Plan conversion is a process in retirement planning that involves transitioning from one type of retirement plan to another. The goal of plan conversion is to provide tax advantages, better investment options, or other benefits that help individuals achieve their retirement goals more effectively. By understanding the various types of retirement plans and their conversion options, individuals can make informed decisions that align with their long-term financial goals. A Traditional IRA is a tax-deferred retirement account that allows individuals to contribute pre-tax income, lowering their taxable income in the current year. The investment growth in the account is tax-deferred until withdrawals are made during retirement. Individuals with a Traditional IRA can convert it into a Roth IRA, subject to income and filing status requirements. This conversion may also be applicable when transitioning from an employer-sponsored plan, such as a 401(k) or a 403(b), to an IRA. A Roth IRA is a retirement account that allows individuals to contribute after-tax income. Although contributions are not tax-deductible, the earnings and qualified withdrawals are tax-free. Converting a Traditional IRA to a Roth IRA is the most common conversion scenario. This conversion typically requires the payment of taxes on the converted amount in the year of conversion. A 401(k) plan is an employer-sponsored retirement plan that allows employees to contribute a portion of their salary on a pre-tax basis. Employers may also offer matching contributions, enhancing the plan's value. Upon leaving an employer, individuals may have the option to convert their 401(k) plan to an IRA. Another option is to roll the 401(k) balance into a new employer's plan if permitted. A 403(b) plan is a retirement plan for employees of tax-exempt organizations, such as schools and hospitals. Similar to a 401(k), the 403(b) allows pre-tax contributions and may offer employer-matching contributions. Similar to a 401(k), a 403(b) can be converted to an IRA or rolled into a new employer's plan when changing jobs. There are additional retirement plans available, such as SEP IRAs and SIMPLE IRAs, which cater to small business owners and the self-employed. Conversion options for these plans may vary, and individuals should consult a financial advisor to understand their choices. Understanding one's current and projected future income is crucial when considering plan conversion. A conversion may be more beneficial if individuals expect their income to be higher in retirement than it is currently. When converting a retirement plan, individuals may need to pay taxes on the converted amount. The tax liability depends on the type of plan and the individual's current tax bracket. Taxes upon withdrawal from retirement accounts vary depending on the plan type. Traditional IRAs and 401(k) plans require taxes to be paid on withdrawals, while Roth IRAs and Roth 401(k) plans have tax-free withdrawals. The time remaining before retirement is a crucial factor in conversion decisions. Individuals with a longer time horizon may benefit more from a conversion due to the tax advantages and potential investment growth. Different retirement plans offer varying investment options. When considering a conversion, it is essential to evaluate the investment options available in the new plan and compare them to the current plan. Contribution limits for different retirement plans may affect the decision to convert. Individuals should understand the limits for each plan type and consider how these limits may impact their overall retirement savings strategy. Before initiating a plan conversion, individuals should assess their current financial situation, retirement goals, and the potential benefits of conversion. This evaluation will help determine whether a conversion aligns with their long-term objectives. After identifying the need for conversion, individuals must choose the appropriate plan based on their financial goals, investment preferences, and tax considerations. Each retirement plan has specific rules and requirements for conversion. It is essential to understand these rules to ensure a smooth and compliant conversion process. Once the appropriate plan has been selected and the rules are understood, individuals can initiate the conversion process. This may involve contacting the plan administrators, completing the required paperwork, and transferring funds between accounts. After the conversion is complete, individuals should monitor their new plan regularly to ensure it continues to meet their retirement goals and make adjustments as needed. Misjudging tax implications during the conversion can lead to unexpected tax liabilities. Individuals should carefully consider the tax consequences before converting their retirement plan. Market volatility can impact the value of investments during the conversion process. Individuals should be aware of market conditions and consider the timing of the conversion accordingly. Some plan conversions may involve fees or penalties. It is crucial to understand any costs associated with conversion and weigh them against the potential benefits. Converting a plan at the wrong time can have negative consequences, such as triggering a higher tax liability or missing out on investment opportunities. Timing is crucial in the conversion process. Individuals with multiple retirement accounts should be cautious when converting plans to avoid creating an unnecessarily complex financial situation. Consolidation and simplification of accounts may be beneficial in some cases. Plan conversion is a crucial aspect of retirement planning that involves transitioning from one type of retirement plan to another. By understanding the various types of retirement plans and their conversion options, individuals can make informed decisions that align with their long-term financial goals. Factors such as current and projected income, tax implications, time horizon until retirement, investment options, and contribution limits play a crucial role in making these decisions. The conversion process requires careful evaluation, selection of an appropriate plan, understanding of conversion rules, and ongoing monitoring of the new plan. Being aware of potential pitfalls and risks can help ensure a successful conversion. Consulting a financial advisor for guidance and support throughout the process is highly recommended to navigate the complexities of plan conversion and achieve a secure and comfortable retirement.Definition of Plan Conversion

