Retirement tax brackets are ranges of income that determine the tax rate applied to a person's retirement income. These brackets determine the amount of tax owed based on different sources of income during retirement. It's important for individuals to comprehend retirement tax brackets as it assists in proper financial planning and minimizing tax obligations. With a good understanding of the tax implications of various income sources, retirees can increase their retirement savings and sustain a comfortable lifestyle. Knowledge of retirement tax brackets can also assist in making informed choices about investments, withdrawals, and other financial aspects. Federal retirement tax brackets refer to the income tax ranges established by the federal government. These brackets determine the tax rate applicable to an individual's income during retirement. The federal tax system is progressive, meaning that as income increases, the tax rate applied to that income also increases. It's essential to stay updated on current federal tax laws to ensure accurate tax calculations. State-specific retirement tax brackets are income tax ranges established by individual states. These brackets, like federal brackets, determine the tax rate applicable to retirement income. However, state tax laws and rates can vary significantly, with some states offering favorable tax treatment to retirees and others levying higher taxes. It's crucial to understand the tax laws of the state in which one resides to plan effectively for retirement. Various sources of retirement income can impact an individual's retirement tax bracket. These sources may include Social Security benefits, pension income, retirement account withdrawals, and investment income. Different types of income may be subject to different tax rates or rules, so understanding each income source's tax implications is critical for effective financial planning. Filing status is an essential factor in determining retirement tax brackets. The available filing statuses include single, married filing jointly, married filing separately, and head of household. Each status has different tax brackets and rates, so choosing the appropriate filing status can greatly impact the amount of tax owed during retirement. Age plays a role in determining retirement tax brackets, as older individuals are generally eligible for additional tax breaks and deductions. These may include a higher standard deduction and additional tax credits, which can help to reduce overall tax liabilities. Being aware of age-related tax benefits can help retirees plan more effectively and minimize their tax burdens. Various deductions and credits can impact retirement tax brackets by reducing taxable income or directly lowering tax liabilities. Examples include standard deductions, itemized deductions, and tax credits for specific expenses or situations. Taking advantage of available deductions and credits can help retirees lower their overall tax burden and keep more of their retirement income. The taxability of Social Security benefits depends on an individual's total income and filing status. For some retirees, a portion of their Social Security benefits may be subject to federal income tax. Understanding the rules surrounding the taxation of Social Security benefits is crucial for accurate tax planning and ensuring compliance with federal tax laws. Retirement tax brackets play a role in determining the taxation of Social Security benefits. The higher the income bracket, the greater the portion of benefits that may be subject to federal income tax. Being aware of how retirement tax brackets affect Social Security taxation can help retirees plan for potential tax liabilities and make informed decisions about income sources. Traditional IRAs are tax-deferred retirement accounts, meaning that contributions are made with pre-tax dollars and taxes are paid upon withdrawal. Withdrawals from traditional IRAs are treated as ordinary income and subject to the retiree's current tax bracket. Understanding the tax implications of traditional IRA withdrawals can help retirees plan for and manage their tax liabilities in retirement. Roth IRAs are funded with after-tax dollars, which means qualified withdrawals are tax-free in retirement. Since Roth IRA withdrawals do not increase taxable income, they do not impact an individual's retirement tax bracket. Roth IRAs can be a valuable tool for tax planning in retirement, as they provide flexibility in managing taxable income and tax brackets. Similar to traditional IRAs, 401(k) plan withdrawals are taxed as ordinary income at the individual's current tax rate. Understanding how 401(k) withdrawals affect retirement tax brackets is essential for tax planning and minimizing tax liabilities. Properly timing and structuring 401(k) withdrawals can help retirees manage their tax brackets and maximize their retirement savings. Private pension plan income is generally taxed as ordinary income in retirement. As