts (IDGTs)

Gifting Strategies for Life Insurance

Irrevocable Life Insurance Trusts (ILITs)

Wealth Replacement Strategies

Estate Planning Considerations

Coordinating Gifting Strategies With Estate Planning

Impact of Gifting on Estate Taxes

Ensuring Liquidity for Estate Tax Payments

Conclusion

Tax-Efficient Gifting Strategies FAQs

A tax-efficient gifting strategy refers to a plan or approach for making gifts to others while minimizing the tax impact on the giver and/or the recipient. This may involve using tax-advantaged accounts or instruments, such as a donor-advised fund or a 529 college savings plan, or taking advantage of certain tax rules, such as the annual gift tax exclusion.

The annual gift tax exclusion is a tax rule that allows you to give a certain amount of money each year to another person without having to pay any gift tax. As of 2026, the annual gift tax exclusion is $19,000 (also $19,000 in 2025) per recipient. This means you can give up to $19,000 to as many people as you want in 2026 without incurring any gift tax. Married couples can give up to $38,000 in 2026 (also $38,000 in 2025) per recipient by splitting the gift.

A donor-advised fund (DAF) is a charitable giving vehicle that allows you to make a tax-deductible contribution to a fund, which can then be used to support charitable organizations over time. One way to use a DAF for tax-efficient gifting is to contribute appreciated assets, such as stocks or mutual funds, to the fund. This can help you avoid capital gains taxes on the appreciated assets and also allows you to take an immediate tax deduction for the full value of the contribution. You can then recommend grants from the fund to support the charities of your choice.

A 529 college savings plan is a tax-advantaged account designed to help families save for future college expenses. One way to use a 529 plan for tax-efficient gifting is to make contributions to the plan for a child or grandchild. These contributions are considered gifts for tax purposes and may be subject to the annual gift tax exclusion. In addition, the earnings on the account grow tax-free as long as they are used for qualified education expenses.

In general, there are no tax implications for receiving a gift. The recipient does not have to pay income tax on the value of the gift, and gift tax is typically paid by the giver, if at all. However, there are some exceptions. For example, if the gift is in the form of income-producing property, such as rental real estate or stocks that pay dividends, the recipient may have to pay income tax on the income generated by the property.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.