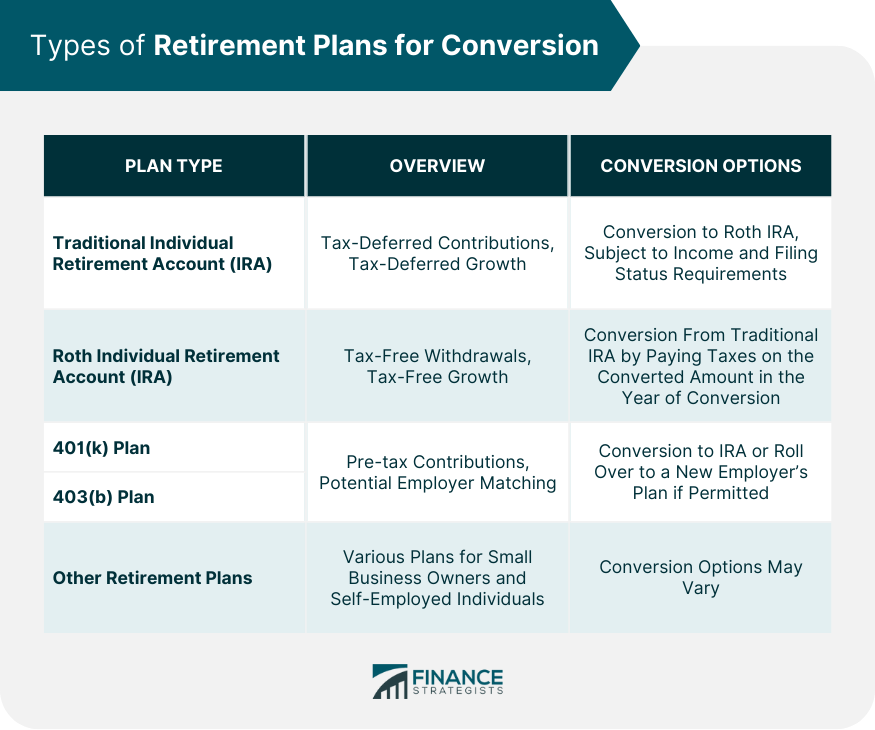

Types of Retirement Plans for Conversion

Traditional Individual Retirement Account (IRA)

Conversion Options

Roth Individual Retirement Account (IRA)