such, it can impact an individual's retirement tax bracket. Understanding the tax implications of private pension plan income can help retirees plan for their tax liabilities and make informed decisions about how to manage their retirement income sources. Public pension plan income, such as from government or military pensions, is typically subject to federal income tax as ordinary income. However, some states may offer favorable tax treatment for public pension income. Understanding the tax implications of public pension plan income at the federal and state levels is essential for accurate tax planning and minimizing tax liabilities. Capital gains, or the profits from the sale of investments, can impact retirement tax brackets. Long-term capital gains are generally taxed at lower rates than ordinary income, while short-term gains are taxed as ordinary income. Understanding the tax treatment of capital gains can help retirees make strategic investment decisions and manage their retirement tax brackets. Dividends, or income received from investments in stocks or mutual funds, can also impact retirement tax brackets. Qualified dividends are generally taxed at lower rates than ordinary income, while non-qualified dividends are taxed as ordinary income. Knowing the tax treatment of dividend income can help retirees make informed investment decisions and manage their retirement tax brackets. Interest income, such as from bonds or savings accounts, are generally taxed as ordinary income and can impact retirement tax brackets. Understanding the tax implications of interest income can help retirees make informed decisions about their investments and manage their retirement tax brackets effectively. Optimizing withdrawals from various retirement accounts can help minimize retirement tax brackets and overall tax liabilities. This strategy may involve withdrawing from tax-deferred accounts, such as traditional IRAs or 401(k) plans, in combination with tax-free withdrawals from Roth IRAs. Properly timing and structuring withdrawals can help retirees manage their tax brackets and maximize their retirement savings. Adopting tax-efficient investment strategies can help retirees manage their retirement tax brackets and reduce tax liabilities. These strategies may include investing in tax-efficient assets, such as municipal bonds or dividend-paying stocks, and tax-advantaged investment vehicles, like Roth IRAs or index funds. Implementing tax-efficient strategies can help retirees make the most of their investments while minimizing tax consequences. Tax-loss harvesting is a strategy that involves selling investments at a loss to offset taxable gains from other investments. This can help manage retirement tax brackets by reducing overall taxable income. Understanding and effectively utilizing tax-loss harvesting can provide retirees with valuable tax savings and help them maintain their desired retirement tax bracket. Estate taxes are levied on the transfer of wealth upon an individual's death. Depending on the size of the estate and the applicable tax laws, retirement tax brackets may play a role in determining the amount of estate tax owed. Proper estate planning, including understanding the tax implications of retirement tax brackets, can help minimize estate tax liabilities and preserve wealth for beneficiaries. Gifting strategies can help retirees manage their retirement tax brackets and reduce estate tax liabilities. By making strategic gifts to family members or charities during their lifetime, retirees can lower their taxable income, reduce their retirement tax bracket, and minimize potential estate taxes. Understanding the tax implications of gifting strategies can help retirees make informed decisions and maximize their wealth transfer. Retirement tax brackets play a critical role in determining the tax rate applied to a person's retirement income. Understanding the different types of retirement tax brackets, such as federal and state-specific brackets, can help retirees plan for potential tax liabilities effectively. Factors like sources of retirement income, filing status, age, and deductions/credits can impact retirement tax brackets and should be taken into account during financial planning. Additionally, retirement tax brackets can also impact Social Security benefits, pension income, and investment income. Adopting tax planning strategies like optimizing withdrawals, tax-efficient investment strategies, and tax-loss harvesting can help retirees manage their tax brackets and reduce overall tax liabilities. Finally, estate planning, including understanding the tax implications of retirement tax brackets, can help minimize estate tax liabilities and preserve wealth for beneficiaries. Professional tax advisors can help you navigate the complexities of retirement tax brackets, optimize your tax strategies, and ensure you're making informed decisions to maximize your retirement savings.What Are Retirement Tax Brackets?