Conversion Options

401(k) Plans

Conversion Options

403(b) Plans

Conversion Options

Other Retirement Plans

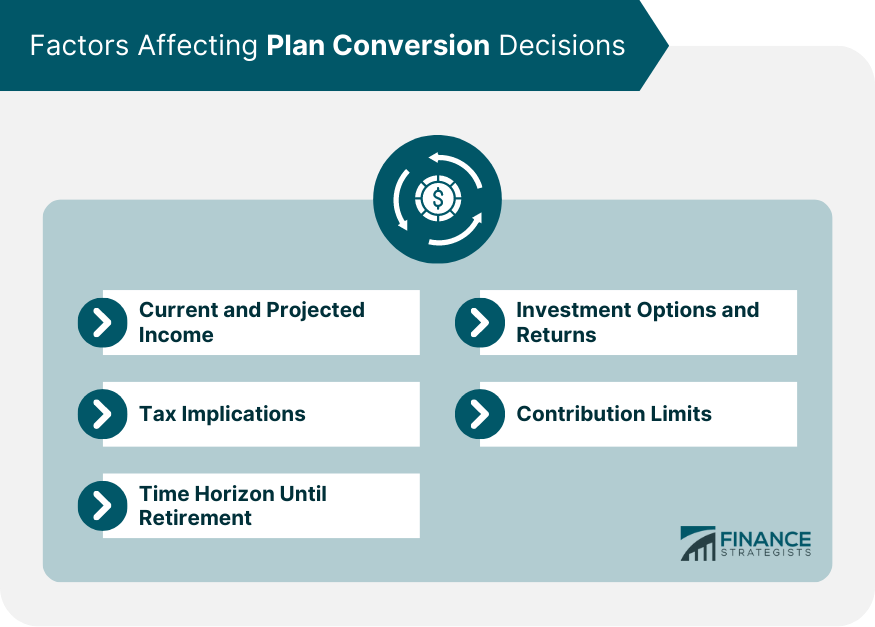

Factors Affecting Plan Conversion Decisions

Current and Projected Income

Tax Implications

Conversion Taxes

Withdrawal Taxes

Time Horizon Until Retirement

Investment Options and Returns

Contribution Limits

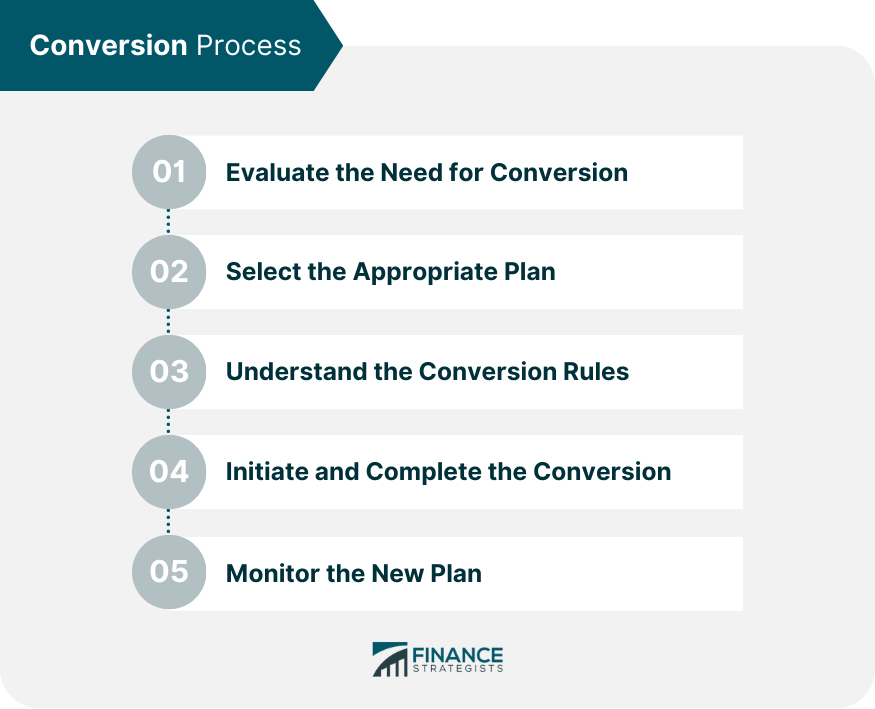

Conversion Process

Evaluating the Need for Conversion

Selecting the Appropriate Plan

Understanding the Conversion Rules

Initiating and Completing the Conversion

Monitoring the New Plan

Potential Pitfalls and Risks of Plan Conversion

Tax Consequences

Market Fluctuations

Conversion Costs

Mistimed Conversions

Managing Multiple Retirement Accounts

Conclusion

Plan Conversion FAQs

A plan conversion involves changing one type of retirement plan into another, such as converting a Traditional IRA to a Roth IRA or rolling over a 401(k) to an IRA. Plan conversions can provide tax advantages, better investment options, or other benefits, helping individuals achieve their retirement goals more effectively.

Individuals should consider a plan conversion when they believe that a different retirement plan type would better align with their long-term financial goals, tax situation, or investment preferences. Factors such as current and projected income, tax implications, time horizon until retirement, and contribution limits should be considered before making a conversion decision.

Risks and pitfalls of plan conversion include tax consequences, market fluctuations, conversion costs, mistimed conversions, and the complexity of managing multiple retirement accounts. Careful consideration and planning can help mitigate these risks and ensure a successful conversion.

A financial advisor can help individuals assess their financial situation, evaluate the potential benefits of a plan conversion, and ensure that the conversion aligns with their long-term retirement goals. They can also assist with the conversion process and provide ongoing support in managing the new plan.

When selecting a new plan for a plan conversion, individuals should consider factors such as the tax implications of the new plan, the available investment options, contribution limits, and any rules or requirements specific to the plan. Additionally, they should ensure that the new plan aligns with their long-term financial goals and retirement objectives.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.