Types of Retirement Tax Brackets

Federal Retirement Tax Brackets

State-Specific Retirement Tax Brackets

Factors Affecting Retirement Tax Brackets

Sources of Retirement Income

Filing Status in Retirement Tax Brackets

Age and Retirement Tax Brackets

Deductions and Credits

Retirement Tax Brackets and Social Security Benefits

Taxability of Social Security Benefits

Retirement Tax Brackets Affecting Social Security Taxation

Retirement Tax Brackets and Retirement Account Withdrawals

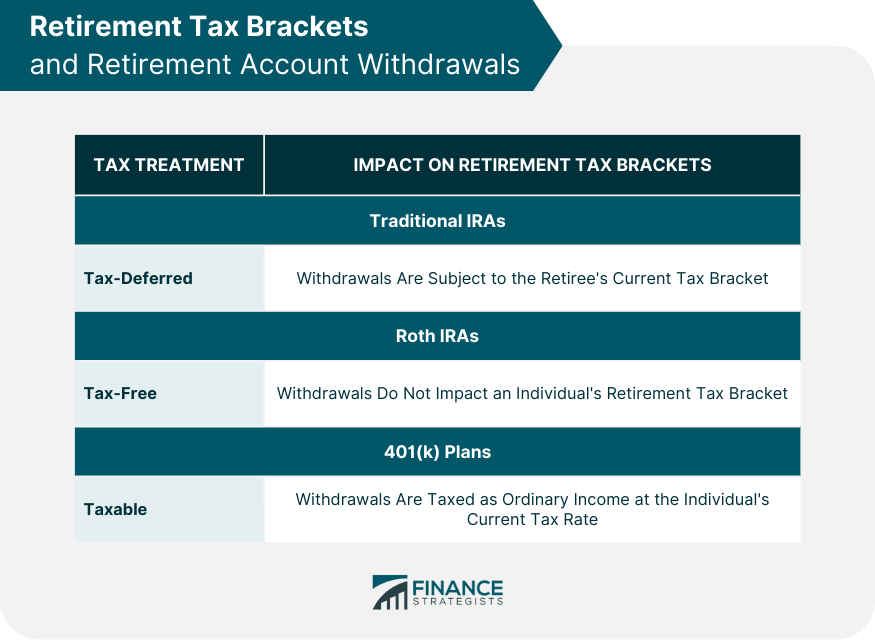

Traditional IRAs and Retirement Tax Brackets

Roth IRAs and Retirement Tax Brackets

401(k) Plans and Retirement Tax Brackets

Retirement Tax Brackets and Pension Income

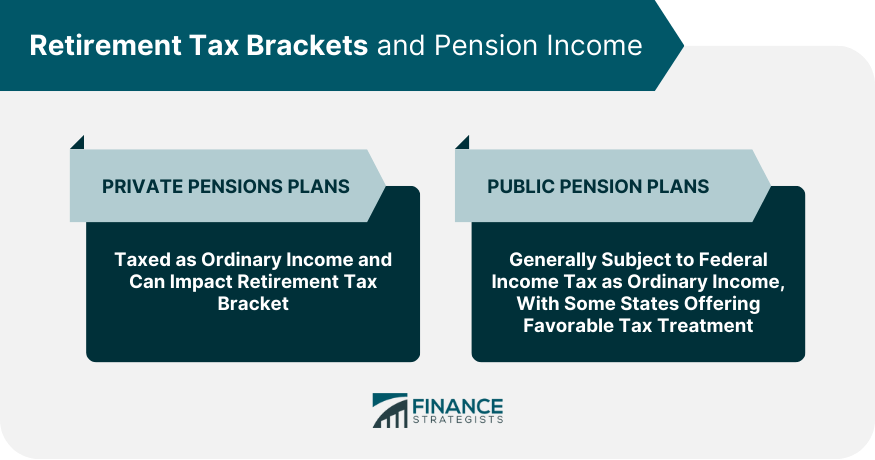

Private Pension Plans and Retirement Tax Brackets

Public Pension Plans and Retirement Tax Brackets

Retirement Tax Brackets and Investment Income

Capital Gains and Retirement Tax Brackets

Dividends and Retirement Tax Brackets

Interest Income and Retirement Tax Brackets

Tax Planning Strategies for Retirement Tax Brackets

Optimizing Withdrawals to Minimize Retirement Tax Brackets

Tax-Efficient Investment Strategies

Tax-Loss Harvesting

Retirement Tax Brackets and Estate Planning

Estate Taxes and Retirement Tax Brackets

Gifting Strategies and Retirement Tax Brackets

Final Thoughts

Retirement Tax Brackets FAQs

Retirement tax brackets are the income ranges used to determine the tax rate applied to an individual's retirement income. Understanding retirement tax brackets is essential for effective financial planning, as it helps retirees manage their taxable income, minimize tax liabilities, and make informed decisions about investments, withdrawals, and other financial matters.

Different sources of retirement income, such as Social Security benefits, pension income, retirement account withdrawals, and investment income, can impact retirement tax brackets. Each income source may have unique tax implications and rates, making it crucial for retirees to understand how each type of income affects their overall tax liability.

Retirees can minimize their retirement tax brackets by optimizing withdrawals from various retirement accounts, adopting tax-efficient investment strategies, utilizing tax-loss harvesting, and taking advantage of available deductions and credits. Consulting with a financial professional can help retirees navigate these strategies and optimize their tax planning.

Federal retirement tax brackets determine the tax rate applicable to an individual's income at the federal level, while state-specific retirement tax brackets determine the tax rate at the state level. Understanding both federal and state tax laws and their impact on retirement income is essential for effective tax planning and minimizing tax liabilities.

Tax planning services, provided by certified public accountants or financial planners, can help retirees understand the complexities of retirement tax brackets, optimize their tax strategies, and make informed decisions about their financial resources. By seeking expert advice, retirees can ensure they are maximizing their retirement savings and minimizing tax liabilities.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.